Key Insights

The German Minimally Invasive Surgery (MIS) Devices market is projected for substantial growth, fueled by technological innovation and rising patient demand for less invasive procedures. With a market size of 94.45 billion in the base year 2025, the industry is expected to expand at a Compound Annual Growth Rate (CAGR) of 16.1% through 2033. This expansion is largely attributed to the increasing adoption of advanced MIS devices, including robotic-assisted surgical systems, electrosurgical devices, and advanced endoscopic instruments. These technologies deliver significant patient benefits such as reduced trauma, faster recovery, and enhanced surgical precision, making them highly sought after by healthcare providers and patients alike. Additionally, Germany's aging demographic and the growing incidence of chronic diseases requiring surgical intervention are contributing to sustained demand for innovative MIS solutions.

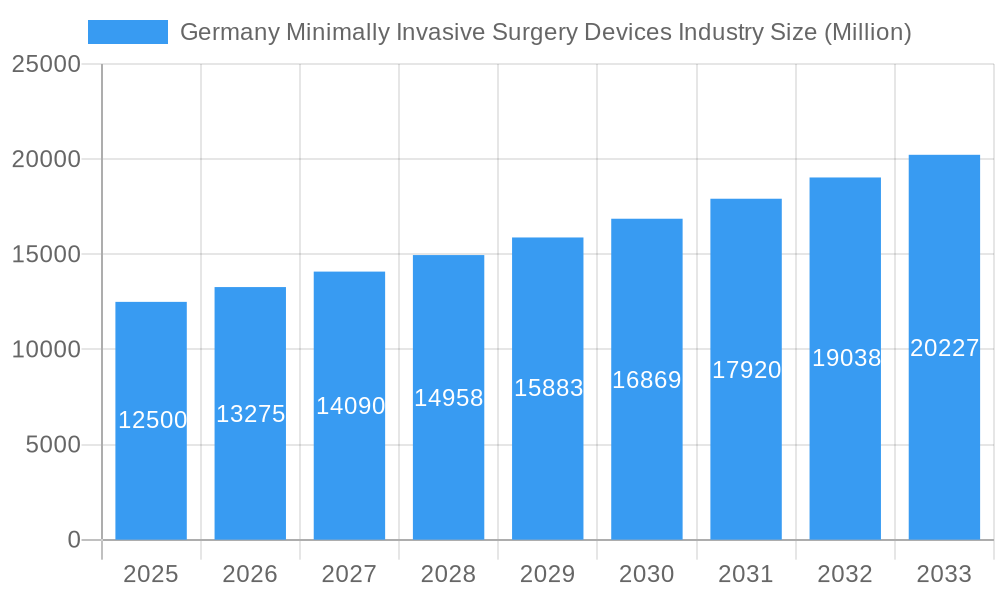

Germany Minimally Invasive Surgery Devices Industry Market Size (In Billion)

Key application areas, including cardiovascular, gastrointestinal, and gynecological/urological procedures, are driving this market expansion. Continuous research and development efforts are focused on improving handheld instruments, monitoring and visualization devices, and laser-based systems. Leading industry players are actively investing in R&D and strategic collaborations to launch new products and broaden their market presence. While market growth is robust, potential challenges may include the initial investment cost of advanced robotic systems and the requirement for specialized healthcare professional training. Despite these factors, the German MIS Devices market exhibits a highly positive outlook with a consistent upward trend anticipated throughout the forecast period.

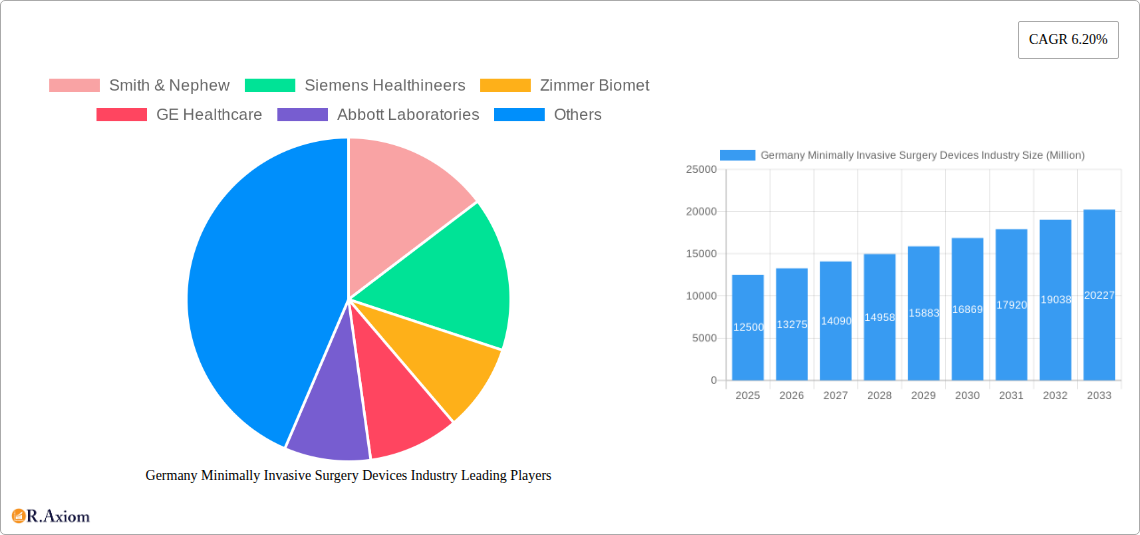

Germany Minimally Invasive Surgery Devices Industry Company Market Share

Germany Minimally Invasive Surgery Devices Industry Market Concentration & Innovation

The German minimally invasive surgery (MIS) devices market exhibits a moderate to high concentration, driven by the presence of established global players and a robust domestic medical technology sector. Key companies like Smith & Nephew, Siemens Healthineers, Zimmer Biomet, GE Healthcare, Abbott Laboratories, Medtronic PLC, Koninklijke Philips NV, Intuitive Surgical Inc, Stryker Corporation, and Olympus Corporation collectively hold a significant market share, estimated to be over 70%. Innovation remains a critical differentiator, propelled by substantial R&D investments and a strong emphasis on developing advanced robotic-assisted surgical systems, sophisticated endoscopic devices, and smart monitoring and visualization equipment. The German regulatory framework, characterized by stringent CE marking requirements and adherence to the Medical Device Regulation (MDR), plays a crucial role in ensuring product safety and efficacy, albeit sometimes posing challenges to market entry for smaller innovators. Product substitutes, while present in some basic surgical tools, are less impactful for highly specialized MIS procedures requiring advanced technology. End-user trends are shifting towards outpatient procedures, shorter recovery times, and improved patient outcomes, directly fueling demand for innovative MIS solutions. Mergers and acquisitions are strategic tools for consolidation and market expansion, with recent M&A deal values in the broader European MIS sector ranging from tens to hundreds of millions, indicating active consolidation.

Germany Minimally Invasive Surgery Devices Industry Industry Trends & Insights

The Germany Minimally Invasive Surgery Devices Industry is poised for significant expansion, driven by a confluence of technological advancements, an aging population, and increasing healthcare expenditure. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 8.5% over the forecast period of 2025-2033, with an estimated market size of xx Billion Euros in 2025, reaching xx Billion Euros by 2033. This growth is underpinned by a rising prevalence of chronic diseases and lifestyle-related conditions that necessitate surgical interventions, where MIS offers distinct advantages such as reduced patient trauma, faster recovery, and shorter hospital stays. Technological disruptions are a primary catalyst, with the integration of artificial intelligence (AI) and machine learning (ML) into surgical planning and execution, enhanced visualization technologies like 4K and 8K imaging, and the continuous refinement of robotic-assisted surgery platforms. The increasing adoption of these sophisticated systems is a key market penetration driver. Consumer preferences are increasingly aligning with less invasive treatment options, as patients become more informed about the benefits of MIS. This growing patient demand, coupled with physician advocacy for MIS techniques, is creating a favorable market environment. Competitive dynamics are intense, with companies focusing on product differentiation, strategic partnerships, and expanding their product portfolios to cater to a wider range of applications. The development of single-use instruments and advanced energy devices also contributes to market growth by addressing concerns related to sterilization and efficiency.

Dominant Markets & Segments in Germany Minimally Invasive Surgery Devices Industry

The Cardiovascular and Gastrointestinal segments stand out as dominant application areas within the German Minimally Invasive Surgery Devices Industry. The cardiovascular segment's leadership is driven by the high prevalence of heart disease in Germany and the increasing preference for less invasive procedures like angioplasty, stenting, and bypass surgery, where specialized MIS devices are indispensable. The Gastrointestinal segment also demonstrates robust growth due to the rising incidence of conditions such as GERD, inflammatory bowel disease, and colorectal cancer, all of which are increasingly managed through laparoscopic and endoscopic interventions.

Within the product segmentation, Endoscopic Devices and Robotic Assisted Surgical Systems are commanding substantial market shares. Endoscopic devices, encompassing a wide array of diagnostic and therapeutic tools like endoscopes, laparoscopes, and colonoscopes, are foundational to a vast number of MIS procedures. Their versatility and ongoing technological enhancements, including improved imaging and maneuverability, ensure their continued dominance. The rapid advancement and adoption of Robotic Assisted Surgical Systems, although representing a premium segment, are significantly contributing to market value and growth. These systems, utilized across various specialties including urology, gynecology, and general surgery, offer unparalleled precision, dexterity, and visualization, driving their increasing integration into surgical workflows.

- Key Drivers for Cardiovascular Dominance:

- High incidence of cardiovascular diseases in Germany.

- Technological advancements in interventional cardiology.

- Government initiatives promoting preventative cardiology.

- Key Drivers for Gastrointestinal Dominance:

- Increasing diagnosis rates for GI-related conditions.

- Development of advanced therapeutic endoscopic devices.

- Shorter patient recovery times associated with laparoscopic GI surgery.

- Key Drivers for Endoscopic Device Dominance:

- Wide range of diagnostic and therapeutic applications.

- Continuous innovation in imaging and miniaturization.

- Cost-effectiveness compared to robotic systems for certain procedures.

- Key Drivers for Robotic Assisted Surgical Systems Dominance:

- Enhanced surgical precision and control.

- Improved patient outcomes and reduced complications.

- Growing surgeon familiarity and training programs.

- Other Influential Segments:

- Gynecological and Urological applications are witnessing significant growth, particularly with advancements in robotic surgery for prostatectomies and hysterectomies.

- Orthopedic MIS devices are also expanding, driven by the demand for less invasive joint replacement and spinal procedures.

Germany Minimally Invasive Surgery Devices Industry Product Developments

Product developments in the German MIS devices industry are characterized by a relentless pursuit of enhanced precision, miniaturization, and integrated intelligence. Innovations are focusing on next-generation robotic surgical platforms offering greater dexterity and haptic feedback, advanced endoscopic imaging systems with AI-driven analytics for real-time diagnostics, and novel electrosurgical devices for more precise tissue dissection and coagulation. The integration of augmented reality (AR) for surgical guidance and the development of smart, connected instruments that transmit data for analysis are also key trends. These advancements offer surgeons superior control, enable more complex procedures to be performed minimally invasively, and ultimately contribute to improved patient outcomes and reduced recovery times, solidifying competitive advantages for companies at the forefront of R&D.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the Germany Minimally Invasive Surgery Devices Industry, encompassing detailed segmentation across product types and applications. The Product Segmentation covers Handheld Instruments, Guiding Devices, Electrosurgical Devices, Endoscopic Devices, Monitoring and Visualization Devices, Robotic Assisted Surgical Systems, Ablation Devices, Laser Based Devices, and Other MIS Devices. The Application Segmentation includes Aesthetic, Cardiovascular, Gastrointestinal, Gynecological and Urological, Orthopedic, and Other Applications. Each segment is analyzed for its market size, growth projections, and competitive dynamics. For instance, the Robotic Assisted Surgical Systems segment, while smaller in unit volume, represents a high-value market with significant growth potential, driven by technological sophistication and expanding clinical use. Conversely, Endoscopic Devices, with their broad applicability, are expected to maintain a substantial market share, fueled by continuous incremental innovations and widespread adoption across multiple medical disciplines.

Key Drivers of Germany Minimally Invasive Surgery Devices Industry Growth

Key drivers fueling the growth of the German MIS devices industry include an aging demographic, leading to increased demand for surgical interventions for age-related conditions. Technological innovation, particularly in robotics and imaging, enables more complex procedures to be performed minimally invasively, enhancing patient outcomes. Favorable reimbursement policies for MIS procedures in Germany further incentivize adoption. A growing emphasis on patient preference for less invasive treatments, quicker recovery times, and reduced hospital stays also acts as a significant growth catalyst. Furthermore, government initiatives aimed at modernizing healthcare infrastructure and promoting advanced medical technologies contribute to the expanding market.

Challenges in the Germany Minimally Invasive Surgery Devices Industry Sector

Despite robust growth, the German MIS devices industry faces several challenges. High upfront costs associated with advanced technologies like robotic surgical systems can be a barrier to widespread adoption, especially for smaller healthcare facilities. Stringent regulatory requirements and lengthy approval processes under the MDR can delay market entry for new products and innovative startups. The need for specialized training for surgeons to effectively utilize complex MIS technologies poses a logistical and financial challenge. Furthermore, intense competition among established players and the emergence of new market entrants can lead to price pressures and impact profit margins. Supply chain disruptions, though gradually easing, can still affect the availability of critical components and finished products.

Emerging Opportunities in Germany Minimally Invasive Surgery Devices Industry

Emerging opportunities in the German MIS devices industry lie in the development and adoption of AI-powered surgical planning and navigation systems, offering enhanced precision and personalized treatment. The growing demand for remote patient monitoring and telementoring in surgery presents a significant avenue for innovation. Expansion into niche surgical areas and the development of specialized MIS devices for emerging applications, such as regenerative medicine and advanced tumor ablation techniques, offer substantial growth potential. The increasing focus on sustainability within healthcare also presents an opportunity for companies developing reusable or environmentally friendly MIS devices and solutions. Furthermore, the continued refinement and cost reduction of robotic platforms will broaden their accessibility.

Leading Players in the Germany Minimally Invasive Surgery Devices Industry Market

- Smith & Nephew

- Siemens Healthineers

- Zimmer Biomet

- GE Healthcare

- Abbott Laboratories

- Medtronic PLC

- Koninklijke Philips NV

- Intuitive Surgical Inc

- Stryker Corporation

- Olympus Corporation

Key Developments in Germany Minimally Invasive Surgery Devices Industry Industry

- 2023/09: Launch of next-generation robotic surgical system with enhanced AI capabilities, improving surgeon dexterity and patient outcomes.

- 2023/07: Introduction of advanced endoscopic imaging technology offering higher resolution and real-time diagnostic analytics.

- 2022/11: Strategic partnership formed to accelerate the development and adoption of personalized MIS treatment plans.

- 2022/05: Acquisition of a key player in the ablation device market to expand product portfolio and market reach.

- 2021/10: CE marking obtained for a novel handheld instrument designed for precision tissue dissection in complex laparoscopic procedures.

Strategic Outlook for Germany Minimally Invasive Surgery Devices Industry Market

The strategic outlook for the German MIS devices industry remains highly positive, driven by ongoing technological advancements and sustained demand for less invasive healthcare solutions. Companies are expected to focus on integrating AI and machine learning into their product offerings to provide predictive analytics and enhanced surgical guidance. The expansion of robotic surgery into new specialties and the development of more affordable robotic platforms will be key growth catalysts. Furthermore, strategic collaborations and partnerships will be crucial for navigating the complex regulatory landscape and for co-developing innovative solutions. The increasing emphasis on value-based healthcare will also push for devices that demonstrate clear improvements in patient outcomes and cost-effectiveness.

Germany Minimally Invasive Surgery Devices Industry Segmentation

-

1. Product

- 1.1. Handheld Instruments

- 1.2. Guiding Devices

- 1.3. Electrosurgical Devices

- 1.4. Endoscopic Devices

- 1.5. Monitoring and Visualization Devices

- 1.6. Robotic Assisted Surgical Systems

- 1.7. Ablation Devices

- 1.8. Laser Based Devices

- 1.9. Other MIS Devices

-

2. Application

- 2.1. Aesthetic

- 2.2. Cardiovascular

- 2.3. Gastrointestinal

- 2.4. Gynecological and Urological

- 2.5. Orthopedic

- 2.6. Other Applications

Germany Minimally Invasive Surgery Devices Industry Segmentation By Geography

- 1. Germany

Germany Minimally Invasive Surgery Devices Industry Regional Market Share

Geographic Coverage of Germany Minimally Invasive Surgery Devices Industry

Germany Minimally Invasive Surgery Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Handheld Instruments

- 5.1.2. Guiding Devices

- 5.1.3. Electrosurgical Devices

- 5.1.4. Endoscopic Devices

- 5.1.5. Monitoring and Visualization Devices

- 5.1.6. Robotic Assisted Surgical Systems

- 5.1.7. Ablation Devices

- 5.1.8. Laser Based Devices

- 5.1.9. Other MIS Devices

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Aesthetic

- 5.2.2. Cardiovascular

- 5.2.3. Gastrointestinal

- 5.2.4. Gynecological and Urological

- 5.2.5. Orthopedic

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Germany Minimally Invasive Surgery Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Handheld Instruments

- 6.1.2. Guiding Devices

- 6.1.3. Electrosurgical Devices

- 6.1.4. Endoscopic Devices

- 6.1.5. Monitoring and Visualization Devices

- 6.1.6. Robotic Assisted Surgical Systems

- 6.1.7. Ablation Devices

- 6.1.8. Laser Based Devices

- 6.1.9. Other MIS Devices

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Aesthetic

- 6.2.2. Cardiovascular

- 6.2.3. Gastrointestinal

- 6.2.4. Gynecological and Urological

- 6.2.5. Orthopedic

- 6.2.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Smith & Nephew

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Siemens Healthineers

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Zimmer Biomet

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 GE Healthcare

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Abbott Laboratories

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Medtronic PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Koninklijke Philips NV

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Intuitive Surgical Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Stryker Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Olympus Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Smith & Nephew

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Minimally Invasive Surgery Devices Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Germany Minimally Invasive Surgery Devices Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany Minimally Invasive Surgery Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Germany Minimally Invasive Surgery Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: Germany Minimally Invasive Surgery Devices Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Germany Minimally Invasive Surgery Devices Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Germany Minimally Invasive Surgery Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Germany Minimally Invasive Surgery Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Germany Minimally Invasive Surgery Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 8: Germany Minimally Invasive Surgery Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 9: Germany Minimally Invasive Surgery Devices Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Germany Minimally Invasive Surgery Devices Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Germany Minimally Invasive Surgery Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Germany Minimally Invasive Surgery Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Minimally Invasive Surgery Devices Industry?

The projected CAGR is approximately 16.1%.

2. Which companies are prominent players in the Germany Minimally Invasive Surgery Devices Industry?

Key companies in the market include Smith & Nephew, Siemens Healthineers, Zimmer Biomet, GE Healthcare, Abbott Laboratories, Medtronic PLC, Koninklijke Philips NV, Intuitive Surgical Inc, Stryker Corporation, Olympus Corporation.

3. What are the main segments of the Germany Minimally Invasive Surgery Devices Industry?

The market segments include Product, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 94.45 billion as of 2022.

5. What are some drivers contributing to market growth?

; Higher Acceptance Rate of Minimally-invasive Surgeries over Traditional Surgeries in Country; Increasing Prevalence of Lifestyle-related and Chronic Disorders.

6. What are the notable trends driving market growth?

Orthopedic Surgery Segment is Expected to Exhibit Fastest Growth Rate Over the Forecast Period.

7. Are there any restraints impacting market growth?

; Uncertain Regulatory Framework.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Minimally Invasive Surgery Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Minimally Invasive Surgery Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Minimally Invasive Surgery Devices Industry?

To stay informed about further developments, trends, and reports in the Germany Minimally Invasive Surgery Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence