Key Insights

The European Polycarbonate Panels market is poised for robust growth, projecting a Compound Annual Growth Rate (CAGR) exceeding 3.50% through 2033. This expansion is primarily driven by the increasing demand for lightweight, durable, and energy-efficient materials across various end-user industries. Notably, the construction sector stands as a significant contributor, leveraging polycarbonate panels for roofing, glazing, and facade applications due to their excellent impact resistance, UV protection, and ease of installation. The automotive industry is also increasingly adopting these panels for their weight-reducing properties, contributing to improved fuel efficiency and performance, while the aerospace sector benefits from their high strength-to-weight ratio. Emerging applications in electrical and electronics, as well as agriculture for greenhouse construction, further bolster market demand. The market is segmented into various types, including solid, corrugated, and multi-walled polycarbonate panels, each catering to specific performance requirements and applications.

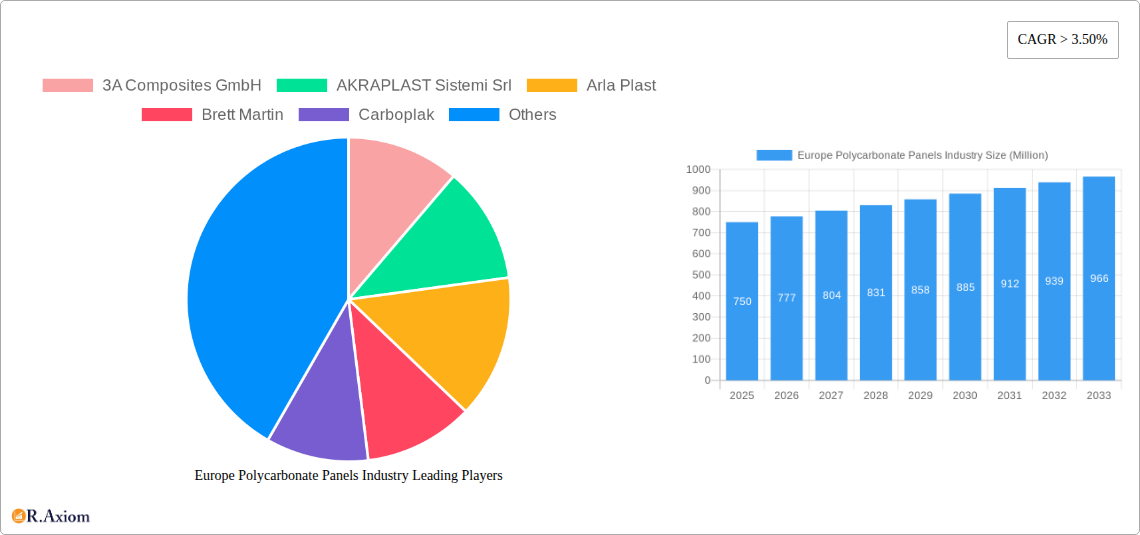

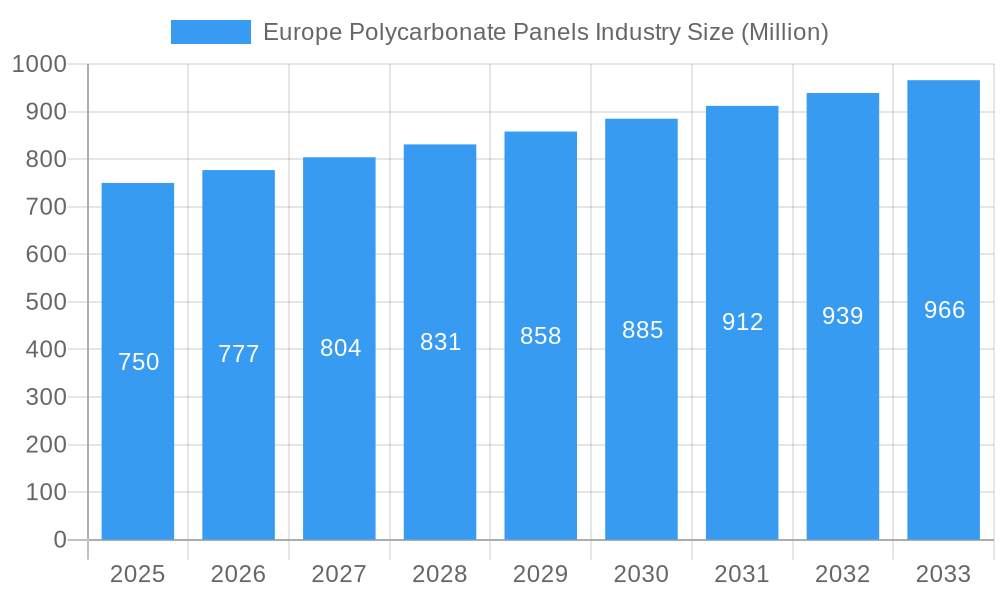

Europe Polycarbonate Panels Industry Market Size (In Million)

Several key trends are shaping the European Polycarbonate Panels market landscape. There's a discernible shift towards sustainable and eco-friendly building solutions, where polycarbonate panels offer advantages in terms of recyclability and their contribution to energy efficiency through improved insulation and natural lighting. Advancements in manufacturing technologies are leading to the development of enhanced polycarbonate panels with superior UV resistance, fire retardancy, and aesthetic appeal, opening up new application possibilities. However, the market also faces certain restraints. Fluctuations in raw material prices, particularly for polycarbonate resins, can impact manufacturing costs and, consequently, market pricing. Stringent regulatory frameworks and the availability of alternative materials, such as glass and other plastics, present ongoing competitive challenges. Despite these hurdles, the inherent benefits of polycarbonate panels, coupled with ongoing innovation and expanding applications, are expected to sustain a positive growth trajectory for the European market in the foreseeable future.

Europe Polycarbonate Panels Industry Company Market Share

Europe Polycarbonate Panels Industry Market Concentration & Innovation

The Europe polycarbonate panels market is characterized by a moderate to high concentration, with a mix of established global players and specialized regional manufacturers. Leading companies like SABIC, Palram Industries Ltd, and EXOLON GROUP hold significant market shares, driven by their extensive product portfolios, robust distribution networks, and continuous investment in research and development. Innovation is a critical differentiator, with a strong focus on developing advanced polycarbonate solutions offering enhanced UV resistance, improved thermal insulation, greater impact strength, and sustainability features. Regulatory frameworks in Europe, particularly those concerning building codes and environmental standards, are increasingly shaping product development, pushing for lighter, more energy-efficient, and recyclable materials. The availability of product substitutes, such as glass, acrylic, and metal panels, necessitates ongoing innovation to maintain competitive advantages. End-user trends, especially the growing demand for sustainable construction materials and lightweight components in the automotive and aerospace sectors, are key drivers for innovation. Mergers and acquisitions (M&A) activity, while not consistently high, plays a role in market consolidation and expansion of capabilities. For instance, the reported estimated M&A deal value in the broader plastics industry ranges from tens to hundreds of millions of Euros annually, indicating potential for strategic partnerships and acquisitions within the polycarbonate panel sector.

Europe Polycarbonate Panels Industry Industry Trends & Insights

The Europe Polycarbonate Panels Industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.5% to 6.5% during the forecast period of 2025–2033. This expansion is underpinned by several dynamic trends and insights shaping the market landscape. A primary growth driver is the escalating demand from the construction sector, fueled by increased urbanization, renovation projects, and a growing preference for energy-efficient building materials. Polycarbonate panels, with their excellent light transmission, insulation properties, and lightweight nature, are increasingly replacing traditional materials like glass in applications such as roofing, facades, and glazing. The automotive industry is another significant contributor, with a rising adoption of polycarbonate for lightweighting vehicles to improve fuel efficiency and reduce emissions. This trend is further propelled by advancements in automotive design and the need for durable, impact-resistant components.

Technological disruptions are playing a crucial role, with continuous improvements in manufacturing processes leading to enhanced product performance and cost-effectiveness. Innovations in UV stabilization, flame retardancy, and scratch resistance are expanding the application range of polycarbonate panels. Furthermore, the development of bio-circular and recycled polycarbonate materials, as evidenced by initiatives like Brett Martin's Marlon BioPlus, is aligning the industry with sustainability goals and attracting environmentally conscious consumers and businesses.

Consumer preferences are leaning towards materials that offer aesthetic appeal, durability, and ease of installation. Polycarbonate panels meet these demands with their versatility in terms of color, texture, and formability. The growing awareness and adoption of sustainable building practices and circular economy principles are also influencing purchasing decisions, favoring manufacturers who demonstrate a commitment to environmental responsibility.

Competitive dynamics remain intense, with key players differentiating themselves through product innovation, strategic partnerships, and market penetration efforts. The market penetration of polycarbonate panels in specific applications, such as industrial roofing, is already substantial, estimated to be over 70% in some Western European countries, indicating opportunities for further growth in emerging markets and niche applications. The overall market size for Europe Polycarbonate Panels is estimated to reach approximately 2.8 Billion Euros by 2025, with projections indicating a significant rise to over 4.5 Billion Euros by 2033.

Dominant Markets & Segments in Europe Polycarbonate Panels Industry

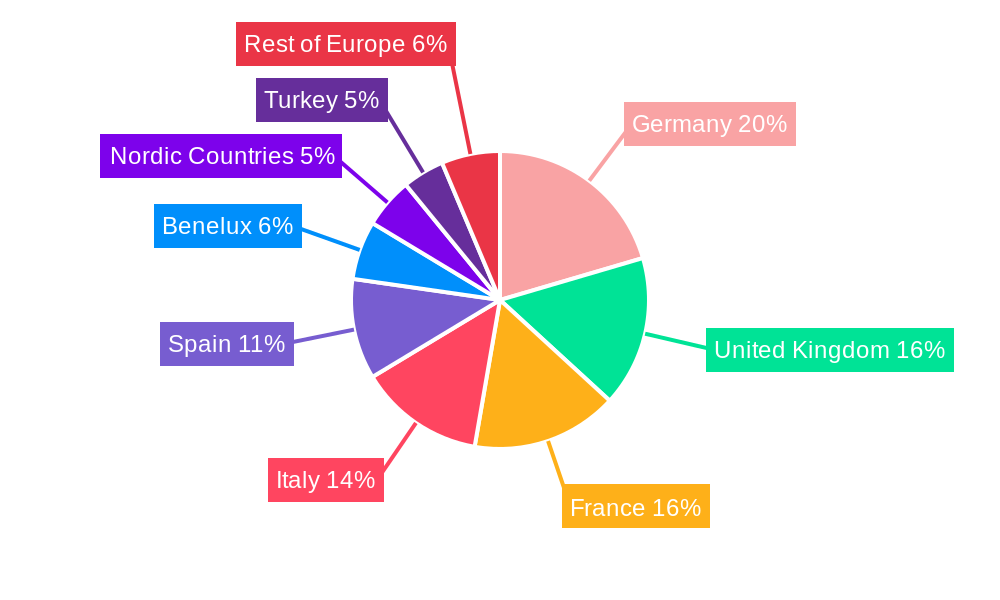

The European Polycarbonate Panels Industry exhibits distinct dominance across various geographical regions and product segments, driven by specific economic policies, infrastructure development, and evolving end-user demands.

Leading Region: Western Europe Western Europe, particularly countries like Germany, France, the UK, and Italy, currently represents the dominant geographical market for polycarbonate panels. This dominance is attributed to:

- Robust Construction Activity: Significant ongoing infrastructure projects, a thriving renovation market, and stringent building codes demanding high-performance materials.

- Advanced Manufacturing Base: Presence of key manufacturers and a well-established supply chain for raw materials and finished products.

- High Environmental Standards: A strong push towards sustainable construction and energy efficiency, favoring materials like polycarbonate.

- Automotive and Aerospace Hubs: Concentration of major automotive and aerospace manufacturers in the region drives demand for lightweight and durable polycarbonate components.

Dominant Segment by End-User Industry: Construction The Construction sector unequivocally dominates the European polycarbonate panels market, accounting for an estimated 65-70% of the total market share. This preeminence is a consequence of:

- Versatile Applications: Polycarbonate panels are used extensively in roofing, skylights, facades, conservatories, agricultural buildings, and industrial structures due to their exceptional light transmission, impact resistance, and insulation properties.

- Demand for Natural Light and Energy Efficiency: Architects and builders increasingly opt for polycarbonate to maximize natural light penetration while minimizing heat loss, contributing to lower energy consumption in buildings.

- Renovation and Retrofitting Projects: The extensive stock of older buildings in Europe presents a significant opportunity for retrofitting with modern, efficient materials like polycarbonate panels.

- Safety and Durability: In construction, the inherent safety features of polycarbonate, such as its shatterproof nature, are highly valued, especially in public buildings and areas prone to vandalism or extreme weather.

Dominant Segment by Type: Solid Polycarbonate Panels While all types of polycarbonate panels are witnessing growth, Solid Polycarbonate Panels currently hold the largest market share by type, estimated to be around 55-60%. Key drivers for their dominance include:

- Versatility and Aesthetic Appeal: Solid panels offer a sleek, transparent or translucent finish, making them ideal for architectural glazing, partitions, and display applications.

- High Impact Strength and Durability: Their robust nature makes them suitable for applications requiring exceptional resistance to physical impact, weather, and UV radiation.

- Ease of Fabrication: Solid polycarbonate sheets can be easily cut, drilled, and thermoformed, allowing for complex designs and custom solutions in construction and manufacturing.

- Widespread Applications: Their use spans from safety glazing and protective shields to architectural features and advertising displays.

Emerging Segments and Opportunities: While Construction and Solid panels lead, Multi-walled Polycarbonate Panels are gaining significant traction in the Agriculture sector for greenhouses, offering superior insulation and light diffusion, and in the Electrical and Electronics industry for protective enclosures due to their electrical insulation properties and impact resistance. The Aerospace and Automotive industries are increasingly exploring advanced polycarbonate composites for their lightweighting benefits.

Europe Polycarbonate Panels Industry Product Developments

Product development in the Europe Polycarbonate Panels industry is heavily focused on enhancing performance, sustainability, and application versatility. Key innovations include the introduction of bio-circular polycarbonate sheets, utilizing mass balancing for reduced environmental impact, and the development of panels with superior UV protection, enhanced fire retardancy, and improved thermal insulation properties. Companies are also investing in advanced coating technologies to improve scratch resistance and self-cleaning capabilities. The integration of polycarbonate into composite materials for lighter yet stronger components in automotive and aerospace is a significant trend. These developments aim to meet stringent regulatory demands, address growing environmental concerns, and expand the use of polycarbonate panels into more demanding and diverse applications.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Europe Polycarbonate Panels Industry, encompassing detailed segmentation by product type and end-user industry.

Type Segmentation:

- Solid Polycarbonate Panels: These panels are characterized by their monolithic structure, offering high impact resistance, optical clarity, and UV stability. They are projected to maintain their leading market share, with an estimated market size of approximately 1.6 Billion Euros in 2025, driven by their extensive use in glazing, facades, and safety applications.

- Corrugated Polycarbonate Panels: Known for their lightweight and structural strength, corrugated panels are extensively used in roofing and wall cladding for industrial, agricultural, and residential buildings. The market for corrugated panels is estimated to reach around 0.7 Billion Euros in 2025, with steady growth expected.

- Multi-walled Polycarbonate Panels: These panels feature internal air channels, providing excellent thermal insulation. They are increasingly favored in greenhouse construction and energy-efficient building envelopes, with a projected market size of approximately 0.5 Billion Euros in 2025.

End-user Industry Segmentation:

- Construction: This remains the largest segment, projected to reach over 1.8 Billion Euros in 2025, driven by demand for roofing, skylights, facades, and interior partitions.

- Aerospace: A niche but growing segment, leveraging polycarbonate's lightweight and impact-resistant properties for interior components. The market is estimated at approximately 0.1 Billion Euros in 2025.

- Automotive: Driven by lightweighting initiatives, this segment is projected to reach around 0.3 Billion Euros in 2025 for applications like sunroofs, lighting, and interior trim.

- Agriculture: Primarily for greenhouse applications, this segment is estimated at approximately 0.3 Billion Euros in 2025, benefiting from improved crop yields and energy savings.

- Electrical and Electronics: Used for protective enclosures and insulation, this segment is forecast to reach approximately 0.1 Billion Euros in 2025.

- Other End-user Industries: Encompassing signage, displays, and industrial applications, this segment is estimated at around 0.2 Billion Euros in 2025.

Key Drivers of Europe Polycarbonate Panels Industry Growth

The Europe Polycarbonate Panels Industry is propelled by a confluence of strategic growth drivers:

- Growing Demand for Sustainable Building Materials: Increasing environmental awareness and stringent regulations are favoring lightweight, energy-efficient, and recyclable materials like polycarbonate. Initiatives promoting bio-circular polycarbonate are a significant catalyst.

- Expansion of the Construction Sector: Ongoing infrastructure development, urban regeneration, and a robust renovation market across Europe are driving demand for high-performance glazing and cladding solutions.

- Automotive Lightweighting Trends: The automotive industry's focus on reducing vehicle weight for improved fuel efficiency and lower emissions is increasing the adoption of polycarbonate for various components.

- Technological Advancements in Manufacturing: Innovations in extrusion and co-extrusion processes are leading to enhanced product properties, such as superior UV resistance, impact strength, and thermal insulation, expanding application possibilities.

- Government Initiatives and Incentives: Favorable government policies supporting green building and renewable energy projects indirectly boost the demand for polycarbonate panels.

Challenges in the Europe Polycarbonate Panels Industry Sector

Despite strong growth prospects, the Europe Polycarbonate Panels Industry faces several challenges:

- Fluctuating Raw Material Prices: The industry is susceptible to price volatility of key raw materials like bisphenol A (BPA) and ethylene, impacting production costs and profit margins.

- Intense Competition and Price Sensitivity: The market is competitive, with a presence of both global manufacturers and regional players, leading to price pressures, especially in less differentiated segments.

- Recycling Infrastructure and End-of-Life Management: While polycarbonate is recyclable, the development of widespread and efficient recycling infrastructure across Europe remains a challenge, impacting the circularity of the material.

- Regulatory Hurdles and Evolving Standards: Adherence to increasingly complex and evolving building codes, fire safety regulations, and environmental standards can pose a compliance burden for manufacturers.

- Supply Chain Disruptions: Geopolitical events, logistical challenges, and the availability of skilled labor can impact the smooth functioning of the supply chain, affecting delivery timelines and costs.

Emerging Opportunities in Europe Polycarbonate Panels Industry

The Europe Polycarbonate Panels Industry is ripe with emerging opportunities driven by evolving market dynamics and technological advancements:

- Smart Buildings and IoT Integration: Opportunities exist in developing polycarbonate panels with integrated sensors or functionalities for smart building applications, enhancing energy management and building automation.

- Circular Economy and Recycled Content: Increased focus on sustainability creates a significant opportunity for companies that can effectively utilize recycled polycarbonate and develop closed-loop recycling systems.

- Expansion in Emerging European Markets: Growing economies in Eastern and Southern Europe present untapped potential for polycarbonate panel adoption in their expanding construction and infrastructure sectors.

- High-Performance Applications: Advancements in material science are opening doors for polycarbonate in specialized, high-performance applications, such as advanced glazing in extreme environments and lightweight structural components in new mobility solutions.

- Customization and Value-Added Services: Offering tailored solutions, including specialized coatings, colors, and integrated design services, can provide a competitive edge and tap into niche market demands.

Leading Players in the Europe Polycarbonate Panels Industry Market

- 3A Composites GmbH

- AKRAPLAST Sistemi Srl

- Arla Plast

- Brett Martin

- Carboplak

- Corplex

- Danpal

- dott gallina Srl

- EXOLON GROUP

- GI PLAST

- Isik Plastik

- NUDEC S A

- Onduline

- Palram Industries Ltd

- PLAZIT-POLYGAL

- Rodeca

- SABIC

- SafPlast Innovative

- Sintostamp SpA

- Sümer Plastik

- WZD Sp z o o

Key Developments in Europe Polycarbonate Panels Industry Industry

- September 2022: Brett Martin launched Marlon BioPlus, an innovative polycarbonate sheet from the company offering dramatically reduced environmental impact by switching from fossil-based resins to certified as 71% bio-circular through a mass balancing manufacturing process.

- January 2022: The Exolon Group and the Italian company Società Europea Plastica (SEP) combined their extrusion competence. They began cooperation on polycarbonate panels that offered the construction industry an extensive range of polycarbonate sheets.

Strategic Outlook for Europe Polycarbonate Panels Industry Market

The strategic outlook for the Europe Polycarbonate Panels Industry is one of sustained growth and innovation. Key catalysts include the increasing global demand for sustainable and energy-efficient building solutions, driving the adoption of polycarbonate in construction. The automotive sector's relentless pursuit of lightweighting for enhanced fuel efficiency will continue to be a significant growth engine. Strategic investments in research and development to create advanced materials with superior performance characteristics, coupled with a focus on circular economy principles and the utilization of recycled content, will be crucial for maintaining market leadership. Expansion into emerging European markets and the development of customized solutions for niche applications represent significant untapped potential. Furthermore, strategic partnerships and potential M&A activities will likely shape the competitive landscape, enabling companies to enhance their product portfolios, expand their geographical reach, and strengthen their technological capabilities, ensuring a robust and dynamic future for the industry.

Europe Polycarbonate Panels Industry Segmentation

-

1. Type

- 1.1. Solid

- 1.2. Corrugated

- 1.3. Multi-walled

-

2. End-user Industry

- 2.1. Construction

- 2.2. Aerospace

- 2.3. Automotive

- 2.4. Agriculture

- 2.5. Electrical and Electronics

- 2.6. Other End-user Industries

Europe Polycarbonate Panels Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Benelux

- 7. Nordic Countries

- 8. Turkey

- 9. Rest of Europe

Europe Polycarbonate Panels Industry Regional Market Share

Geographic Coverage of Europe Polycarbonate Panels Industry

Europe Polycarbonate Panels Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.24% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Solid

- 5.1.2. Corrugated

- 5.1.3. Multi-walled

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Construction

- 5.2.2. Aerospace

- 5.2.3. Automotive

- 5.2.4. Agriculture

- 5.2.5. Electrical and Electronics

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Spain

- 5.3.6. Benelux

- 5.3.7. Nordic Countries

- 5.3.8. Turkey

- 5.3.9. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Solid

- 6.1.2. Corrugated

- 6.1.3. Multi-walled

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Construction

- 6.2.2. Aerospace

- 6.2.3. Automotive

- 6.2.4. Agriculture

- 6.2.5. Electrical and Electronics

- 6.2.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Germany Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Solid

- 7.1.2. Corrugated

- 7.1.3. Multi-walled

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Construction

- 7.2.2. Aerospace

- 7.2.3. Automotive

- 7.2.4. Agriculture

- 7.2.5. Electrical and Electronics

- 7.2.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. United Kingdom Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Solid

- 8.1.2. Corrugated

- 8.1.3. Multi-walled

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Construction

- 8.2.2. Aerospace

- 8.2.3. Automotive

- 8.2.4. Agriculture

- 8.2.5. Electrical and Electronics

- 8.2.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. France Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Solid

- 9.1.2. Corrugated

- 9.1.3. Multi-walled

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Construction

- 9.2.2. Aerospace

- 9.2.3. Automotive

- 9.2.4. Agriculture

- 9.2.5. Electrical and Electronics

- 9.2.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Italy Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Solid

- 10.1.2. Corrugated

- 10.1.3. Multi-walled

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Construction

- 10.2.2. Aerospace

- 10.2.3. Automotive

- 10.2.4. Agriculture

- 10.2.5. Electrical and Electronics

- 10.2.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Spain Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Solid

- 11.1.2. Corrugated

- 11.1.3. Multi-walled

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Construction

- 11.2.2. Aerospace

- 11.2.3. Automotive

- 11.2.4. Agriculture

- 11.2.5. Electrical and Electronics

- 11.2.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Benelux Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Solid

- 12.1.2. Corrugated

- 12.1.3. Multi-walled

- 12.2. Market Analysis, Insights and Forecast - by End-user Industry

- 12.2.1. Construction

- 12.2.2. Aerospace

- 12.2.3. Automotive

- 12.2.4. Agriculture

- 12.2.5. Electrical and Electronics

- 12.2.6. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Nordic Countries Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Type

- 13.1.1. Solid

- 13.1.2. Corrugated

- 13.1.3. Multi-walled

- 13.2. Market Analysis, Insights and Forecast - by End-user Industry

- 13.2.1. Construction

- 13.2.2. Aerospace

- 13.2.3. Automotive

- 13.2.4. Agriculture

- 13.2.5. Electrical and Electronics

- 13.2.6. Other End-user Industries

- 13.1. Market Analysis, Insights and Forecast - by Type

- 14. Turkey Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Type

- 14.1.1. Solid

- 14.1.2. Corrugated

- 14.1.3. Multi-walled

- 14.2. Market Analysis, Insights and Forecast - by End-user Industry

- 14.2.1. Construction

- 14.2.2. Aerospace

- 14.2.3. Automotive

- 14.2.4. Agriculture

- 14.2.5. Electrical and Electronics

- 14.2.6. Other End-user Industries

- 14.1. Market Analysis, Insights and Forecast - by Type

- 15. Rest of Europe Europe Polycarbonate Panels Industry Analysis, Insights and Forecast, 2020-2032

- 15.1. Market Analysis, Insights and Forecast - by Type

- 15.1.1. Solid

- 15.1.2. Corrugated

- 15.1.3. Multi-walled

- 15.2. Market Analysis, Insights and Forecast - by End-user Industry

- 15.2.1. Construction

- 15.2.2. Aerospace

- 15.2.3. Automotive

- 15.2.4. Agriculture

- 15.2.5. Electrical and Electronics

- 15.2.6. Other End-user Industries

- 15.1. Market Analysis, Insights and Forecast - by Type

- 16. Competitive Analysis

- 16.1. Company Profiles

- 16.1.1 3A Composites GmbH

- 16.1.1.1. Company Overview

- 16.1.1.2. Products

- 16.1.1.3. Company Financials

- 16.1.1.4. SWOT Analysis

- 16.1.2 AKRAPLAST Sistemi Srl

- 16.1.2.1. Company Overview

- 16.1.2.2. Products

- 16.1.2.3. Company Financials

- 16.1.2.4. SWOT Analysis

- 16.1.3 Arla Plast

- 16.1.3.1. Company Overview

- 16.1.3.2. Products

- 16.1.3.3. Company Financials

- 16.1.3.4. SWOT Analysis

- 16.1.4 Brett Martin

- 16.1.4.1. Company Overview

- 16.1.4.2. Products

- 16.1.4.3. Company Financials

- 16.1.4.4. SWOT Analysis

- 16.1.5 Carboplak

- 16.1.5.1. Company Overview

- 16.1.5.2. Products

- 16.1.5.3. Company Financials

- 16.1.5.4. SWOT Analysis

- 16.1.6 Corplex

- 16.1.6.1. Company Overview

- 16.1.6.2. Products

- 16.1.6.3. Company Financials

- 16.1.6.4. SWOT Analysis

- 16.1.7 Danpal

- 16.1.7.1. Company Overview

- 16.1.7.2. Products

- 16.1.7.3. Company Financials

- 16.1.7.4. SWOT Analysis

- 16.1.8 dott gallina Srl

- 16.1.8.1. Company Overview

- 16.1.8.2. Products

- 16.1.8.3. Company Financials

- 16.1.8.4. SWOT Analysis

- 16.1.9 EXOLON GROUP

- 16.1.9.1. Company Overview

- 16.1.9.2. Products

- 16.1.9.3. Company Financials

- 16.1.9.4. SWOT Analysis

- 16.1.10 GI PLAST

- 16.1.10.1. Company Overview

- 16.1.10.2. Products

- 16.1.10.3. Company Financials

- 16.1.10.4. SWOT Analysis

- 16.1.11 Isik Plastik

- 16.1.11.1. Company Overview

- 16.1.11.2. Products

- 16.1.11.3. Company Financials

- 16.1.11.4. SWOT Analysis

- 16.1.12 NUDEC S A

- 16.1.12.1. Company Overview

- 16.1.12.2. Products

- 16.1.12.3. Company Financials

- 16.1.12.4. SWOT Analysis

- 16.1.13 Onduline

- 16.1.13.1. Company Overview

- 16.1.13.2. Products

- 16.1.13.3. Company Financials

- 16.1.13.4. SWOT Analysis

- 16.1.14 Palram Industries Ltd

- 16.1.14.1. Company Overview

- 16.1.14.2. Products

- 16.1.14.3. Company Financials

- 16.1.14.4. SWOT Analysis

- 16.1.15 PLAZIT-POLYGAL

- 16.1.15.1. Company Overview

- 16.1.15.2. Products

- 16.1.15.3. Company Financials

- 16.1.15.4. SWOT Analysis

- 16.1.16 Rodeca

- 16.1.16.1. Company Overview

- 16.1.16.2. Products

- 16.1.16.3. Company Financials

- 16.1.16.4. SWOT Analysis

- 16.1.17 SABIC

- 16.1.17.1. Company Overview

- 16.1.17.2. Products

- 16.1.17.3. Company Financials

- 16.1.17.4. SWOT Analysis

- 16.1.18 SafPlast Innovative

- 16.1.18.1. Company Overview

- 16.1.18.2. Products

- 16.1.18.3. Company Financials

- 16.1.18.4. SWOT Analysis

- 16.1.19 Sintostamp SpA

- 16.1.19.1. Company Overview

- 16.1.19.2. Products

- 16.1.19.3. Company Financials

- 16.1.19.4. SWOT Analysis

- 16.1.20 Sümer Plastik

- 16.1.20.1. Company Overview

- 16.1.20.2. Products

- 16.1.20.3. Company Financials

- 16.1.20.4. SWOT Analysis

- 16.1.21 WZD Sp z o o *List Not Exhaustive

- 16.1.21.1. Company Overview

- 16.1.21.2. Products

- 16.1.21.3. Company Financials

- 16.1.21.4. SWOT Analysis

- 16.1.1 3A Composites GmbH

- 16.2. Market Entropy

- 16.2.1 Company's Key Areas Served

- 16.2.2 Recent Developments

- 16.3. Company Market Share Analysis 2025

- 16.3.1 Top 5 Companies Market Share Analysis

- 16.3.2 Top 3 Companies Market Share Analysis

- 16.4. List of Potential Customers

- 17. Research Methodology

List of Figures

- Figure 1: Global Europe Polycarbonate Panels Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Germany Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: Germany Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Germany Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Germany Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Germany Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Germany Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: United Kingdom Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: United Kingdom Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: United Kingdom Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: United Kingdom Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: United Kingdom Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: United Kingdom Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: France Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: France Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: France Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: France Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: France Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: France Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Italy Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Italy Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Italy Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Italy Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Italy Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Italy Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Spain Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Spain Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Spain Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Spain Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Spain Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Spain Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Benelux Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 33: Benelux Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 34: Benelux Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 35: Benelux Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 36: Benelux Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 37: Benelux Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Nordic Countries Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 39: Nordic Countries Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 40: Nordic Countries Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 41: Nordic Countries Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 42: Nordic Countries Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 43: Nordic Countries Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 44: Turkey Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 45: Turkey Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 46: Turkey Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 47: Turkey Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 48: Turkey Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 49: Turkey Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Rest of Europe Europe Polycarbonate Panels Industry Revenue (billion), by Type 2025 & 2033

- Figure 51: Rest of Europe Europe Polycarbonate Panels Industry Revenue Share (%), by Type 2025 & 2033

- Figure 52: Rest of Europe Europe Polycarbonate Panels Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 53: Rest of Europe Europe Polycarbonate Panels Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 54: Rest of Europe Europe Polycarbonate Panels Industry Revenue (billion), by Country 2025 & 2033

- Figure 55: Rest of Europe Europe Polycarbonate Panels Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 9: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 21: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 24: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 27: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 30: Global Europe Polycarbonate Panels Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Polycarbonate Panels Industry?

The projected CAGR is approximately 5.24%.

2. Which companies are prominent players in the Europe Polycarbonate Panels Industry?

Key companies in the market include 3A Composites GmbH, AKRAPLAST Sistemi Srl, Arla Plast, Brett Martin, Carboplak, Corplex, Danpal, dott gallina Srl, EXOLON GROUP, GI PLAST, Isik Plastik, NUDEC S A, Onduline, Palram Industries Ltd, PLAZIT-POLYGAL, Rodeca, SABIC, SafPlast Innovative, Sintostamp SpA, Sümer Plastik, WZD Sp z o o *List Not Exhaustive.

3. What are the main segments of the Europe Polycarbonate Panels Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Revival of the Construction Industry in European Countries; Increasing Popularity of Polycarbonate Against Conventional Materials.

6. What are the notable trends driving market growth?

Increasing Demand from the Construction Industry.

7. Are there any restraints impacting market growth?

Revival of the Construction Industry in European Countries; Increasing Popularity of Polycarbonate Against Conventional Materials.

8. Can you provide examples of recent developments in the market?

September 2022: Brett Martin launched Marlon BioPlus, an innovative polycarbonate sheet from the company offering dramatically reduced environmental impact by switching from fossil-based resins to certified as 71% bio-circular through a mass balancing manufacturing process.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Polycarbonate Panels Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Polycarbonate Panels Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Polycarbonate Panels Industry?

To stay informed about further developments, trends, and reports in the Europe Polycarbonate Panels Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence