Key Insights

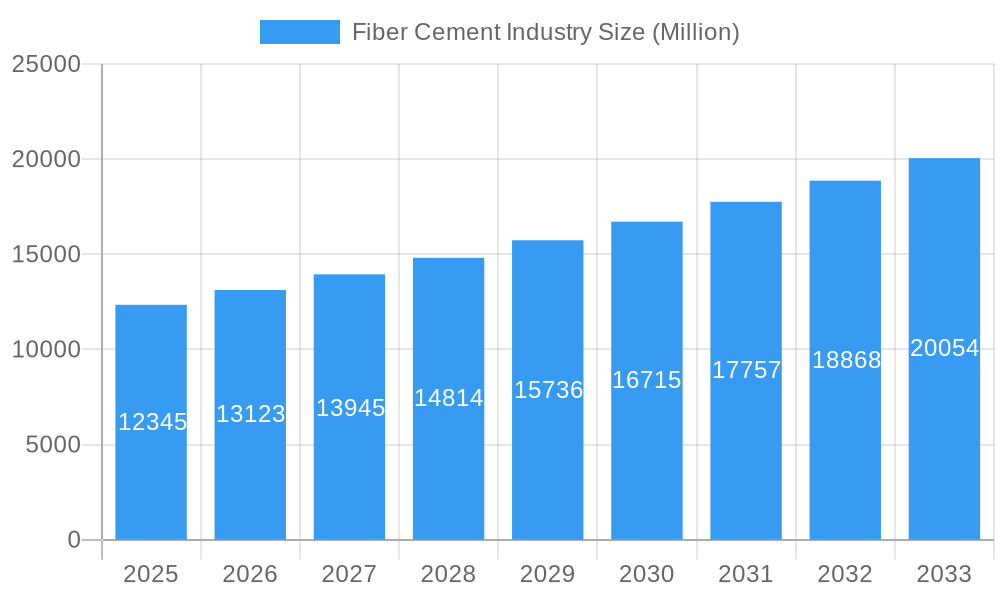

The global Fiber Cement market is poised for significant expansion, projected to reach an estimated XX million USD by 2025, with a robust Compound Annual Growth Rate (CAGR) exceeding 6.00% throughout the forecast period of 2025-2033. This upward trajectory is primarily fueled by a growing demand for durable, low-maintenance building materials, especially in the face of increasing urbanization and a need for sustainable construction solutions. Key drivers include the material's inherent resistance to fire, moisture, pests, and extreme weather conditions, making it an attractive alternative to traditional materials like wood and vinyl siding. The rising adoption of fiber cement in various construction applications, from residential siding and roofing to commercial and infrastructure projects, underscores its versatility and increasing market acceptance. Furthermore, advancements in manufacturing processes are leading to more aesthetically pleasing and diverse product offerings, further stimulating market growth. The market is also benefiting from government initiatives promoting green building practices and the use of eco-friendly materials.

Fiber Cement Industry Market Size (In Billion)

The market’s growth is strategically segmented across diverse end-use sectors and applications. The Commercial, Industrial, and Institutional segment, along with the Infrastructure sector, are expected to be significant contributors, driven by large-scale construction and renovation projects. Residential applications, particularly siding, molding, and trimming, also represent a substantial and growing segment, reflecting homeowner preference for long-lasting and aesthetically appealing exterior finishes. Trends such as the increasing use of fiber cement in modern architectural designs and the development of innovative product features, including enhanced insulation properties and a wider range of textures and colors, are shaping market dynamics. However, potential restraints, such as the initial higher cost compared to some conventional materials and the need for specialized installation expertise, could pose challenges. Despite these, the long-term benefits of fiber cement, including its durability and low lifecycle costs, are expected to outweigh these concerns, ensuring sustained market expansion. Key players like Etex Group, Swisspearl Group A, Saint-Gobain, and James Hardie Building Products Inc. are actively investing in product innovation and market penetration to capitalize on these growth opportunities.

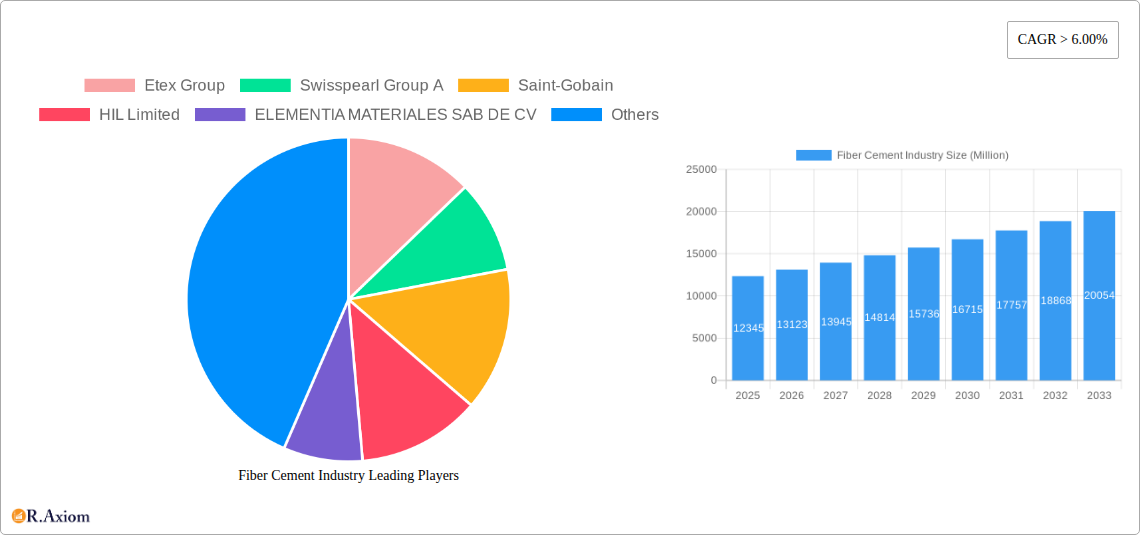

Fiber Cement Industry Company Market Share

This comprehensive report delves into the intricate landscape of the global fiber cement industry, providing an in-depth analysis of its market concentration, innovation drivers, industry trends, dominant markets, and future growth potential. Covering a study period of 2019–2033, with a base and estimated year of 2025 and a forecast period from 2025–2033, this report leverages historical data from 2019–2024 to offer actionable insights for industry stakeholders. With a projected market size in the tens of billions of dollars and a CAGR of xx%, the fiber cement market is poised for significant expansion, driven by sustainability initiatives, product innovation, and increasing demand in residential and commercial construction.

Fiber Cement Industry Market Concentration & Innovation

The fiber cement market exhibits moderate to high concentration, with key players like James Hardie Building Products Inc., Etex Group, and Saint-Gobain holding substantial market shares, estimated to be in the range of 20-30% collectively for the top three. Innovation is a critical driver, fueled by the demand for durable, weather-resistant, and aesthetically versatile building materials. Emerging technologies focus on lighter formulations, enhanced fire resistance, and improved sustainability credentials, contributing to the development of novel fiber cement siding, cladding, and roofing solutions. Regulatory frameworks promoting energy efficiency and sustainable construction practices are indirectly boosting the adoption of fiber cement. Product substitutes, such as vinyl siding and engineered wood, present a competitive challenge, yet the superior longevity and fire resistance of fiber cement often provide a distinct advantage. End-user trends are increasingly favoring materials that offer low maintenance, aesthetic flexibility, and long-term value, aligning perfectly with fiber cement's inherent benefits. Mergers and acquisitions (M&A) play a significant role in market consolidation and expansion. For instance, Saint-Gobain's acquisition of Hume Cemboard Industries Sdn Bhd (HCBI) signifies a strategic move to enhance its sustainable construction portfolio. Estimated M&A deal values are in the range of hundreds of millions of dollars for significant acquisitions, impacting market dynamics and widening the reach of established players.

Fiber Cement Industry Industry Trends & Insights

The global fiber cement market is experiencing robust growth, propelled by an increasing global demand for sustainable and durable building materials. The compound annual growth rate (CAGR) is projected to be approximately xx% over the forecast period. Key growth drivers include the rising urbanization, coupled with significant infrastructure development across emerging economies, particularly in Asia-Pacific and Latin America. The growing awareness of environmental concerns and the push for energy-efficient buildings are also contributing to the adoption of fiber cement, as it offers excellent insulation properties and a long service life, reducing the need for frequent replacements. Technological advancements are revolutionizing product offerings, leading to the development of lighter, stronger, and more aesthetically appealing fiber cement products. These innovations cater to evolving consumer preferences for customizable and visually appealing building exteriors. The competitive landscape is intensifying, with manufacturers focusing on product differentiation, cost optimization, and expanding their distribution networks. Market penetration for fiber cement in developed regions like North America and Europe is already substantial, estimated to be over xx% in new residential construction, while emerging markets present significant untapped potential. The shift towards pre-fabricated construction and modular building systems further supports the demand for fiber cement components due to their ease of installation and dimensional stability. Furthermore, the increasing demand for low-maintenance and weather-resistant building materials, particularly in regions prone to extreme weather conditions, is a significant contributor to market expansion. The industry is witnessing a trend towards more eco-friendly manufacturing processes, with a focus on reducing energy consumption and waste generation.

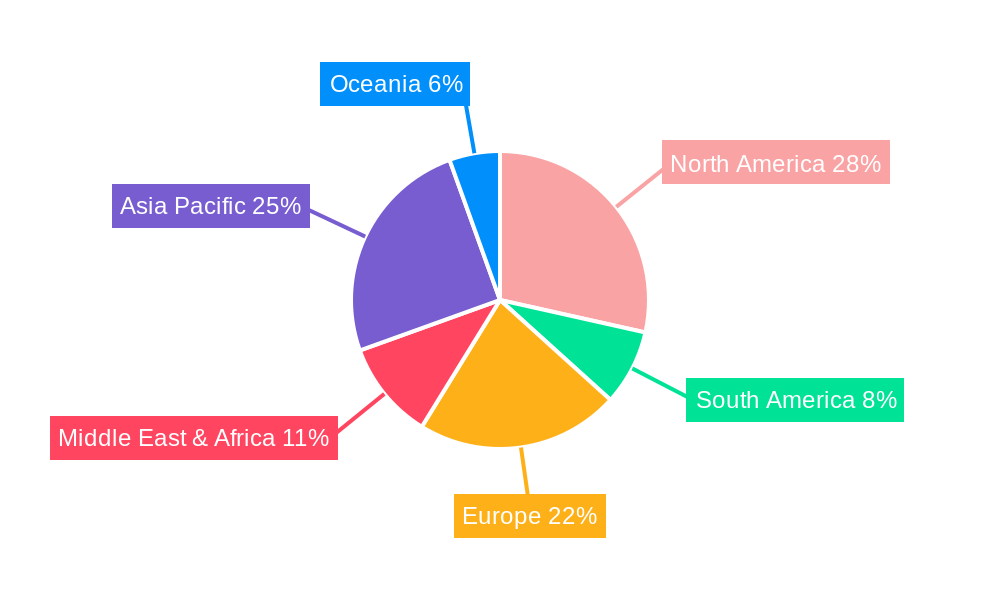

Dominant Markets & Segments in Fiber Cement Industry

The fiber cement industry is witnessing significant dominance across various geographical regions and application segments. North America, particularly the United States, stands out as a leading market, driven by a strong existing housing stock requiring renovations and a robust new construction sector. The Residential end-use sector is a primary consumer, accounting for an estimated xx% of the total market share, propelled by homeowner preferences for durability, aesthetics, and low maintenance. Within applications, Siding represents the largest segment, estimated at xx% of the market, due to its widespread use in exterior wall finishes. The Infrastructure end-use sector is also showing considerable growth, with fiber cement materials being increasingly specified for bridge components, utility poles, and other civil engineering applications, benefiting from their longevity and resistance to environmental degradation. Economic policies promoting green building standards and incentives for energy-efficient construction further bolster demand. For example, government initiatives in the United States encouraging sustainable housing development directly benefit the fiber cement market.

- Leading Region: North America, with an estimated market share of xx%, is the dominant region.

- Key Drivers: High disposable incomes, strong renovation market, stringent building codes promoting durable materials, and significant new residential construction.

- Dominant End Use Sector: Residential, accounting for approximately xx% of the market.

- Key Drivers: Increasing demand for aesthetically pleasing and low-maintenance home exteriors, growing preference for sustainable building materials, and the long lifespan of fiber cement products.

- Dominant Application: Siding, representing an estimated xx% of the market.

- Key Drivers: Superior weather resistance, fire retardancy, versatility in design options, and cost-effectiveness over the product's lifecycle compared to traditional materials.

- Emerging Sector: Infrastructure.

- Key Drivers: Government investment in infrastructure projects, demand for durable and low-maintenance materials in challenging environments, and increasing adoption in utility and civil engineering applications.

Fiber Cement Industry Product Developments

Product innovation in the fiber cement industry is centered on enhancing performance and expanding applications. Manufacturers are developing lighter, stronger fiber cement boards and panels with improved fire and moisture resistance. Advanced formulations are enabling greater design flexibility, offering a wider range of textures, colors, and finishes that mimic natural materials like wood and stone. These developments provide architects and builders with more aesthetic choices and address the growing demand for visually appealing, yet highly functional, building materials. The competitive advantage lies in offering solutions that are not only durable and weather-resistant but also contribute to sustainable building practices, such as improved insulation and longer product lifecycles, reducing the overall environmental footprint of construction projects.

Report Scope & Segmentation Analysis

This report meticulously segments the fiber cement industry across critical dimensions to provide a granular understanding of market dynamics.

End Use Sectors:

- Commercial: Encompasses office buildings, retail spaces, and hospitality venues. This segment is projected to grow at a CAGR of xx%, driven by the construction of new commercial spaces and renovations demanding durable and fire-resistant materials.

- Industrial and Institutional: Includes factories, warehouses, schools, and hospitals. Expected to grow at a CAGR of xx%, fueled by the need for robust and low-maintenance materials in demanding environments.

- Infrastructure: Covers bridges, tunnels, and public utilities. This segment, with an anticipated CAGR of xx%, is benefiting from government investments in infrastructure and the demand for long-lasting, weather-resistant solutions.

- Residential: Addresses single-family homes, multi-family dwellings, and apartments. This is the largest segment, with a projected CAGR of xx%, driven by new home construction, renovations, and homeowner preference for aesthetics and durability.

Applications:

- Cladding: Exterior wall coverings. This segment, projected at xx% market share, is crucial for both aesthetics and protection.

- Molding and Trimming: Decorative and functional elements around windows, doors, and eaves. Estimated at xx% market share, it benefits from the demand for durable and weather-resistant finishing touches.

- Roofing: Fiber cement roofing tiles and shingles. This segment, with xx% projected market share, offers a durable and fire-resistant alternative to traditional roofing materials.

- Siding: Exterior wall panels. The largest application segment at xx% market share, it remains a primary driver for fiber cement adoption due to its versatility and performance.

- Other Applications: Includes soffits, fascia, fencing, and interior panels. This segment, with xx% projected growth, is expanding as new uses are discovered and implemented.

Key Drivers of Fiber Cement Industry Growth

The fiber cement industry's growth is primarily propelled by several key factors:

- Sustainability and Durability: Increasing global emphasis on eco-friendly construction materials and the inherent long lifespan and low maintenance requirements of fiber cement products are major drivers.

- Technological Advancements: Innovations in manufacturing processes and product formulations are leading to lighter, stronger, and more aesthetically versatile fiber cement materials.

- Growing Construction Activity: Rising urbanization, infrastructure development, and a robust housing market, particularly in emerging economies, are significantly boosting demand for construction materials like fiber cement.

- Regulatory Support: Favorable building codes and government incentives promoting energy efficiency and sustainable construction practices indirectly benefit the adoption of fiber cement.

Challenges in the Fiber Cement Industry Sector

Despite its growth trajectory, the fiber cement industry faces several challenges:

- Cost Competitiveness: While offering long-term value, the initial installation cost of fiber cement can be higher compared to some alternative materials, posing a barrier for budget-conscious projects.

- Supply Chain Volatility: Global supply chain disruptions and the fluctuating costs of raw materials, such as cement, silica, and cellulose fibers, can impact production costs and availability.

- Skilled Labor Requirements: Installation of fiber cement products often requires specialized skills and tools, which can lead to higher labor costs and potential shortages of qualified installers in certain regions.

- Competition from Substitutes: The availability of a wide range of alternative building materials, such as vinyl, wood composites, and metal, presents ongoing competitive pressure.

Emerging Opportunities in Fiber Cement Industry

The fiber cement industry is ripe with emerging opportunities:

- Expansion in Emerging Markets: Significant untapped potential exists in developing economies across Asia, Africa, and Latin America, where rapid urbanization and infrastructure development are creating substantial demand for building materials.

- Development of Smart Building Materials: Integrating IoT capabilities or advanced insulation properties into fiber cement products can open new avenues for innovation and higher-value applications.

- Focus on Recycled Content and Circular Economy: Developing fiber cement products with a higher percentage of recycled content and exploring end-of-life recycling solutions aligns with growing sustainability demands and can create a competitive advantage.

- Customization and Aesthetic Solutions: Meeting the increasing consumer desire for personalized and aesthetically diverse building exteriors through advanced manufacturing techniques and a wider palette of finishes and textures.

Leading Players in the Fiber Cement Industry Market

- Etex Group

- Swisspearl Group A

- Saint-Gobain

- HIL Limited

- ELEMENTIA MATERIALES SAB DE CV

- NICHIHA Co Ltd

- James Hardie Building Products Inc.

- SHERA Public Company Limited

- SCG

- CSR Limited

Key Developments in Fiber Cement Industry Industry

- October 2023: James Hardie Building Products Inc. partnered with D.R. Horton, Inc., the largest homebuilder in the United States, to provide premier quality and innovative fiber cement solutions to home construction across the United States. This collaboration aims to enhance the availability and adoption of high-performance fiber cement products in a significant segment of the residential construction market.

- June 2023: Saint-Gobain has entered into a definitive agreement to acquire Hume Cemboard Industries Sdn Bhd (HCBI), a manufacturer of fiber cement boards for façades, partitions, and ceilings, to expand its growth by enriching its range of solutions for light and sustainable construction in Malaysia. This strategic acquisition strengthens Saint-Gobain's position in the Asian market and its commitment to sustainable building solutions.

- April 2023: BlueLinx Holdings Inc., a leading wholesale distributor of building products in the United States, and Allura USA, a subsidiary of Elementia Materiales, announced the expansion of their distribution partnership to maintain growth in the highly competitive landscape of fiber cement siding, trim, and accessories. This expanded partnership is expected to improve product availability and strengthen market penetration for Allura USA's fiber cement offerings.

Strategic Outlook for Fiber Cement Industry Market

The strategic outlook for the fiber cement industry is overwhelmingly positive, fueled by a confluence of factors that position it for sustained growth and innovation. The increasing global imperative for sustainable and durable building solutions aligns perfectly with the inherent advantages of fiber cement products, driving demand across residential, commercial, and infrastructure sectors. Investments in research and development for lighter, more aesthetically versatile, and environmentally conscious fiber cement formulations will continue to be a critical differentiator. Expansion into burgeoning emerging markets, coupled with strategic partnerships and potential M&A activities, will further consolidate market share and drive geographical penetration. The industry's ability to adapt to evolving regulatory landscapes, embrace circular economy principles, and cater to the growing demand for customizable and high-performance building materials will be paramount to capturing future market opportunities and solidifying its position as a leading material in modern construction.

Fiber Cement Industry Segmentation

-

1. End Use Sector

- 1.1. Commercial

- 1.2. Industrial and Institutional

- 1.3. Infrastructure

- 1.4. Residential

-

2. Application

- 2.1. Cladding

- 2.2. Molding and Trimming

- 2.3. Roofing

- 2.4. Siding

- 2.5. Other Applications

Fiber Cement Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fiber Cement Industry Regional Market Share

Geographic Coverage of Fiber Cement Industry

Fiber Cement Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 6.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End Use Sector

- 5.1.1. Commercial

- 5.1.2. Industrial and Institutional

- 5.1.3. Infrastructure

- 5.1.4. Residential

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Cladding

- 5.2.2. Molding and Trimming

- 5.2.3. Roofing

- 5.2.4. Siding

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by End Use Sector

- 6. Global Fiber Cement Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End Use Sector

- 6.1.1. Commercial

- 6.1.2. Industrial and Institutional

- 6.1.3. Infrastructure

- 6.1.4. Residential

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Cladding

- 6.2.2. Molding and Trimming

- 6.2.3. Roofing

- 6.2.4. Siding

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by End Use Sector

- 7. North America Fiber Cement Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End Use Sector

- 7.1.1. Commercial

- 7.1.2. Industrial and Institutional

- 7.1.3. Infrastructure

- 7.1.4. Residential

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Cladding

- 7.2.2. Molding and Trimming

- 7.2.3. Roofing

- 7.2.4. Siding

- 7.2.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by End Use Sector

- 8. South America Fiber Cement Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End Use Sector

- 8.1.1. Commercial

- 8.1.2. Industrial and Institutional

- 8.1.3. Infrastructure

- 8.1.4. Residential

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Cladding

- 8.2.2. Molding and Trimming

- 8.2.3. Roofing

- 8.2.4. Siding

- 8.2.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by End Use Sector

- 9. Europe Fiber Cement Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End Use Sector

- 9.1.1. Commercial

- 9.1.2. Industrial and Institutional

- 9.1.3. Infrastructure

- 9.1.4. Residential

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Cladding

- 9.2.2. Molding and Trimming

- 9.2.3. Roofing

- 9.2.4. Siding

- 9.2.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by End Use Sector

- 10. Middle East & Africa Fiber Cement Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End Use Sector

- 10.1.1. Commercial

- 10.1.2. Industrial and Institutional

- 10.1.3. Infrastructure

- 10.1.4. Residential

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Cladding

- 10.2.2. Molding and Trimming

- 10.2.3. Roofing

- 10.2.4. Siding

- 10.2.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by End Use Sector

- 11. Asia Pacific Fiber Cement Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by End Use Sector

- 11.1.1. Commercial

- 11.1.2. Industrial and Institutional

- 11.1.3. Infrastructure

- 11.1.4. Residential

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Cladding

- 11.2.2. Molding and Trimming

- 11.2.3. Roofing

- 11.2.4. Siding

- 11.2.5. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by End Use Sector

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Etex Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Swisspearl Group A

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Saint-Gobain

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 HIL Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 ELEMENTIA MATERIALES SAB DE CV

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NICHIHA Co Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 James Hardie Building Products Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SHERA Public Company Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SCG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 CSR Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Etex Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fiber Cement Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Fiber Cement Industry Revenue (Million), by End Use Sector 2025 & 2033

- Figure 3: North America Fiber Cement Industry Revenue Share (%), by End Use Sector 2025 & 2033

- Figure 4: North America Fiber Cement Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Fiber Cement Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Fiber Cement Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Fiber Cement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fiber Cement Industry Revenue (Million), by End Use Sector 2025 & 2033

- Figure 9: South America Fiber Cement Industry Revenue Share (%), by End Use Sector 2025 & 2033

- Figure 10: South America Fiber Cement Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: South America Fiber Cement Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: South America Fiber Cement Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: South America Fiber Cement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fiber Cement Industry Revenue (Million), by End Use Sector 2025 & 2033

- Figure 15: Europe Fiber Cement Industry Revenue Share (%), by End Use Sector 2025 & 2033

- Figure 16: Europe Fiber Cement Industry Revenue (Million), by Application 2025 & 2033

- Figure 17: Europe Fiber Cement Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Fiber Cement Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Fiber Cement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fiber Cement Industry Revenue (Million), by End Use Sector 2025 & 2033

- Figure 21: Middle East & Africa Fiber Cement Industry Revenue Share (%), by End Use Sector 2025 & 2033

- Figure 22: Middle East & Africa Fiber Cement Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Middle East & Africa Fiber Cement Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East & Africa Fiber Cement Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fiber Cement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fiber Cement Industry Revenue (Million), by End Use Sector 2025 & 2033

- Figure 27: Asia Pacific Fiber Cement Industry Revenue Share (%), by End Use Sector 2025 & 2033

- Figure 28: Asia Pacific Fiber Cement Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Asia Pacific Fiber Cement Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Fiber Cement Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Fiber Cement Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fiber Cement Industry Revenue Million Forecast, by End Use Sector 2020 & 2033

- Table 2: Global Fiber Cement Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Fiber Cement Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Fiber Cement Industry Revenue Million Forecast, by End Use Sector 2020 & 2033

- Table 5: Global Fiber Cement Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Fiber Cement Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Fiber Cement Industry Revenue Million Forecast, by End Use Sector 2020 & 2033

- Table 11: Global Fiber Cement Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Fiber Cement Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Fiber Cement Industry Revenue Million Forecast, by End Use Sector 2020 & 2033

- Table 17: Global Fiber Cement Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 18: Global Fiber Cement Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Fiber Cement Industry Revenue Million Forecast, by End Use Sector 2020 & 2033

- Table 29: Global Fiber Cement Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 30: Global Fiber Cement Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Fiber Cement Industry Revenue Million Forecast, by End Use Sector 2020 & 2033

- Table 38: Global Fiber Cement Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 39: Global Fiber Cement Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fiber Cement Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fiber Cement Industry?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the Fiber Cement Industry?

Key companies in the market include Etex Group, Swisspearl Group A, Saint-Gobain, HIL Limited, ELEMENTIA MATERIALES SAB DE CV, NICHIHA Co Ltd, James Hardie Building Products Inc, SHERA Public Company Limited, SCG, CSR Limited.

3. What are the main segments of the Fiber Cement Industry?

The market segments include End Use Sector, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Awareness about the Advantages of Industrial Flooring; Increasing Demand from the Food & Beverages Industry.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Stringent Regulations on VOCs Released from Industrial Floorings.

8. Can you provide examples of recent developments in the market?

October 2023: James Hardie Building Products Inc. partnered with D.R. Horton, Inc., the largest homebuilder in the United States, to provide premier quality and innovative fiber cement solutions to home construction across the United States.June 2023: Saint-Gobain has entered into a definitive agreement to acquire Hume Cemboard Industries Sdn Bhd (HCBI), a manufacturer of fiber cement boards for façades, partitions, and ceilings, to expand its growth by enriching its range of solutions for light and sustainable construction in Malaysia.April 2023: BlueLinx Holdings Inc., a leading wholesale distributor of building products in the United States, and Allura USA, a subsidiary of Elementia Materiales, announced the expansion of their distribution partnership to maintain growth in the highly competitive landscape of fiber cement siding, trim, and accessories.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fiber Cement Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fiber Cement Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fiber Cement Industry?

To stay informed about further developments, trends, and reports in the Fiber Cement Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence