Key Insights

The Italian condominiums and apartments market, spanning major urban centers such as Rome, Milan, Venice, and Florence, demonstrates significant expansion potential. With an estimated market size of €1279.93 billion in the base year 2025, and a projected Compound Annual Growth Rate (CAGR) of 4.9%, the sector is poised for sustained growth through 2033. Key growth drivers include a thriving tourism industry stimulating rental property demand, increasing urbanization leading to higher residential density in key cities, and government initiatives promoting sustainable housing developments. Furthermore, market trends are shaped by a growing preference for modern, energy-efficient apartments, alongside the rising popularity of co-living spaces and smart home technology integration. While rising construction costs and labor shortages present challenges, these are expected to be offset by advancements in construction technology and innovative financing. The competitive landscape features established national entities like Facile Ristrutturare SPA and Impresa Tonon SPA, alongside international corporations such as Takenaka Europe GmbH, all competing for market share.

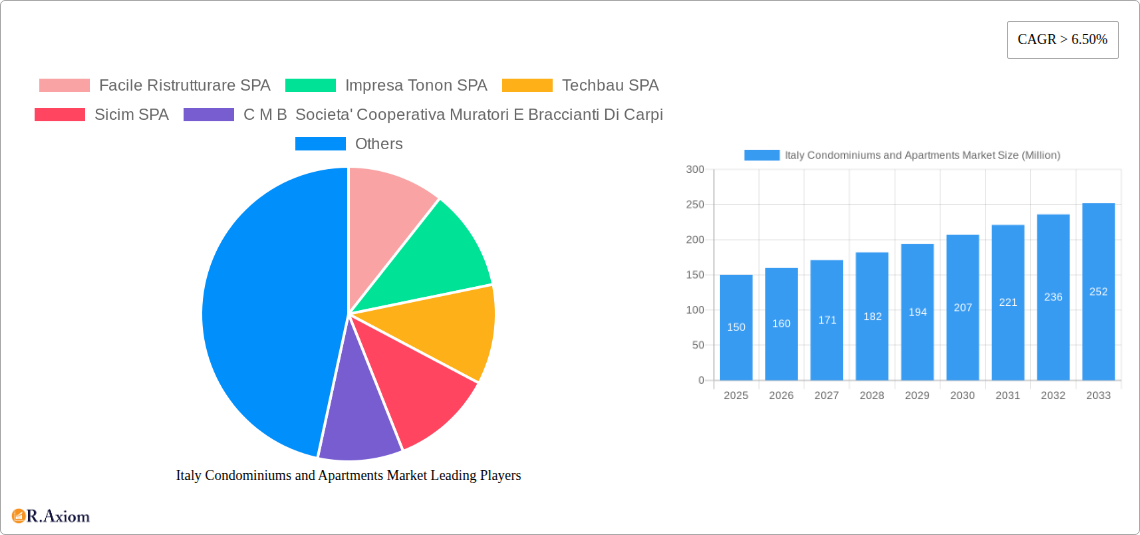

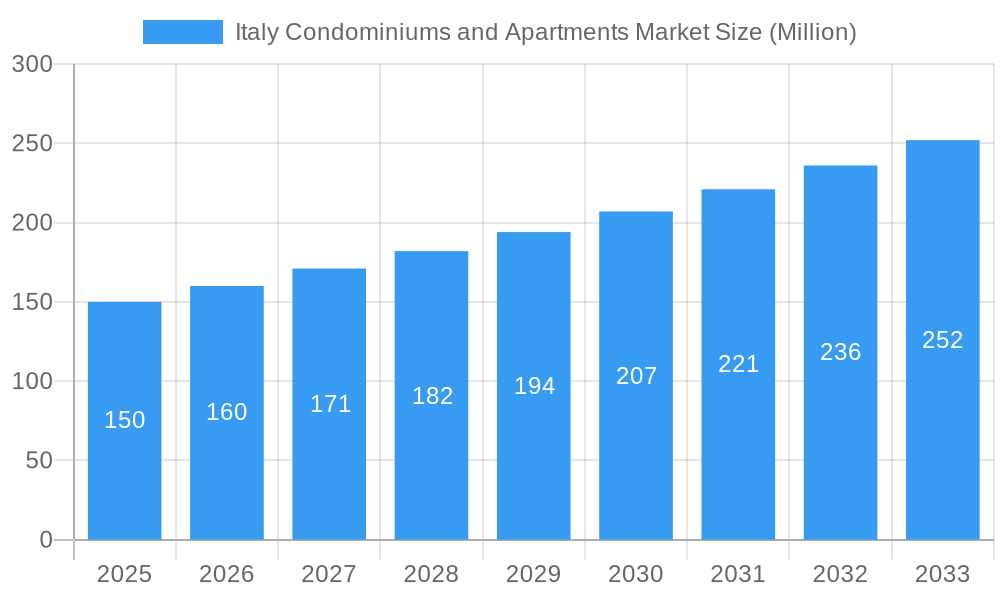

Italy Condominiums and Apartments Market Market Size (In Million)

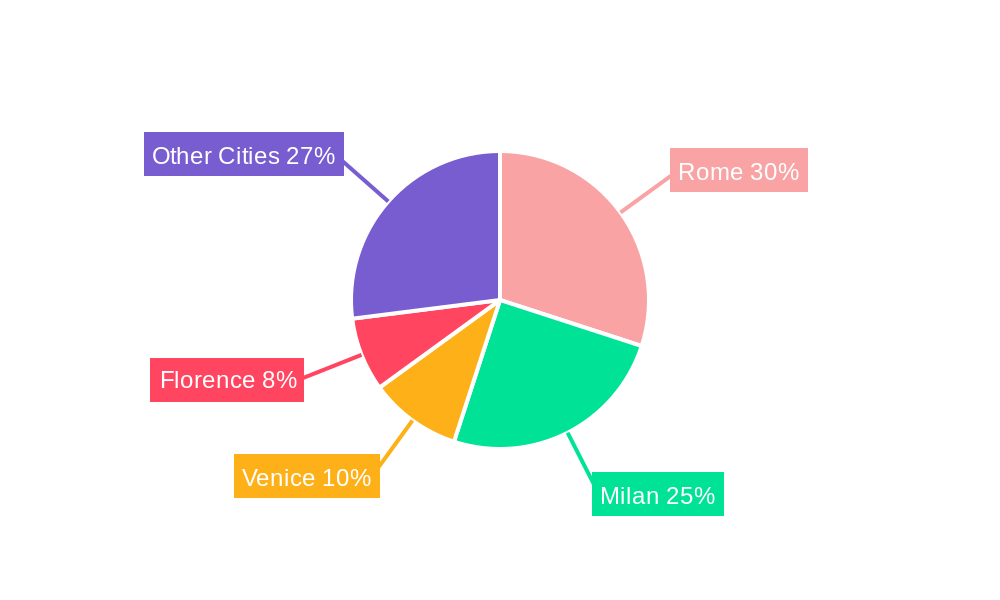

Segment analysis indicates varied market activity across Italian cities. Rome and Milan, as primary metropolitan areas, command the largest market share, followed by Venice and Florence, renowned for their tourist appeal and high property values. The "Other Cities" segment represents a substantial portion of the market, reflecting broader residential development across Italy. The forecast period (2025-2033) anticipates continued growth, fueled by rising disposable incomes, favorable demographic shifts, and ongoing government support for the housing sector. The market's robust fundamentals, coupled with continuous development and adaptation to contemporary trends, present a promising outlook for investors and developers in the Italian condominiums and apartments sector.

Italy Condominiums and Apartments Market Company Market Share

Italy Condominiums and Apartments Market: A Comprehensive Report (2019-2033)

This comprehensive report provides a detailed analysis of the Italy condominiums and apartments market, offering invaluable insights for investors, developers, and industry stakeholders. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report leverages extensive market research and data analysis to deliver actionable intelligence.

Italy Condominiums and Apartments Market Market Concentration & Innovation

The Italian condominiums and apartments market exhibits a moderately concentrated landscape, with a few large players holding significant market share. However, the market is also characterized by a large number of smaller, regional operators. While precise market share figures for individual companies are proprietary, it is observed that companies like Impresa Pizzarotti & C SPA and Salini Costruttori SPA hold substantial influence due to their scale and experience in large-scale projects. The overall market concentration ratio (CR4 or CR8) is estimated to be around xx, indicating a moderate level of competition.

Innovation in the sector is primarily driven by factors like:

- Sustainable construction practices: Increasing adoption of green building technologies and energy-efficient materials.

- Smart home integration: Growing demand for technologically advanced apartments with integrated smart home systems.

- Co-living and co-working spaces: The rise of shared living arrangements is reshaping the rental market.

- Airbnb and short-term rentals: Impacting the overall supply and demand dynamics of the market.

Regulatory frameworks, including building codes and zoning regulations, significantly influence market dynamics. Product substitutes, such as long-term hotel stays or rented houses, pose competitive pressure. End-user trends, including a preference for centrally located properties with modern amenities, strongly shape demand. M&A activity, as seen in recent transactions (detailed in the Key Developments section), indicates consolidation and strategic expansion within the market. The value of these transactions, like the Borgosesia acquisition of Como 11 Srl, range from several Million EUR to tens of Million EUR, reflecting substantial investment in the sector.

Italy Condominiums and Apartments Market Industry Trends & Insights

The Italian condominiums and apartments market is experiencing robust growth, driven by several key factors. Urbanization and population growth in major cities like Rome and Milan are fueling demand for residential properties. Increasing disposable incomes, particularly amongst younger demographics, and a shift in preferences towards modern, comfortable living spaces are contributing to market expansion.

Technological disruptions, such as the rise of proptech platforms and online property portals, are transforming how properties are bought, sold, and managed. The emergence of co-living spaces caters to new lifestyle preferences, influencing both supply and demand. Consumer preferences are shifting toward sustainable, energy-efficient housing, driving demand for green building projects. The competitive dynamics are shaped by the interplay between established developers and emerging proptech companies.

The market is anticipated to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration of smart home technologies is projected to reach xx% by 2033. These trends collectively point towards a dynamic and evolving market with substantial future growth potential.

Dominant Markets & Segments in Italy Condominiums and Apartments Market

Milan and Rome dominate the Italian condominiums and apartments market, driven by several key factors:

- Economic Strength: Both cities are major economic hubs with high concentrations of employment and high purchasing power.

- Tourism: Rome's significant tourism sector creates high demand for short-term rental properties.

- Infrastructure: Well-developed transportation networks and infrastructure support higher property values and demand.

- Lifestyle: Attractive lifestyle and cultural offerings draw residents and investors.

Milan's strong financial sector and high concentration of multinational companies contribute to significant demand for upscale apartments and condominiums. Rome's rich history and tourism sector create high demand for both residential and short-term rental units. Venice, while smaller, holds a unique position due to its iconic appeal, albeit with limited space and higher property prices. Florence also exhibits strong demand, driven by its tourism sector and affluent resident population. While other cities contribute to the overall market, their impact is proportionally smaller compared to Milan and Rome. The key drivers for each city vary, but consistent themes include economic strength, tourism, and the overall desirability of living in these locations.

Italy Condominiums and Apartments Market Product Developments

Recent product innovations focus on sustainable materials, energy-efficient designs, and smart home integration. The market is seeing a growing adoption of prefabricated construction methods to speed up development and reduce costs. These innovations are improving the overall quality and appeal of residential properties, enhancing their market fit and offering developers a competitive advantage. The integration of renewable energy sources, such as solar panels, is becoming increasingly common, reflecting both environmental consciousness and cost savings.

Report Scope & Segmentation Analysis

This report segments the Italy condominiums and apartments market by key city: Rome, Milan, Venice, Florence, and Other Cities.

Rome: The Rome segment is characterized by a high concentration of historical properties, significant tourist activity, and a diverse mix of residential options. The market is expected to show steady growth, driven by ongoing investments in infrastructure and tourism.

Milan: The Milan segment demonstrates strong growth fueled by its robust financial sector and high demand for modern, upscale properties. The market is highly competitive, with numerous developers and a significant influx of high-net-worth individuals.

Venice: The Venice segment is unique due to its limited space and high property values. Growth is expected to be relatively moderate, limited by the city's historical preservation efforts.

Florence: The Florence segment is similar to Venice, with high demand driven by tourism and its appeal as a historical and cultural center. Growth is expected to be moderate but stable.

Other Cities: This segment encompasses all other cities in Italy, representing a significant but more fragmented market. Growth rates will vary considerably among these cities.

Key Drivers of Italy Condominiums and Apartments Market Growth

Several factors are driving growth in the Italian condominiums and apartments market. These include increasing urbanization, a growing population, rising disposable incomes, and favorable government policies promoting real estate investment. Furthermore, technological advancements in construction and property management are enhancing efficiency and market appeal. The continuous inflow of both domestic and international tourism also significantly contributes to the demand for rental properties.

Challenges in the Italy Condominiums and Apartments Market Sector

The Italian condominiums and apartments market faces challenges, including complex bureaucratic processes for obtaining building permits, and high construction costs. The availability of skilled labor remains a constraint, affecting project timelines. The increasing cost of materials also contributes to overall project expenses. Furthermore, intense competition among developers creates pressure on pricing and profitability. These factors can lead to project delays and reduce profit margins.

Emerging Opportunities in Italy Condominiums and Apartments Market

Emerging opportunities lie in sustainable construction practices, smart home technology integration, and the growth of co-living and co-working spaces. The increasing demand for energy-efficient and eco-friendly housing presents significant growth potential for developers adopting green building techniques. The untapped potential of smaller cities outside of the major metropolitan areas also offers opportunities for expansion and diversification.

Leading Players in the Italy Condominiums and Apartments Market Market

- Facile Ristrutturare SPA

- Impresa Tonon SPA

- Techbau SPA

- Sicim SPA

- C M B Societa' Cooperativa Muratori E Braccianti Di Carpi

- Rizzani De Eccher SPA

- Consorzio Integra Soc Coop

- IGEFI SRL

- Impresa Percassi SPA

- Impresa Pizzarotti & C SPA

- Salini Costruttori SPA

- IREM SPA

- Takenaka Europe Gmbh

Key Developments in Italy Condominiums and Apartments Market Industry

- June 2022: Borgosesia acquired Como 11 Srl, adding 13 renovated apartments in Milan for USD 7.5 Million, showcasing strategic investment in prime locations.

- June 2022: DoveVivo's acquisition of ALTIDO significantly expanded its property portfolio by 51 units, bolstering its post-Covid recovery and market position.

Strategic Outlook for Italy Condominiums and Apartments Market Market

The Italian condominiums and apartments market presents a positive outlook, driven by robust economic growth, increasing urbanization, and a preference for modern living spaces. Continued investments in infrastructure, sustainable building practices, and technological innovation will further drive market expansion. Opportunities exist for companies that can successfully navigate regulatory hurdles, manage construction costs, and adapt to evolving consumer preferences. The market's overall trajectory points towards sustained growth and increasing sophistication in both supply and demand.

Italy Condominiums and Apartments Market Segmentation

-

1. Key City

- 1.1. Rome

- 1.2. Milan

- 1.3. Venice

- 1.4. Florence

- 1.5. Other Cities

Italy Condominiums and Apartments Market Segmentation By Geography

- 1. Italy

Italy Condominiums and Apartments Market Regional Market Share

Geographic Coverage of Italy Condominiums and Apartments Market

Italy Condominiums and Apartments Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Key City

- 5.1.1. Rome

- 5.1.2. Milan

- 5.1.3. Venice

- 5.1.4. Florence

- 5.1.5. Other Cities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Italy

- 5.1. Market Analysis, Insights and Forecast - by Key City

- 6. Italy Condominiums and Apartments Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Key City

- 6.1.1. Rome

- 6.1.2. Milan

- 6.1.3. Venice

- 6.1.4. Florence

- 6.1.5. Other Cities

- 6.1. Market Analysis, Insights and Forecast - by Key City

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Facile Ristrutturare SPA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Impresa Tonon SPA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Techbau SPA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Sicim SPA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 C M B Societa' Cooperativa Muratori E Braccianti Di Carpi

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Rizzani De Eccher SPA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Consorzio Integra Soc Coop

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 IGEFI SRL

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Impresa Percassi SPA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Impresa Pizzarotti & C SPA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Salini Costruttori SPA

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 IREM SPA**List Not Exhaustive

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Takenaka Europe Gmbh

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Facile Ristrutturare SPA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italy Condominiums and Apartments Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Italy Condominiums and Apartments Market Share (%) by Company 2025

List of Tables

- Table 1: Italy Condominiums and Apartments Market Revenue billion Forecast, by Key City 2020 & 2033

- Table 2: Italy Condominiums and Apartments Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Italy Condominiums and Apartments Market Revenue billion Forecast, by Key City 2020 & 2033

- Table 4: Italy Condominiums and Apartments Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italy Condominiums and Apartments Market?

The projected CAGR is approximately 4.9%.

2. Which companies are prominent players in the Italy Condominiums and Apartments Market?

Key companies in the market include Facile Ristrutturare SPA, Impresa Tonon SPA, Techbau SPA, Sicim SPA, C M B Societa' Cooperativa Muratori E Braccianti Di Carpi, Rizzani De Eccher SPA, Consorzio Integra Soc Coop, IGEFI SRL, Impresa Percassi SPA, Impresa Pizzarotti & C SPA, Salini Costruttori SPA, IREM SPA**List Not Exhaustive, Takenaka Europe Gmbh.

3. What are the main segments of the Italy Condominiums and Apartments Market?

The market segments include Key City.

4. Can you provide details about the market size?

The market size is estimated to be USD 1279.93 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; The growing number of high-rise buildings and skyscrapers globally has created a robust market for facade systems4.; Building owners and developers are placing greater emphasis on the overall performance of their structures.

6. What are the notable trends driving market growth?

Despite skyrocketing living expenses fueled by high inflation. average home prices in Italy rose..

7. Are there any restraints impacting market growth?

4.; High-quality facade materials and designs can be costly. making it challenging for some projects to meet budget constraint4.; Facades must comply with building codes and safety regulations. which can vary based on location.

8. Can you provide examples of recent developments in the market?

June 2022: Borgosesia purchased the full capital of Como 11 Srl, which owns 13 freshly renovated apartments in Milan's Corso Como, for EUR 7 million (USD 7.5 Million).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italy Condominiums and Apartments Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italy Condominiums and Apartments Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italy Condominiums and Apartments Market?

To stay informed about further developments, trends, and reports in the Italy Condominiums and Apartments Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence