Key Insights

The global Liquid Cooling Rack market is experiencing robust expansion, projected to reach a significant valuation by 2033. This growth is underpinned by a substantial compound annual growth rate (CAGR), indicating a rapidly maturing and increasingly vital segment within the broader IT infrastructure landscape. The primary drivers fueling this surge include the relentless demand for enhanced thermal management solutions in high-density computing environments, such as modern data centers. As processors and other components become more powerful and energy-efficient, they also generate more heat, necessitating advanced cooling techniques beyond traditional air cooling. This is particularly evident in the burgeoning fields of Artificial Intelligence (AI), Machine Learning (ML), and High-Performance Computing (HPC), where intense computational workloads generate considerable thermal loads that liquid cooling is uniquely equipped to handle. Furthermore, the growing emphasis on energy efficiency and sustainability within the IT sector is also a key catalyst, as liquid cooling systems often offer superior energy performance compared to their air-cooled counterparts.

The market is characterized by dynamic trends such as the increasing adoption of direct contact liquid cooling solutions, which offer unparalleled thermal transfer efficiency. These systems are becoming indispensable for high-performance computing clusters and specialized server configurations. Conversely, indirect contact liquid cooling, including immersion cooling techniques, is also gaining traction, particularly for its ability to manage heat across entire server racks and its potential for scalability. While the market presents immense opportunities, certain restraints, such as the initial capital investment for implementing liquid cooling infrastructure and the need for specialized maintenance expertise, may pose challenges to widespread adoption, especially for smaller enterprises. However, the long-term operational cost savings and performance benefits are increasingly outweighing these initial hurdles, paving the way for sustained market growth across diverse applications including laboratories, libraries with specialized computing needs, and industrial workshops.

This in-depth report provides a comprehensive analysis of the global Liquid Cooling Rack market, offering unparalleled insights into market dynamics, growth trajectories, and strategic opportunities. Covering a study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this report is an essential resource for industry stakeholders, investors, and decision-makers seeking to understand and capitalize on the rapidly evolving liquid cooling solutions landscape. We delve into market concentration, key trends, dominant segments, product innovations, and strategic outlooks, supported by robust data and expert analysis.

Liquid Cooling Rack Market Concentration & Innovation

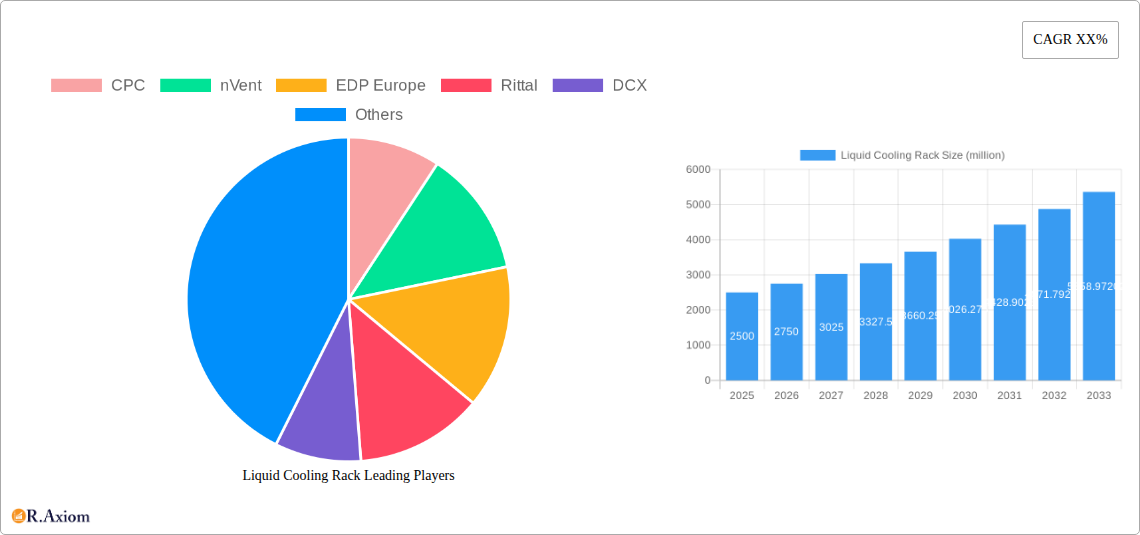

The global Liquid Cooling Rack market exhibits a moderate level of concentration, with a few key players like CPC, nVent, and Rittal holding significant market shares. However, the landscape is dynamically evolving, driven by continuous innovation in direct contact and indirect contact cooling technologies. Regulatory frameworks, particularly concerning energy efficiency and environmental impact in data centers, are increasingly influencing product development and adoption. End-user trends, such as the escalating demand for high-performance computing and AI infrastructure, are significant innovation drivers. The emergence of specialized solutions for laboratories and workshops also contributes to market dynamism. Strategic mergers and acquisitions (M&A) are expected to play a crucial role in market consolidation. For instance, recent M&A activities have seen deal values in the range of approximately $50 million to $150 million, indicating strategic consolidation and investment in this growing sector. Anticipated M&A deals in the forecast period could exceed $200 million, further shaping market structure.

- Innovation Drivers: High-performance computing, AI/ML workloads, energy efficiency mandates, modular data center designs.

- Regulatory Impact: Government incentives for green data centers, stricter emission standards, data center energy usage regulations.

- M&A Activities: Strategic acquisitions of specialized technology providers, partnerships for integrated solutions.

- Market Share Snapshot (Estimated Base Year 2025): Leading players are estimated to hold combined market shares ranging from 60% to 75%.

Liquid Cooling Rack Industry Trends & Insights

The Liquid Cooling Rack industry is poised for substantial growth, driven by the insatiable demand for efficient thermal management solutions in an era of increasingly power-dense computing. The projected Compound Annual Growth Rate (CAGR) for the liquid cooling rack market is estimated to be around 18% to 22% during the forecast period of 2025–2033. This robust growth is fueled by several key factors. Firstly, the exponential increase in data generation and processing power required for artificial intelligence, machine learning, big data analytics, and high-performance computing (HPC) necessitates more advanced cooling solutions than traditional air cooling can provide. Server rack power densities are rapidly increasing, often exceeding 30 kW to 50 kW per rack, making liquid cooling a critical necessity. Secondly, rising energy costs and stringent environmental regulations are compelling data center operators to adopt energy-efficient cooling technologies. Liquid cooling offers significantly better thermal performance, leading to reduced power consumption for cooling systems, potentially lowering Operational Expenditure (OpEx) by 15% to 25% compared to air-cooled equivalents. Market penetration of liquid cooling solutions, which stood at approximately 10% to 15% in 2024, is projected to surge to 30% to 40% by 2033. Technological disruptions, such as advancements in immersion cooling, direct-to-chip liquid cooling, and advanced coolant formulations, are continuously improving efficiency and cost-effectiveness. Consumer preferences are shifting towards integrated, plug-and-play liquid cooling solutions that minimize deployment complexity and maintenance. The competitive landscape is intensifying, with both established IT infrastructure providers and specialized liquid cooling companies vying for market share, leading to a healthy influx of innovative products and services. The market size is projected to grow from an estimated $5 billion in the base year 2025 to over $20 billion by 2033.

Dominant Markets & Segments in Liquid Cooling Rack

The Data Centre application segment stands as the undisputed leader in the global Liquid Cooling Rack market, driven by the relentless expansion of hyperscale, colocation, and enterprise data centers. The sheer density of computing power and the critical need for uninterrupted operation in these environments make advanced thermal management indispensable. Economic policies promoting digital transformation and investment in cloud infrastructure further bolster this segment. The increasing demand for AI and machine learning workloads, requiring high-density GPU and CPU configurations, directly translates into a higher demand for efficient liquid cooling solutions, with rack power densities often exceeding 50 kW. The Indirect Contact type of liquid cooling, including Rear Door Heat Exchangers (RDHx) and direct-to-chip cooling systems, is currently dominating due to its compatibility with existing infrastructure and its ability to address localized heat loads efficiently. However, Direct Contact liquid cooling, particularly immersion cooling (single-phase and two-phase), is gaining significant traction, especially for extremely high-density applications and where maximum energy efficiency is paramount. Countries with robust digital economies, such as the United States, China, and Germany, are leading the adoption of liquid cooling racks, owing to massive data center investments and government initiatives supporting green technology. Infrastructure development, including the availability of sufficient power and water resources for efficient cooling, also plays a critical role in regional dominance.

- Data Centre Dominance:

- Drivers: Hyperscale expansion, AI/ML workloads, edge computing deployments, HPC requirements.

- Market Size Projection (Base Year 2025): Estimated at $4 billion.

- Growth Momentum: Expected to exhibit a CAGR of 19% to 23% in the forecast period.

- Indirect Contact Type Leadership:

- Drivers: Retrofitting capabilities, modularity, targeted heat removal, compatibility with existing infrastructure.

- Market Share (Estimated Base Year 2025): Approximately 70% to 80% of the total market.

- Technological Advancements: Improved heat transfer fluids, more efficient heat exchangers, advanced pump technologies.

- Emerging Leadership in Direct Contact:

- Drivers: Superior thermal efficiency for extreme densities, potential for significant energy savings, suitability for specialized environments.

- Growth Potential: Projected to grow at a CAGR of 25% to 30% in the forecast period.

- Market Penetration: Expected to increase from 20% to 30% by 2033.

Liquid Cooling Rack Product Developments

Recent product developments in the liquid cooling rack market are focused on enhancing efficiency, scalability, and ease of integration. Innovations include advanced direct-to-chip cold plates designed for higher heat flux CPUs and GPUs, and improved immersion cooling fluids with lower viscosity and better dielectric properties. The introduction of modular and scalable rack-level liquid cooling systems, such as rear-door heat exchangers with intelligent fan control and automated coolant management, is simplifying deployment for data center operators. Competitive advantages are being achieved through reduced power consumption for cooling, increased server density within racks, and extended hardware lifespan due to more stable operating temperatures. Market players are also emphasizing robust leak detection and prevention systems, crucial for widespread adoption.

Report Scope & Segmentation Analysis

This report segments the Liquid Cooling Rack market by Application and Type. The Application segments include Data Centres, Laboratories, Libraries, Workshops, and Others, with Data Centres dominating in terms of market size and growth. Laboratories are experiencing increasing adoption for specialized high-performance computing needs, while Libraries and Workshops represent niche but growing markets for localized high-density computing. The Types segments encompass Direct Contact and Indirect Contact liquid cooling solutions. Direct Contact, including immersion cooling, is projected for substantial growth due to its superior thermal performance. Indirect Contact, such as direct-to-chip and rear-door heat exchangers, currently holds a larger market share due to its broader applicability and compatibility with existing infrastructure.

- Data Centre: Expected market size of $4 billion (2025), with a CAGR of 19% to 23%.

- Laboratory: Projected market size of $200 million (2025), with a CAGR of 15% to 18%.

- Library: Niche segment with projected market size of $50 million (2025), CAGR of 10% to 12%.

- Workshop: Growing segment with projected market size of $150 million (2025), CAGR of 16% to 19%.

- Others: Represents emerging applications and specialized deployments, projected market size of $100 million (2025), CAGR of 17% to 20%.

- Direct Contact: Projected market size of $1 billion (2025), CAGR of 25% to 30%.

- Indirect Contact: Projected market size of $4 billion (2025), CAGR of 17% to 20%.

Key Drivers of Liquid Cooling Rack Growth

The growth of the Liquid Cooling Rack market is primarily propelled by the escalating thermal demands of modern IT equipment. The proliferation of high-performance computing (HPC), artificial intelligence (AI), and machine learning (ML) workloads necessitates advanced cooling solutions that can dissipate significantly higher heat loads than traditional air cooling. Server rack power densities are projected to reach 60 kW to 100 kW in the coming years, making liquid cooling not just an option, but a requirement. Furthermore, the increasing global focus on sustainability and energy efficiency in data centers, driven by regulatory mandates and corporate social responsibility, favors liquid cooling’s superior thermal performance and potential for reduced energy consumption. For instance, liquid cooling can reduce the Power Usage Effectiveness (PUE) of a data center by 10% to 20%. Investments in digital infrastructure and the expansion of hyperscale data centers worldwide also contribute significantly to market expansion.

Challenges in the Liquid Cooling Rack Sector

Despite the promising growth, the Liquid Cooling Rack sector faces several challenges. Initial capital expenditure for liquid cooling infrastructure can be higher compared to air-cooled solutions, posing a barrier for some organizations. The perceived complexity of installation and maintenance, though diminishing with advancements in modular designs, remains a concern for less experienced IT teams. Furthermore, ensuring the reliability and leak-proof nature of liquid cooling systems is paramount, as any failure can have catastrophic consequences for sensitive IT hardware, costing millions in potential data loss and equipment damage. Supply chain disruptions for specialized components and the need for skilled technicians for installation and servicing also present hurdles.

Emerging Opportunities in Liquid Cooling Rack

The Liquid Cooling Rack market presents significant emerging opportunities. The rapid growth of edge computing, requiring compact and efficient cooling solutions for distributed data centers, offers a substantial new market. The development of more cost-effective and user-friendly immersion cooling systems is poised to broaden its adoption beyond high-performance computing environments. Furthermore, the increasing demand for sustainable data center designs and the integration of liquid cooling with renewable energy sources represent a key opportunity for market differentiation. Partnerships between hardware manufacturers, cooling solution providers, and cloud service providers are expected to drive innovation and market penetration. The potential for reusing waste heat generated by data centers for district heating or other industrial applications, facilitated by advanced liquid cooling systems, is another significant emerging avenue.

Leading Players in the Liquid Cooling Rack Market

- CPC

- nVent

- EDP Europe

- Rittal

- DCX

- Alphacool

- Ingrasys

- Gigabyte Technology

- Shenzhen Envicool Technology

- Dongguan Lianli Electronic Technology

Key Developments in Liquid Cooling Rack Industry

- 2023 Q4: Launch of next-generation direct-to-chip cold plates optimized for higher TDP CPUs and GPUs.

- 2024 Q1: Introduction of modular immersion cooling solutions designed for easier integration into existing data center footprints.

- 2024 Q2: Strategic partnership announced between a major server manufacturer and a leading liquid cooling provider to offer integrated liquid-cooled server racks.

- 2024 Q3: Significant investment by a venture capital firm into a startup specializing in advanced dielectric fluids for two-phase immersion cooling.

- 2024 Q4: Release of enhanced leak detection and management systems for rack-level liquid cooling deployments.

- 2025 Q1: Major hyperscaler announces a commitment to deploying liquid-cooled racks across 30% of its new data center capacity.

Strategic Outlook for Liquid Cooling Rack Market

The strategic outlook for the Liquid Cooling Rack market is overwhelmingly positive, driven by the inevitable shift towards higher power densities and increased energy efficiency demands in IT infrastructure. Continued innovation in both direct and indirect contact cooling technologies will further democratize access to these solutions, making them viable for a broader range of applications beyond hyperscale data centers. The focus will increasingly be on integrated, intelligent, and sustainable cooling solutions. Opportunities for market expansion lie in developing standardized protocols, reducing deployment costs, and enhancing the skills of IT professionals in managing liquid-cooled environments. Strategic collaborations and acquisitions will continue to shape the competitive landscape, fostering further advancements and market consolidation. The future success of data centers, HPC, and AI initiatives is inextricably linked to the evolution and adoption of advanced liquid cooling technologies.

Liquid Cooling Rack Segmentation

-

1. Application

- 1.1. Data Centre

- 1.2. Laboratory

- 1.3. Library

- 1.4. Workshop

- 1.5. Others

-

2. Types

- 2.1. Direct Contact

- 2.2. Indirect Contact

Liquid Cooling Rack Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Liquid Cooling Rack REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Liquid Cooling Rack Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Data Centre

- 5.1.2. Laboratory

- 5.1.3. Library

- 5.1.4. Workshop

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Direct Contact

- 5.2.2. Indirect Contact

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Liquid Cooling Rack Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Data Centre

- 6.1.2. Laboratory

- 6.1.3. Library

- 6.1.4. Workshop

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Direct Contact

- 6.2.2. Indirect Contact

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Liquid Cooling Rack Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Data Centre

- 7.1.2. Laboratory

- 7.1.3. Library

- 7.1.4. Workshop

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Direct Contact

- 7.2.2. Indirect Contact

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Liquid Cooling Rack Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Data Centre

- 8.1.2. Laboratory

- 8.1.3. Library

- 8.1.4. Workshop

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Direct Contact

- 8.2.2. Indirect Contact

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Liquid Cooling Rack Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Data Centre

- 9.1.2. Laboratory

- 9.1.3. Library

- 9.1.4. Workshop

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Direct Contact

- 9.2.2. Indirect Contact

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Liquid Cooling Rack Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Data Centre

- 10.1.2. Laboratory

- 10.1.3. Library

- 10.1.4. Workshop

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Direct Contact

- 10.2.2. Indirect Contact

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 CPC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 nVent

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 EDP Europe

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Rittal

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 DCX

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Alphacool

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ingrasys

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Gigabyte Technology

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shenzhen Envicool Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Dongguan Lianli Electronic Technology

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 CPC

List of Figures

- Figure 1: Global Liquid Cooling Rack Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Liquid Cooling Rack Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Liquid Cooling Rack Revenue (million), by Application 2024 & 2032

- Figure 4: North America Liquid Cooling Rack Volume (K), by Application 2024 & 2032

- Figure 5: North America Liquid Cooling Rack Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Liquid Cooling Rack Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Liquid Cooling Rack Revenue (million), by Types 2024 & 2032

- Figure 8: North America Liquid Cooling Rack Volume (K), by Types 2024 & 2032

- Figure 9: North America Liquid Cooling Rack Revenue Share (%), by Types 2024 & 2032

- Figure 10: North America Liquid Cooling Rack Volume Share (%), by Types 2024 & 2032

- Figure 11: North America Liquid Cooling Rack Revenue (million), by Country 2024 & 2032

- Figure 12: North America Liquid Cooling Rack Volume (K), by Country 2024 & 2032

- Figure 13: North America Liquid Cooling Rack Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Liquid Cooling Rack Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Liquid Cooling Rack Revenue (million), by Application 2024 & 2032

- Figure 16: South America Liquid Cooling Rack Volume (K), by Application 2024 & 2032

- Figure 17: South America Liquid Cooling Rack Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Liquid Cooling Rack Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Liquid Cooling Rack Revenue (million), by Types 2024 & 2032

- Figure 20: South America Liquid Cooling Rack Volume (K), by Types 2024 & 2032

- Figure 21: South America Liquid Cooling Rack Revenue Share (%), by Types 2024 & 2032

- Figure 22: South America Liquid Cooling Rack Volume Share (%), by Types 2024 & 2032

- Figure 23: South America Liquid Cooling Rack Revenue (million), by Country 2024 & 2032

- Figure 24: South America Liquid Cooling Rack Volume (K), by Country 2024 & 2032

- Figure 25: South America Liquid Cooling Rack Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Liquid Cooling Rack Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Liquid Cooling Rack Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Liquid Cooling Rack Volume (K), by Application 2024 & 2032

- Figure 29: Europe Liquid Cooling Rack Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Liquid Cooling Rack Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Liquid Cooling Rack Revenue (million), by Types 2024 & 2032

- Figure 32: Europe Liquid Cooling Rack Volume (K), by Types 2024 & 2032

- Figure 33: Europe Liquid Cooling Rack Revenue Share (%), by Types 2024 & 2032

- Figure 34: Europe Liquid Cooling Rack Volume Share (%), by Types 2024 & 2032

- Figure 35: Europe Liquid Cooling Rack Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Liquid Cooling Rack Volume (K), by Country 2024 & 2032

- Figure 37: Europe Liquid Cooling Rack Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Liquid Cooling Rack Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Liquid Cooling Rack Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Liquid Cooling Rack Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Liquid Cooling Rack Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Liquid Cooling Rack Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Liquid Cooling Rack Revenue (million), by Types 2024 & 2032

- Figure 44: Middle East & Africa Liquid Cooling Rack Volume (K), by Types 2024 & 2032

- Figure 45: Middle East & Africa Liquid Cooling Rack Revenue Share (%), by Types 2024 & 2032

- Figure 46: Middle East & Africa Liquid Cooling Rack Volume Share (%), by Types 2024 & 2032

- Figure 47: Middle East & Africa Liquid Cooling Rack Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Liquid Cooling Rack Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Liquid Cooling Rack Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Liquid Cooling Rack Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Liquid Cooling Rack Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Liquid Cooling Rack Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Liquid Cooling Rack Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Liquid Cooling Rack Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Liquid Cooling Rack Revenue (million), by Types 2024 & 2032

- Figure 56: Asia Pacific Liquid Cooling Rack Volume (K), by Types 2024 & 2032

- Figure 57: Asia Pacific Liquid Cooling Rack Revenue Share (%), by Types 2024 & 2032

- Figure 58: Asia Pacific Liquid Cooling Rack Volume Share (%), by Types 2024 & 2032

- Figure 59: Asia Pacific Liquid Cooling Rack Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Liquid Cooling Rack Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Liquid Cooling Rack Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Liquid Cooling Rack Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Liquid Cooling Rack Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Liquid Cooling Rack Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Liquid Cooling Rack Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Liquid Cooling Rack Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Liquid Cooling Rack Revenue million Forecast, by Types 2019 & 2032

- Table 6: Global Liquid Cooling Rack Volume K Forecast, by Types 2019 & 2032

- Table 7: Global Liquid Cooling Rack Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Liquid Cooling Rack Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Liquid Cooling Rack Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Liquid Cooling Rack Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Liquid Cooling Rack Revenue million Forecast, by Types 2019 & 2032

- Table 12: Global Liquid Cooling Rack Volume K Forecast, by Types 2019 & 2032

- Table 13: Global Liquid Cooling Rack Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Liquid Cooling Rack Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Liquid Cooling Rack Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Liquid Cooling Rack Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Liquid Cooling Rack Revenue million Forecast, by Types 2019 & 2032

- Table 24: Global Liquid Cooling Rack Volume K Forecast, by Types 2019 & 2032

- Table 25: Global Liquid Cooling Rack Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Liquid Cooling Rack Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Liquid Cooling Rack Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Liquid Cooling Rack Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Liquid Cooling Rack Revenue million Forecast, by Types 2019 & 2032

- Table 36: Global Liquid Cooling Rack Volume K Forecast, by Types 2019 & 2032

- Table 37: Global Liquid Cooling Rack Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Liquid Cooling Rack Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Liquid Cooling Rack Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Liquid Cooling Rack Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Liquid Cooling Rack Revenue million Forecast, by Types 2019 & 2032

- Table 60: Global Liquid Cooling Rack Volume K Forecast, by Types 2019 & 2032

- Table 61: Global Liquid Cooling Rack Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Liquid Cooling Rack Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Liquid Cooling Rack Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Liquid Cooling Rack Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Liquid Cooling Rack Revenue million Forecast, by Types 2019 & 2032

- Table 78: Global Liquid Cooling Rack Volume K Forecast, by Types 2019 & 2032

- Table 79: Global Liquid Cooling Rack Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Liquid Cooling Rack Volume K Forecast, by Country 2019 & 2032

- Table 81: China Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Liquid Cooling Rack Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Liquid Cooling Rack Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Cooling Rack?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Liquid Cooling Rack?

Key companies in the market include CPC, nVent, EDP Europe, Rittal, DCX, Alphacool, Ingrasys, Gigabyte Technology, Shenzhen Envicool Technology, Dongguan Lianli Electronic Technology.

3. What are the main segments of the Liquid Cooling Rack?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Cooling Rack," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Cooling Rack report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Cooling Rack?

To stay informed about further developments, trends, and reports in the Liquid Cooling Rack, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence