Key Insights

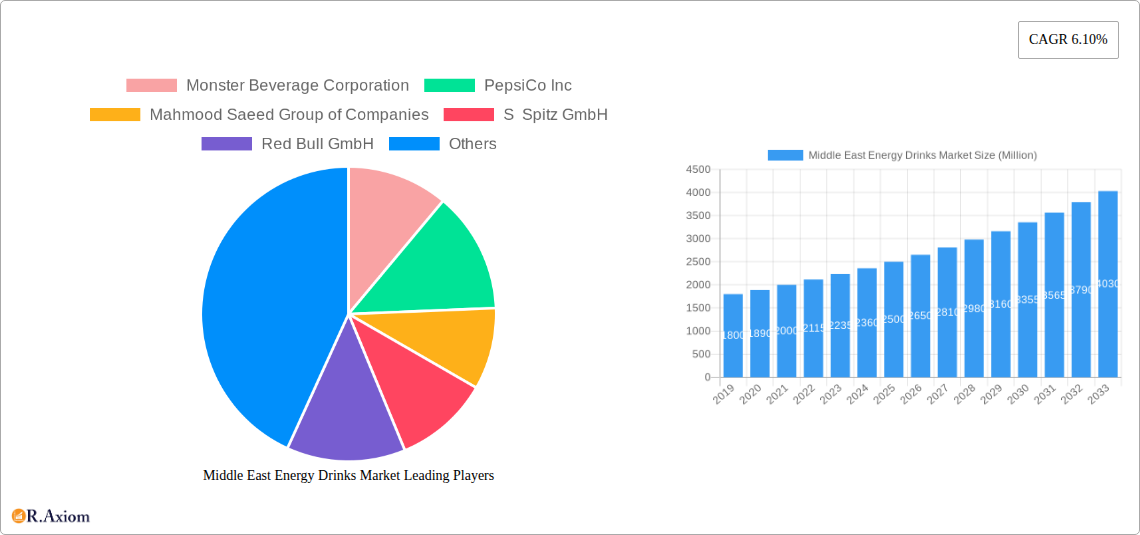

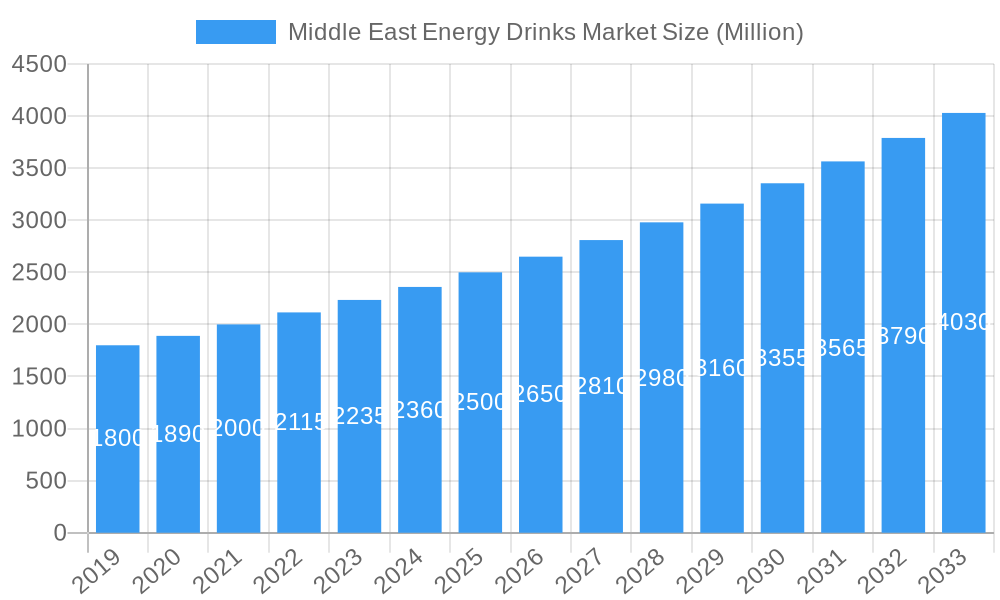

The Middle East energy drinks market is projected to expand significantly, reaching $3968.3 million by 2033, with a robust Compound Annual Growth Rate (CAGR) of 8.1% from the 2023 base year. This growth is propelled by shifting consumer lifestyles, rising disposable incomes, and a heightened demand for functional beverages that enhance energy and focus. Key drivers include the increasing popularity of sports and fitness, alongside the burgeoning digital content creation and gaming culture, particularly among younger demographics. Major players are actively expanding their market presence through aggressive marketing and innovative product development.

Middle East Energy Drinks Market Market Size (In Billion)

Market segmentation highlights a dynamic landscape. While traditional energy drinks maintain a strong presence, there is a notable rise in demand for natural/organic and sugar-free/low-calorie options, reflecting growing health consciousness in the Middle East. Packaging innovations, favoring metal cans and PET bottles for convenience and portability, are also influencing consumer choices. Distribution channels are evolving, with online retail and supermarkets/hypermarkets experiencing substantial growth within off-trade channels, complemented by on-trade venues. Leading companies are engaged in fierce competition, introducing new flavors and formulations. Health concerns regarding sugar and caffeine content are being addressed through product reformulations and the promotion of healthier alternatives.

Middle East Energy Drinks Market Company Market Share

This comprehensive report offers an in-depth analysis of the Middle East energy drinks market, a dynamic sector driven by evolving consumer lifestyles, increasing disposable incomes, and a burgeoning demand for performance-enhancing beverages. Covering the historical period and projecting growth through 2033, this report provides unparalleled insights for industry stakeholders navigating this lucrative market. Leveraging sophisticated market intelligence, we dissect key trends, dominant segments, competitive landscapes, and future opportunities within the MENA energy drink industry.

Middle East Energy Drinks Market Market Concentration & Innovation

The Middle East energy drinks market is characterized by a moderate to high level of concentration, with global giants like Red Bull GmbH and Monster Beverage Corporation holding significant market share. However, the presence of strong regional players such as Mahmood Saeed Group of Companies and Abuljadayel Beverages Industries Llc, alongside emerging brands, fosters a competitive environment ripe for innovation. Key innovation drivers include the increasing demand for sugar-free energy drinks, natural/organic energy drinks, and beverages with added functional benefits. Regulatory frameworks concerning ingredient disclosures and health claims are evolving, influencing product development and marketing strategies. Substitutes like coffee and traditional soft drinks pose a moderate threat, but the unique value proposition of energy drinks in boosting alertness and performance continues to drive consumption. End-user trends are heavily influenced by young demographics, a growing sports and fitness culture, and the need for sustained energy in demanding work environments. Mergers and acquisitions (M&A) activity, while not extensively documented publicly for this specific region, are anticipated to increase as larger players seek to expand their portfolios and market reach, potentially involving deal values in the hundreds of millions of dollars for significant acquisitions.

Middle East Energy Drinks Market Industry Trends & Insights

The Middle East energy drinks market is poised for robust growth, driven by a confluence of factors. The escalating demand for convenient and effective solutions to combat fatigue and enhance mental and physical performance is a primary catalyst. A significant trend is the rising adoption of sugar-free and low-calorie energy drinks, mirroring global health consciousness shifts. This segment is projected to witness a compound annual growth rate (CAGR) of approximately 7.5% during the forecast period (2025-2033). Technological disruptions in beverage formulation and packaging are enabling manufacturers to introduce novel flavors, ingredients, and delivery formats, such as energy shots. Consumer preferences are increasingly leaning towards products with natural ingredients and functional benefits beyond mere energy boosts, including vitamins and antioxidants. Competitive dynamics are intensifying, with established players continuously launching new products and marketing campaigns, while new entrants are exploring niche markets and innovative distribution strategies. The market penetration of energy drinks is steadily increasing across various demographic segments, particularly among young adults and professionals aged 18-35, who are key consumers due to demanding lifestyles and active social engagements. The overall market size is projected to reach an estimated USD 3,500 million by 2025.

Dominant Markets & Segments in Middle East Energy Drinks Market

The United Arab Emirates (UAE) and Saudi Arabia stand out as the dominant markets within the Middle East energy drinks sector, collectively accounting for over 60% of the regional market share. This dominance is attributed to their large youth populations, high disposable incomes, significant expatriate communities, and proactive government initiatives promoting healthy lifestyles and sports.

Soft Drink Type Dominance:

- Sugar-free or Low-calories Energy Drinks: This segment is experiencing the most rapid expansion, driven by health-conscious consumers and government regulations aimed at reducing sugar intake. Its market share is projected to grow to approximately 35% by 2033.

- Traditional Energy Drinks: While still holding a substantial market share, its growth rate is moderating as consumers seek healthier alternatives.

- Natural/Organic Energy Drinks: This niche segment is gaining traction, appealing to a growing segment of consumers seeking products with perceived health benefits and fewer artificial ingredients.

Packaging Type Dominance:

- Metal Can: This packaging type remains the most popular due to its convenience, portability, and perceived premium appeal. It currently dominates with a market share of around 55%.

- PET Bottles: Growing in popularity for their lighter weight and shatter-resistant properties, especially in larger formats.

- Glass Bottles: Primarily associated with premium or specialized energy drinks.

Distribution Channel Dominance:

- Off-trade: This channel is the primary driver of sales, with convenience stores and supermarkets/hypermarkets leading the charge.

- Online Retail: Experiencing exceptional growth, particularly in urban centers, driven by e-commerce expansion and consumer preference for home delivery. Its market share is projected to exceed 20% by 2033.

- On-trade: Restaurants, cafes, and entertainment venues contribute to sales, though to a lesser extent than off-trade channels.

- Off-trade: This channel is the primary driver of sales, with convenience stores and supermarkets/hypermarkets leading the charge.

Key drivers for this dominance include favorable economic policies, robust retail infrastructure development, high internet penetration rates, and targeted marketing campaigns catering to the preferences of the young and urbanized populations in these leading countries.

Middle East Energy Drinks Market Product Developments

Product development in the Middle East energy drinks market is intensely focused on innovation to meet evolving consumer demands. Recent developments highlight a significant shift towards healthier options, with brands introducing sugar-free variants and incorporating natural ingredients. For example, the launch of Monster Energy Zero Sugar with 160 mg of caffeine in January 2023 caters to consumers actively seeking reduced sugar intake. Red Bull GmBH’s introduction of an Apricot-Strawberry zero-sugar flavor in March 2022 further exemplifies this trend. PepsiCo's foray into hemp-based energy drinks with Rockstar Energy in January 2022, featuring lower caffeine content (80 mg per 12-ounce can) and novel flavors, showcases a strategy to diversify its portfolio and attract a broader consumer base. These innovations aim to enhance product appeal, differentiate brands in a crowded market, and capture new consumer segments looking for performance-enhancing beverages with added health benefits and unique flavor profiles.

Report Scope & Segmentation Analysis

This report comprehensively segments the Middle East energy drinks market to provide granular insights into its diverse landscape. The segmentation encompasses:

Soft Drink Type: This includes Energy Shots, offering highly concentrated energy boosts; Natural/Organic Energy Drinks, appealing to health-conscious consumers; Sugar-free or Low-calories Energy Drinks, addressing growing health concerns; Traditional Energy Drinks, the established segment; and Other Energy Drinks, encompassing niche and innovative formulations. Each sub-segment's growth projections and competitive dynamics are meticulously analyzed.

Packaging Type: Key categories are Glass Bottles, favored for premium offerings; Metal Can, the dominant and convenient format; and PET Bottles, gaining traction for their practicality and environmental considerations. Market size and consumption patterns for each are detailed.

Distribution Channel: The report delves into Off-trade channels, further broken down into Convenience Stores, Online Retail, Supermarket/Hypermarket, and Others, analyzing their respective market shares and growth trajectories. The On-trade channel, representing sales in hospitality venues, is also assessed, with projected market sizes and competitive factors influencing each segment.

Key Drivers of Middle East Energy Drinks Market Growth

Several factors are propelling the growth of the Middle East energy drinks market. Economically, rising disposable incomes and a growing young demographic with active lifestyles are key contributors, increasing consumer spending on lifestyle beverages. Technologically, advancements in beverage formulation allow for the creation of a wider variety of flavors and functional benefits, such as added vitamins and natural stimulants, catering to diverse consumer preferences. Regulatory frameworks, while sometimes presenting challenges, also drive innovation towards healthier options, particularly with the increasing focus on reducing sugar consumption in many Middle Eastern countries. The burgeoning sports and fitness culture, coupled with the demand for sustained energy in academic and professional settings, further fuels consumption.

Challenges in the Middle East Energy Drinks Market Sector

Despite the strong growth trajectory, the Middle East energy drinks market faces several challenges. Regulatory hurdles, including stringent labeling requirements, ingredient restrictions, and marketing regulations, can impact product launches and expansion. Health concerns associated with high sugar and caffeine content in traditional energy drinks continue to be a significant barrier, prompting a shift towards healthier alternatives and potentially limiting market penetration among health-conscious demographics. Competitive pressures from established global brands and an increasing number of local players create an intensely saturated market, requiring significant investment in marketing and product differentiation. Supply chain complexities, particularly in logistics and distribution across diverse geographical regions within the Middle East, can also pose operational challenges.

Emerging Opportunities in Middle East Energy Drinks Market

The Middle East energy drinks market presents numerous emerging opportunities for growth and innovation. The escalating demand for natural and organic energy drinks signifies a significant avenue, with consumers actively seeking products perceived as healthier and free from artificial additives. The energy shots segment, offering convenience and a rapid energy boost, is another promising area for expansion. Furthermore, the increasing adoption of e-commerce and online retail channels presents a substantial opportunity for direct-to-consumer sales and broader market reach, especially in densely populated urban centers. There is also potential for developing energy drinks tailored to specific functional needs, such as those for gaming, studying, or pre-workout routines, tapping into niche consumer segments. Collaborations with fitness influencers and sports organizations can further enhance brand visibility and market penetration.

Leading Players in the Middle East Energy Drinks Market Market

- Monster Beverage Corporation

- PepsiCo Inc

- Mahmood Saeed Group of Companies

- S Spitz GmbH

- Red Bull GmbH

- Applied Nutrition Ltd

- Ghost Beverages LLC

- ZOA Energy LLC

- Yeni Magazacilik Anonim Sirketi

- Anheuser-Busch InBev SA/NV

- Vital Pharmaceuticals Inc

- Congo Brands

- Sapporo Holdings Limited

- Abuljadayel Beverages Industries Llc

- Buffalo energy drinks GmbH

Key Developments in Middle East Energy Drinks Market Industry

- January 2023: Monster Energy launched Monster Energy Zero Sugar, which is primed with 160 mg of caffeine. The launch was projected to tap a new consumer base that prefers sugar-free energy drinks. These products are available across retail channels of Saudi Arabia and United Arab Emirates.

- March 2022: Red Bull GmBH introduced a new energy drink, i.e., Apricot-Strawberry flavor with a zero-sugar option, in order to cater to the consumers preferring sugar-free drinks in the Saudi Arabian Market.

- January 2022: In a move to diversify its product portfolio, PepsiCo introduced "Rockstar Energy," a line of hemp-based energy drinks in the Middle East. This new lineup, available in three flavors, claims a lower caffeine content than other Rockstar offerings. Each 12-ounce can of Rockstar Energy packs 80 mg of caffeine.

Strategic Outlook for Middle East Energy Drinks Market Market

The strategic outlook for the Middle East energy drinks market is exceptionally promising, driven by sustained consumer demand for performance-enhancing and lifestyle beverages. Future growth will be significantly influenced by continued innovation in product formulation, with an emphasis on healthier alternatives like sugar-free energy drinks, natural ingredients, and functional benefits. The expansion of online retail channels presents a key growth catalyst, allowing brands to reach a wider audience efficiently. Strategic partnerships, targeted marketing campaigns leveraging digital platforms, and a focus on understanding evolving consumer preferences for taste and efficacy will be crucial for success. The market is expected to witness continued expansion, driven by demographic trends and an increasing integration of energy drinks into daily routines across various consumer segments.

Middle East Energy Drinks Market Segmentation

-

1. Soft Drink Type

- 1.1. Energy Shots

- 1.2. Natural/Organic Energy Drinks

- 1.3. Sugar-free or Low-calories Energy Drinks

- 1.4. Traditional Energy Drinks

- 1.5. Other Energy Drinks

-

2. Packaging Type

- 2.1. Glass Bottles

- 2.2. Metal Can

- 2.3. PET Bottles

-

3. Distribution Channel

-

3.1. Off-trade

- 3.1.1. Convenience Stores

- 3.1.2. Online Retail

- 3.1.3. Supermarket/Hypermarket

- 3.1.4. Others

- 3.2. On-trade

-

3.1. Off-trade

Middle East Energy Drinks Market Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East Energy Drinks Market Regional Market Share

Geographic Coverage of Middle East Energy Drinks Market

Middle East Energy Drinks Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 5.1.1. Energy Shots

- 5.1.2. Natural/Organic Energy Drinks

- 5.1.3. Sugar-free or Low-calories Energy Drinks

- 5.1.4. Traditional Energy Drinks

- 5.1.5. Other Energy Drinks

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Glass Bottles

- 5.2.2. Metal Can

- 5.2.3. PET Bottles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Off-trade

- 5.3.1.1. Convenience Stores

- 5.3.1.2. Online Retail

- 5.3.1.3. Supermarket/Hypermarket

- 5.3.1.4. Others

- 5.3.2. On-trade

- 5.3.1. Off-trade

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 6. Middle East Energy Drinks Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 6.1.1. Energy Shots

- 6.1.2. Natural/Organic Energy Drinks

- 6.1.3. Sugar-free or Low-calories Energy Drinks

- 6.1.4. Traditional Energy Drinks

- 6.1.5. Other Energy Drinks

- 6.2. Market Analysis, Insights and Forecast - by Packaging Type

- 6.2.1. Glass Bottles

- 6.2.2. Metal Can

- 6.2.3. PET Bottles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Off-trade

- 6.3.1.1. Convenience Stores

- 6.3.1.2. Online Retail

- 6.3.1.3. Supermarket/Hypermarket

- 6.3.1.4. Others

- 6.3.2. On-trade

- 6.3.1. Off-trade

- 6.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Monster Beverage Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 PepsiCo Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mahmood Saeed Group of Companies

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 S Spitz GmbH

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Red Bull GmbH

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Applied Nutrition Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ghost Beverages LLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ZOA Energy LL

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Yeni Magazacilik Anonim Sirketi

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Anheuser-Busch InBev SA/NV

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Vital Pharmaceuticals Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Congo Brands

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Sapporo Holdings Limited

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Abuljadayel Beverages Industries Llc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Buffalo energy drinks GmbH

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Monster Beverage Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle East Energy Drinks Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Middle East Energy Drinks Market Share (%) by Company 2025

List of Tables

- Table 1: Middle East Energy Drinks Market Revenue million Forecast, by Soft Drink Type 2020 & 2033

- Table 2: Middle East Energy Drinks Market Revenue million Forecast, by Packaging Type 2020 & 2033

- Table 3: Middle East Energy Drinks Market Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Middle East Energy Drinks Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: Middle East Energy Drinks Market Revenue million Forecast, by Soft Drink Type 2020 & 2033

- Table 6: Middle East Energy Drinks Market Revenue million Forecast, by Packaging Type 2020 & 2033

- Table 7: Middle East Energy Drinks Market Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 8: Middle East Energy Drinks Market Revenue million Forecast, by Country 2020 & 2033

- Table 9: Saudi Arabia Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: United Arab Emirates Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Israel Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Qatar Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Kuwait Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Oman Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Bahrain Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Jordan Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Lebanon Middle East Energy Drinks Market Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Energy Drinks Market?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Middle East Energy Drinks Market?

Key companies in the market include Monster Beverage Corporation, PepsiCo Inc, Mahmood Saeed Group of Companies, S Spitz GmbH, Red Bull GmbH, Applied Nutrition Ltd, Ghost Beverages LLC, ZOA Energy LL, Yeni Magazacilik Anonim Sirketi, Anheuser-Busch InBev SA/NV, Vital Pharmaceuticals Inc, Congo Brands, Sapporo Holdings Limited, Abuljadayel Beverages Industries Llc, Buffalo energy drinks GmbH.

3. What are the main segments of the Middle East Energy Drinks Market?

The market segments include Soft Drink Type, Packaging Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 3968.3 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Functional and Fortified Food; Multi-functionality and Wide Application of Riboflavin.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Low Stability of Riboflavin on Exposure to Light and Heat.

8. Can you provide examples of recent developments in the market?

January 2023: Monster Energy launched Monster Energy Zero Sugar, which is primed with 160 mg of caffeine. The launch was projected to tap a new consumer base that prefers sugar-free energy drinks. These products are available across retail channels of Saudi Arabia and United Arab Emirates.March 2022: RedBull GmBH introduced a new energy drink, i.e., Apricot-Strawberry flavor with a zero-sugar option, in order to cater to the consumers preferring sugar-free drinks in the Saudi Arabian Market.January 2022: In a move to diversify its product portfolio, PepsiCo introduced "Rockstar Energy," a line of hemp-based energy drinks in the Middle East. This new lineup, available in three flavors, claims a lower caffeine content than other Rockstar offerings. Each 12-ounce can of Rockstar Energy packs 80 mg of caffeine.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Energy Drinks Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Energy Drinks Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Energy Drinks Market?

To stay informed about further developments, trends, and reports in the Middle East Energy Drinks Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence