Key Insights

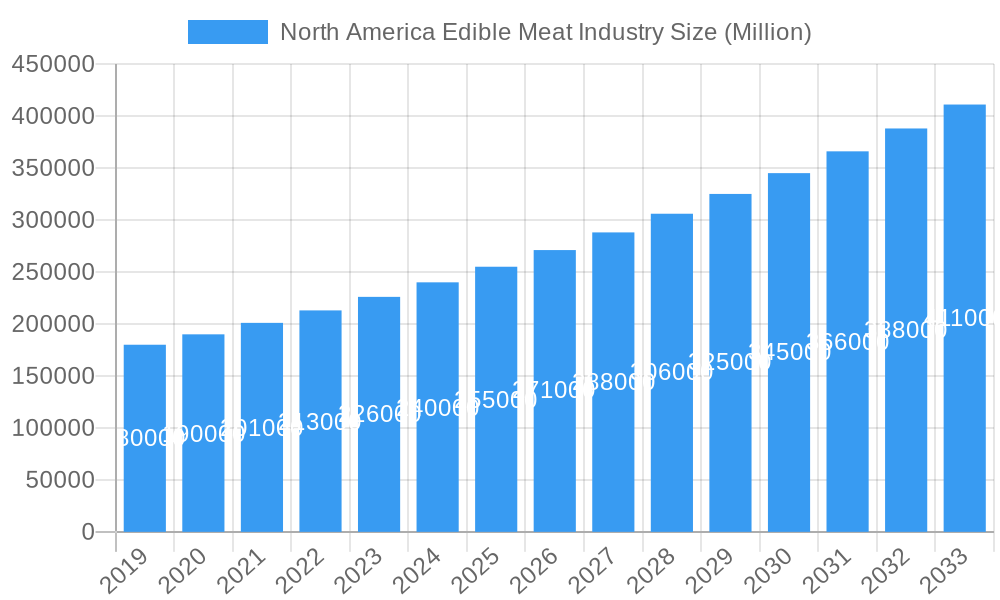

The North America Edible Meat Industry is forecast for significant expansion, projected to reach USD 216.98 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.96% through 2033. This growth is propelled by increased demand for protein-rich diets, a rising preference for convenient food options, and the expanding availability of diverse meat products across retail and food service sectors. Key drivers include a growing middle class with greater disposable income, heightened awareness of meat as a crucial nutrient source, and the influence of global culinary trends. Advancements in food processing technology and robust supply chain infrastructure are also critical in meeting this demand. The industry is witnessing a notable shift towards value-added and processed meat products, offering consumers enhanced convenience and variety. Innovations in packaging and preservation techniques further support this evolution by extending shelf life and improving product appeal, aligning with busy lifestyles and diverse consumer preferences.

North America Edible Meat Industry Market Size (In Billion)

The market is shaped by a dynamic interplay of opportunities and challenges. The increasing adoption of e-commerce and online grocery platforms is significantly expanding access to a wide array of meat products, thereby boosting sales. The 'off-trade' segment, including convenience stores, online channels, and supermarkets, shows strong performance, indicating a consumer preference for accessible purchasing options. However, the industry faces restraints such as fluctuating raw material prices, impacting profit margins, and growing consumer concerns regarding animal welfare and the environmental impact of meat production. Regulatory pressures and the increasing adoption of plant-based alternatives also present challenges. Despite these factors, the North American edible meat market remains robust, driven by consistent consumer demand and ongoing industry innovation. The competitive landscape features a blend of global and regional players vying for market share through product diversification, strategic partnerships, and expanded distribution networks.

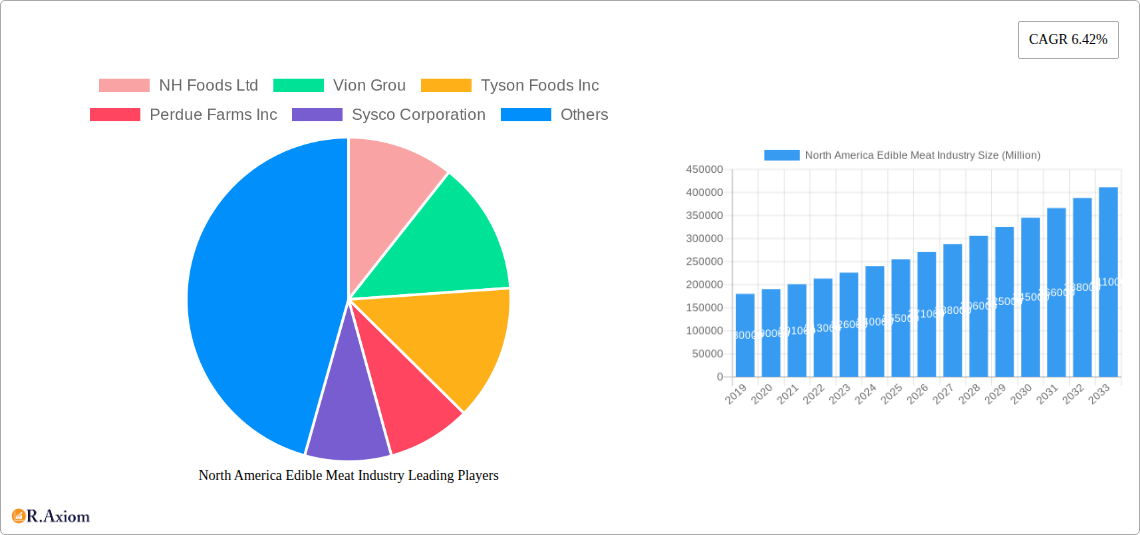

North America Edible Meat Industry Company Market Share

North America Edible Meat Industry Report: Strategic Analysis & Future Projections (2019-2033)

This comprehensive report provides an in-depth analysis of the North America Edible Meat Industry, offering critical insights into market dynamics, competitive landscapes, and future growth trajectories. Covering the historical period from 2019-2024 and projecting through 2033, with a base year of 2025, this analysis is essential for stakeholders navigating this vital sector. We meticulously examine key segments including Beef, Mutton, Pork, and Poultry across various forms such as Fresh/Chilled, Frozen, Canned, and Processed meat. Distribution channels, encompassing Off-Trade (Supermarkets, Hypermarkets, Online Channels, Convenience Stores) and On-Trade, are thoroughly analyzed. Discover actionable intelligence on market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and significant M&A activities, with an estimated market size of USD 216.98 billion for the North American market in 2025. This report is your definitive guide to understanding and capitalizing on opportunities within the North America edible meat market.

North America Edible Meat Industry Market Concentration & Innovation

The North America Edible Meat Industry exhibits a moderate to high degree of market concentration, with a few dominant players holding significant market shares, estimated to be over 60% of the total market value. Innovation is a critical differentiator, driven by consumer demand for healthier, sustainable, and convenient protein options. Key innovation drivers include the development of novel processing techniques to enhance shelf-life and nutritional value, the introduction of plant-based meat alternatives that challenge traditional offerings, and advancements in traceability and supply chain transparency. Regulatory frameworks, such as stringent food safety standards and evolving labeling requirements, play a crucial role in shaping market entry and operational strategies. Product substitutes, primarily plant-based proteins and other alternative food sources, are increasingly impacting market share, particularly among health-conscious and environmentally aware consumers. End-user trends are shifting towards premiumization, ethically sourced products, and increased consumption of poultry and plant-based alternatives. Mergers and acquisitions (M&A) remain a significant strategy for consolidation and market expansion, with estimated M&A deal values exceeding $5,000 Million annually.

- Market Share: Dominant players collectively hold an estimated over 60% market share.

- Innovation Drivers:

- Nutritional enhancement and shelf-life extension technologies.

- Development of sustainable and ethically sourced products.

- Increased focus on plant-based and alternative protein innovations.

- Blockchain for supply chain traceability.

- Regulatory Frameworks: Strict adherence to food safety, animal welfare, and labeling regulations.

- Product Substitutes: Growing influence of plant-based meats and other alternative protein sources.

- End-User Trends: Demand for convenience, health benefits, sustainability, and premium quality.

- M&A Activities: Active consolidation through strategic acquisitions and mergers, with annual deal values surpassing $5,000 Million.

North America Edible Meat Industry Industry Trends & Insights

The North America Edible Meat Industry is poised for robust growth, with an estimated Compound Annual Growth Rate (CAGR) of approximately 4.5% projected over the forecast period (2025-2033). This expansion is fueled by several key trends and insights. Growing consumer awareness regarding health and nutrition continues to drive demand for lean protein sources, particularly poultry, which boasts a lower fat content and is perceived as a healthier alternative. The increasing adoption of convenience foods and ready-to-eat meals, propelled by busy lifestyles, is boosting the market for processed and pre-cooked meat products. Technological disruptions are profoundly reshaping the industry, with advancements in precision agriculture, automated processing, and cold chain logistics enhancing efficiency and reducing waste. The rise of e-commerce and online grocery platforms has significantly expanded the distribution channels for edible meat products, making them more accessible to a wider consumer base. Competitive dynamics are intensifying, with established players diversifying their product portfolios, investing in sustainable practices, and engaging in strategic partnerships to maintain and enhance their market positions. The increasing penetration of private label brands in supermarkets and hypermarkets is also creating competitive pressure on national brands. Furthermore, global supply chain vulnerabilities and geopolitical events have heightened the importance of localized sourcing and resilient supply chains, encouraging greater investment in domestic production and processing capabilities. The sustained demand for traditional meat products, coupled with the nascent but rapidly growing market for alternative proteins, creates a dynamic and complex market landscape. The market penetration for protein-rich diets remains high, with consumers increasingly seeking variety and quality across all meat types.

Dominant Markets & Segments in North America Edible Meat Industry

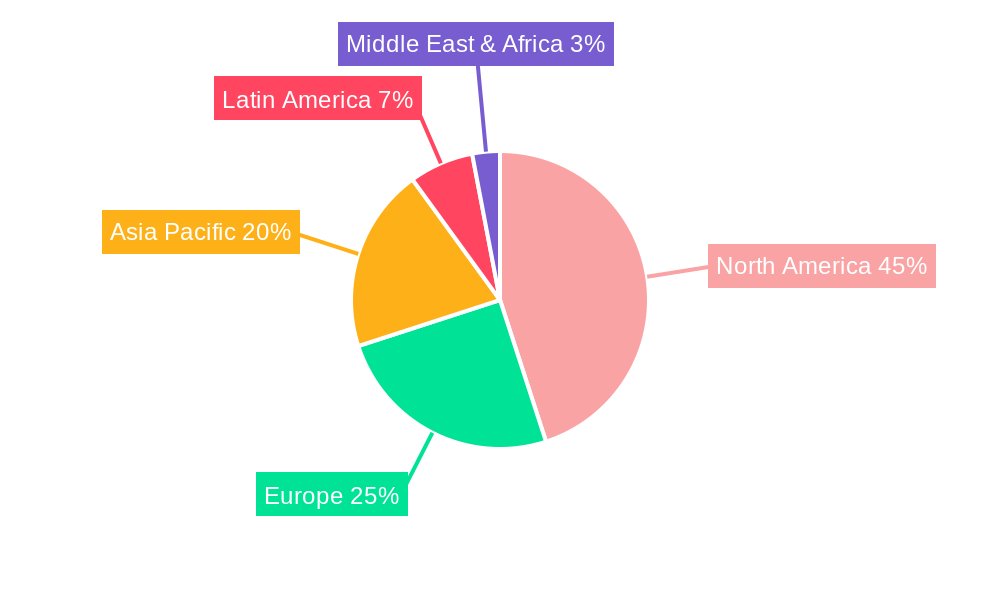

The North American Edible Meat Industry is dominated by the United States, which represents the largest market in terms of both volume and value, driven by a large population, robust economic conditions, and established consumption patterns. Within the Type segment, Poultry emerges as the dominant category, accounting for an estimated 45% of the total market value. This dominance is attributed to its versatility, perceived health benefits, and competitive pricing compared to other meats. Beef follows as a significant segment, with a substantial market share of approximately 30%, driven by consumer preference for traditional dishes and premium cuts. Pork holds a considerable share, estimated at 20%, owing to its widespread use in various culinary applications and processed meat products. Fresh/Chilled meat, comprising an estimated 55% of the market value, is the leading Form, reflecting consumer preference for minimally processed products and greater perceived freshness. Frozen meat follows with a substantial share of 30%, driven by its longer shelf-life and convenience for storage. The Distribution Channel landscape is largely shaped by Off-Trade sales, which account for over 70% of the market. Within Off-Trade, Supermarkets and Hypermarkets are the primary channel, holding an estimated 50% market share, due to their extensive reach and product variety. The Online Channel is experiencing rapid growth, with an estimated market share of 15%, driven by the convenience of home delivery and the expansion of e-commerce platforms.

- Leading Region: United States.

- Key Drivers: Large population, strong economic base, established meat consumption culture, significant agricultural output.

- Dominant Type: Poultry.

- Key Drivers: Affordability, perceived health benefits, versatility in culinary applications, consistent supply.

- Dominant Form: Fresh/Chilled.

- Key Drivers: Consumer preference for freshness and minimal processing, wider availability of fresh cuts.

- Dominant Distribution Channel: Off-Trade.

- Key Drivers: Convenience, accessibility, wide product selection, competitive pricing.

- Sub-Dominant Channel: Supermarkets and Hypermarkets.

- Key Drivers: One-stop shopping experience, promotional offers, extensive product ranges.

North America Edible Meat Industry Product Developments

Product development in the North America edible meat industry is increasingly focused on enhancing consumer appeal through innovation and addressing evolving dietary preferences. Key developments include the expansion of value-added products such as marinated and seasoned meats, convenient meal kits featuring meat components, and ready-to-cook options. There is a significant push towards producing leaner meat products with reduced sodium and fat content, aligning with growing health consciousness. Furthermore, advancements in packaging technologies are extending shelf-life and improving product presentation, thereby reducing food waste and enhancing consumer convenience. The integration of smart packaging that provides temperature monitoring and extended shelf-life indicators is also emerging.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the North America Edible Meat Industry, segmenting the market by Type, Form, and Distribution Channel.

Type Segmentation: This includes Beef, Mutton, Pork, Poultry, and Other Meat. Each segment is analyzed for market size, growth projections, and competitive dynamics, with poultry projected to lead in market value during the forecast period.

Form Segmentation: This segment covers Canned, Fresh/Chilled, Frozen, and Processed meat. Fresh/Chilled and Frozen forms are expected to dominate, driven by consumer preferences for convenience and perceived quality, with strong growth anticipated in the processed meat segment due to value-added offerings.

Distribution Channel Segmentation: This encompasses Off-Trade (including Convenience Stores, Online Channel, Supermarkets and Hypermarkets, and Others) and On-Trade. The Off-Trade channel, particularly supermarkets and the rapidly growing online segment, is projected to witness sustained expansion, reflecting changing consumer shopping habits.

Key Drivers of North America Edible Meat Industry Growth

The growth of the North America Edible Meat Industry is propelled by several interconnected factors.

- Rising Disposable Incomes: Increased purchasing power allows consumers to opt for higher-quality and a wider variety of meat products.

- Population Growth: A growing population directly translates to increased demand for essential food sources like edible meat.

- Demand for Protein: Persistent consumer focus on protein intake for health and fitness fuels consistent demand across meat types.

- Technological Advancements: Innovations in farming, processing, and logistics enhance efficiency, reduce costs, and improve product quality, making meat more accessible and appealing.

- Convenience and Value-Added Products: The market is driven by an increasing demand for ready-to-cook and value-added meat products that cater to busy lifestyles.

Challenges in the North America Edible Meat Industry Sector

Despite robust growth, the North America Edible Meat Industry faces several significant challenges:

- Stringent Regulations: Evolving food safety, animal welfare, and environmental regulations require continuous investment and adaptation from industry players.

- Supply Chain Volatility: Fluctuations in feed costs, labor shortages, and unforeseen events like disease outbreaks can disrupt supply chains and impact profitability.

- Growing Competition from Alternatives: The rise of plant-based and other alternative protein sources poses a competitive threat, especially to traditional meat consumption.

- Consumer Health Concerns: Increasing awareness about the health implications of red meat consumption can lead to shifts in consumer preference towards leaner protein options.

- Environmental Scrutiny: The environmental footprint of meat production is under increasing scrutiny, pushing for more sustainable practices and potentially leading to higher operational costs.

Emerging Opportunities in North America Edible Meat Industry

The North America Edible Meat Industry presents numerous emerging opportunities for growth and innovation.

- Sustainable Sourcing and Production: Growing consumer demand for ethically sourced and environmentally friendly products creates a significant opportunity for companies adopting sustainable practices.

- Expansion of Value-Added Products: Innovation in ready-to-eat meals, marinated meats, and specialized cuts can cater to evolving consumer preferences for convenience and unique culinary experiences.

- Direct-to-Consumer (DTC) Models: Leveraging online channels and e-commerce platforms to establish direct relationships with consumers can enhance brand loyalty and capture higher margins.

- Fortification and Nutritional Enhancement: Developing meat products fortified with essential vitamins and minerals can appeal to health-conscious consumers.

- Traceability and Transparency: Implementing advanced technologies like blockchain to ensure product traceability can build consumer trust and command premium pricing.

Leading Players in the North America Edible Meat Industry Market

- NH Foods Ltd

- Vion Group

- Tyson Foods Inc

- Perdue Farms Inc

- Sysco Corporation

- The Kraft Heinz Company

- Foster Farms Inc

- Continental Grain Company

- Hormel Foods Corporation

- Cargill Inc

- Marfrig Global Foods S A

- The Clemens Family Corporation

- JBS SA

- OSI Group

Key Developments in North America Edible Meat Industry Industry

- February 2023: Sysco Corporation has launched its new ‘Recipe for Sustainability’ program. Through this program, Sysco will collaborate with top Students at Arizona State University and Pennsylvania State University to explore innovations that will accelerate climate action and lead the industry towards a more sustainable future.

- December 2022: JBS USA, a subsidiary of JBS SA, announced it reached an agreement to acquire certain assets from TriOak Foods for an undisclosed amount. Operations of TriOak Foods include live pork production, grain merchandising, and fertilizer marketing.

- July 2022: Cargill Incorporated partnered with Continental Grain Company to acquire Sanderson Farms. Upon completion of the acquisition, Cargill and Continental Grain will combine Sanderson Farms with Wayne Farms, a subsidiary of Continental Grain, to form a new, privately held poultry business. The combination of Sanderson Farms and Wayne Farms will create a best-in-class US poultry company with a high-quality asset base, complementary operating cultures, and an industry-leading management team and workforce.

Strategic Outlook for North America Edible Meat Industry Market

The strategic outlook for the North America Edible Meat Industry is characterized by an imperative for adaptation and innovation. Companies that prioritize sustainability, invest in advanced technologies for efficient and transparent supply chains, and diversify their product offerings to include healthier and more convenient options will be best positioned for success. The increasing consumer demand for protein, coupled with evolving dietary trends, presents significant opportunities for both traditional meat producers and those exploring alternative protein sources. Strategic partnerships, mergers, and acquisitions will continue to play a vital role in market consolidation and expansion. A focus on direct-to-consumer models and leveraging the growing online channel will be crucial for enhanced market penetration and customer engagement. Ultimately, long-term growth will depend on the industry's ability to address environmental concerns, meet evolving consumer health expectations, and maintain resilient supply chains in a dynamic global landscape.

North America Edible Meat Industry Segmentation

-

1. Type

- 1.1. Beef

- 1.2. Mutton

- 1.3. Pork

- 1.4. Poultry

- 1.5. Other Meat

-

2. Form

- 2.1. Canned

- 2.2. Fresh / Chilled

- 2.3. Frozen

- 2.4. Processed

-

3. Distribution Channel

-

3.1. Off-Trade

- 3.1.1. Convenience Stores

- 3.1.2. Online Channel

- 3.1.3. Supermarkets and Hypermarkets

- 3.1.4. Others

- 3.2. On-Trade

-

3.1. Off-Trade

North America Edible Meat Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Edible Meat Industry Regional Market Share

Geographic Coverage of North America Edible Meat Industry

North America Edible Meat Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Beef

- 5.1.2. Mutton

- 5.1.3. Pork

- 5.1.4. Poultry

- 5.1.5. Other Meat

- 5.2. Market Analysis, Insights and Forecast - by Form

- 5.2.1. Canned

- 5.2.2. Fresh / Chilled

- 5.2.3. Frozen

- 5.2.4. Processed

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Off-Trade

- 5.3.1.1. Convenience Stores

- 5.3.1.2. Online Channel

- 5.3.1.3. Supermarkets and Hypermarkets

- 5.3.1.4. Others

- 5.3.2. On-Trade

- 5.3.1. Off-Trade

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Edible Meat Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Beef

- 6.1.2. Mutton

- 6.1.3. Pork

- 6.1.4. Poultry

- 6.1.5. Other Meat

- 6.2. Market Analysis, Insights and Forecast - by Form

- 6.2.1. Canned

- 6.2.2. Fresh / Chilled

- 6.2.3. Frozen

- 6.2.4. Processed

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Off-Trade

- 6.3.1.1. Convenience Stores

- 6.3.1.2. Online Channel

- 6.3.1.3. Supermarkets and Hypermarkets

- 6.3.1.4. Others

- 6.3.2. On-Trade

- 6.3.1. Off-Trade

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 NH Foods Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Vion Grou

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Tyson Foods Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Perdue Farms Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sysco Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 The Kraft Heinz Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Foster Farms Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Continental Grain Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Hormel Foods Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Cargill Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Marfrig Global Foods S A

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 The Clemens Family Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 JBS SA

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 OSI Group

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 NH Foods Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Edible Meat Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Edible Meat Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Edible Meat Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Edible Meat Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 3: North America Edible Meat Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: North America Edible Meat Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Edible Meat Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: North America Edible Meat Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 7: North America Edible Meat Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 8: North America Edible Meat Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States North America Edible Meat Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Edible Meat Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Edible Meat Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Edible Meat Industry?

The projected CAGR is approximately 4.96%.

2. Which companies are prominent players in the North America Edible Meat Industry?

Key companies in the market include NH Foods Ltd, Vion Grou, Tyson Foods Inc, Perdue Farms Inc, Sysco Corporation, The Kraft Heinz Company, Foster Farms Inc, Continental Grain Company, Hormel Foods Corporation, Cargill Inc, Marfrig Global Foods S A, The Clemens Family Corporation, JBS SA, OSI Group.

3. What are the main segments of the North America Edible Meat Industry?

The market segments include Type, Form, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 216.98 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Low-Fat and Low-Calorie Food; Increasing Product Innovation.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

; Threat of New Entrants; Bargaining Power of Buyers/Consumers; Bargaining Power of Suppliers; Threat of Substitute Products; Degree Of Competition.

8. Can you provide examples of recent developments in the market?

February 2023: Sysco Corporation has launched its new ‘Recipe for Sustainability’ program. Through this program, Sysco will collaborate with top Students at Arizona State University and Pennsylvania State University to explore innovations that will accelerate climate action and lead the industry towards a more sustainable future.December 2022: JBS USA, a subsidiary of JBS SA, announced it reached an agreement to acquire certain assets from TriOak Foods for an undisclosed amount. Operations of TriOak Foods include live pork production, grain merchandising, and fertilizer marketing.July 2022: Cargill Incorporated partnered with Continental Grain Company to acquire Sanderson Farms. Upon completion of the acquisition, Cargill and Continental Grain will combine Sanderson Farms with Wayne Farms, a subsidiary of Continental Grain, to form a new, privately held poultry business. The combination of Sanderson Farms and Wayne Farms will create a best-in-class US poultry company with a high-quality asset base, complementary operating cultures, and an industry-leading management team and workforce.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Edible Meat Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Edible Meat Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Edible Meat Industry?

To stay informed about further developments, trends, and reports in the North America Edible Meat Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence