Key Insights

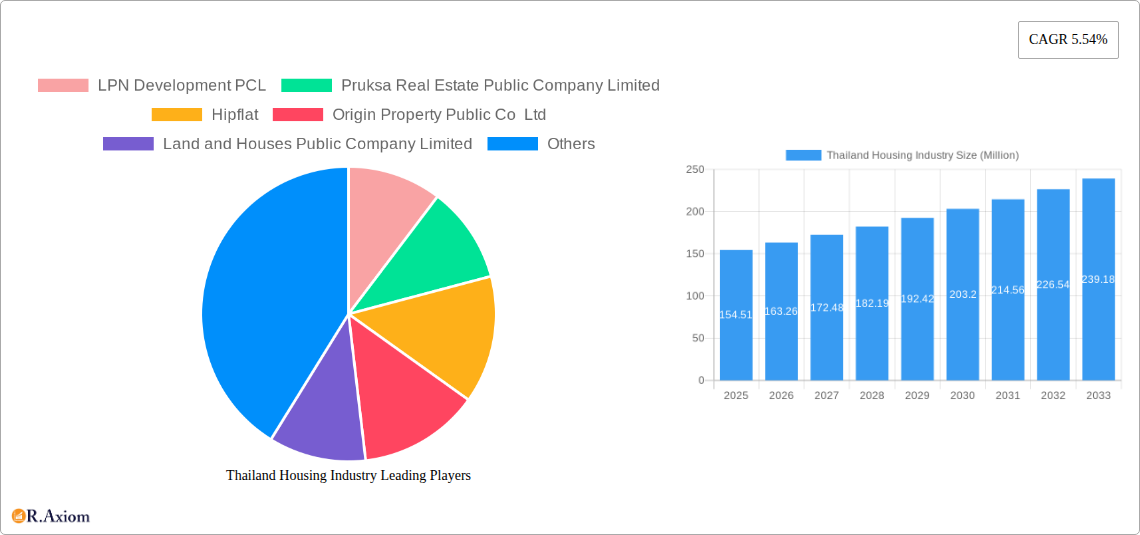

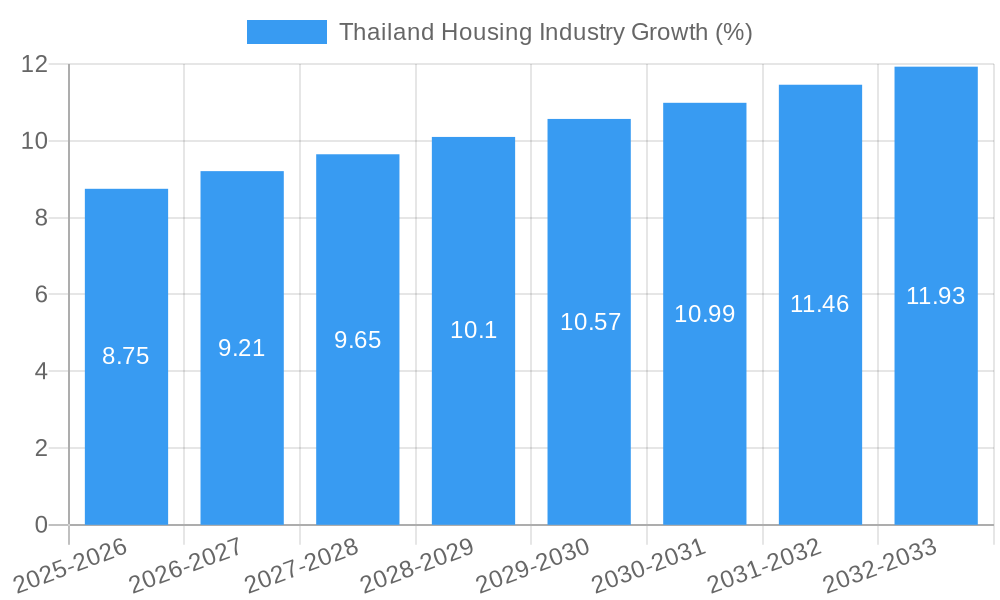

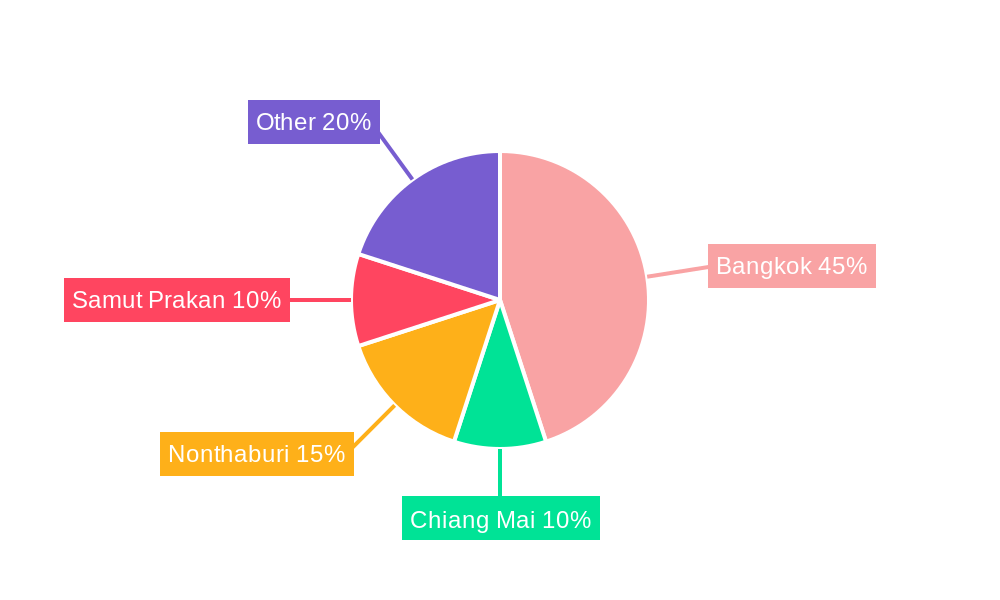

The Thailand housing market, valued at $154.51 million in 2025, is projected to experience robust growth, driven by a burgeoning population, increasing urbanization, and a rising middle class with greater disposable income. The 5.54% CAGR (Compound Annual Growth Rate) indicates a steady expansion throughout the forecast period (2025-2033). Key market segments include apartments and condominiums, which are likely to dominate due to affordability and location advantages in major cities like Bangkok. Landed houses and villas cater to a higher-end market segment, and their growth will be influenced by factors such as land availability and luxury property demand. Significant growth is anticipated in key cities like Bangkok, Chiang Mai, Nonthaburi, and Samut Prakan, reflecting these areas' economic dynamism and population concentration. Challenges could include fluctuating interest rates, government regulations concerning property development and land use, and potential shifts in consumer preferences. Major players like LPN Development PCL, Pruksa Real Estate, and Sansiri Public Co Ltd are expected to maintain strong market positions, while competition from emerging developers will continue to intensify. The market's future trajectory will depend on the government's policies supporting housing affordability, infrastructure development that enhances connectivity, and the overall stability of the Thai economy.

The competitive landscape is characterized by a mix of large established developers and smaller niche players. The success of these companies hinges on their ability to adapt to evolving consumer preferences, leverage technological advancements in construction and marketing, and create innovative housing solutions that meet the diverse needs of the Thai market. Factors influencing growth will include effective marketing strategies, sustainable construction practices, and the capacity to provide attractive financing options. While the existing market data focuses on 2025, extrapolating from the provided CAGR allows for a reasonable estimation of future market values and trends. Continued economic growth and government initiatives in the housing sector are key drivers that contribute to a positive outlook for the Thailand housing market over the coming years.

This comprehensive report provides a detailed analysis of the Thailand housing industry, encompassing market size, segmentation, growth drivers, challenges, and key players. The report covers the period 2019-2033, with a focus on the estimated year 2025 and a forecast period of 2025-2033. This in-depth study is essential for industry stakeholders, investors, and anyone seeking to understand the dynamics of this rapidly evolving market.

Thailand Housing Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the Thai housing market, examining market concentration, innovation drivers, regulatory influences, and market dynamics. The analysis includes an assessment of mergers and acquisitions (M&A) activity and its impact on market share. We explore the role of technological advancements, evolving consumer preferences, and the influence of substitute products.

Market Concentration: The Thai housing market exhibits a moderately concentrated structure, with a few large players holding significant market share. For example, in 2024, Sansiri Public Co Ltd held an estimated xx% market share, followed by Land and Houses Public Company Limited with xx%. The remaining market share is distributed among numerous smaller developers. Further analysis reveals a growing trend towards consolidation through M&A activities.

Innovation Drivers: Key innovation drivers include the adoption of sustainable building materials, smart home technologies, and prefabricated construction methods to enhance efficiency and affordability. Government initiatives promoting green building practices further stimulate innovation.

Regulatory Framework: The regulatory environment influences housing development through building codes, land-use regulations, and environmental standards. Changes in these regulations directly impact construction costs and project timelines.

Product Substitutes: The market faces competition from alternative housing options such as rental apartments and shared living spaces, impacting demand for traditional housing types.

End-User Trends: The increasing preference for environmentally friendly and technologically advanced homes drives innovation in the housing sector. Demand for larger living spaces in suburban areas is also impacting market segmentation.

M&A Activity: In the period 2019-2024, the total value of M&A deals in the Thai housing sector reached approximately $XX Million, reflecting the ongoing consolidation efforts within the industry. Key deals included [mention specific examples if data is available].

Thailand Housing Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the Thai housing market, providing a comprehensive understanding of market dynamics. We analyze market growth drivers, the impact of technological advancements, shifting consumer preferences, and the competitive dynamics that influence market share. The analysis includes projections for Compound Annual Growth Rate (CAGR) and market penetration.

The Thai housing market experienced a CAGR of xx% between 2019 and 2024, driven primarily by factors such as [mention specific drivers like economic growth, urbanization, government policies, etc.]. Technological disruptions, such as the use of Building Information Modeling (BIM) and 3D printing, are slowly increasing efficiency and reducing costs. Consumer preferences are shifting towards sustainable and technologically advanced housing solutions. The increased adoption of smart home features and eco-friendly building materials is reshaping the market. Intense competition among developers is driving innovation and influencing pricing strategies. This section further analyzes the impact of these factors on market penetration and growth projections. Market penetration for condominium units in Bangkok, for instance, reached approximately xx% in 2024 and is projected to reach xx% by 2033.

Dominant Markets & Segments in Thailand Housing Industry

This section identifies the leading segments within the Thai housing market by type (apartments and condominiums, landed houses and villas) and key cities (Bangkok, Chiang Mai, Nonthaburi, Samut Prakan). We analyze the drivers behind the dominance of specific segments and regions, including economic policies, infrastructure development, and consumer preferences.

By Type:

Apartments and Condominiums: Bangkok dominates this segment due to high population density, strong rental demand, and favorable government policies. The segment enjoys higher growth projection due to high demand from younger professionals.

Landed Houses and Villas: Suburban areas surrounding Bangkok, such as Nonthaburi and Samut Prakan, show stronger growth in this segment, driven by a preference for larger living spaces and a more tranquil environment.

By Key Cities:

Bangkok: This is the dominant market due to its high population density, economic activity, and well-established infrastructure.

Chiang Mai: This city attracts a significant amount of foreign investment and tourism, leading to growth in the housing market, particularly in the higher-end segments.

Nonthaburi & Samut Prakan: These surrounding provinces benefit from proximity to Bangkok and improved infrastructure, fueling demand for landed properties.

The detailed dominance analysis shows that Bangkok holds the largest market share for both apartments/condominiums and landed properties, although other areas are experiencing considerable growth.

Thailand Housing Industry Product Developments

The Thai housing industry witnesses continuous product innovation, driven by technological advancements and changing consumer preferences. Smart home technologies, sustainable building materials (like bamboo and recycled materials), and prefabricated construction methods are gaining popularity. These innovations enhance energy efficiency, reduce environmental impact, and offer improved living experiences, aligning with the growing demand for sustainable and technologically advanced housing. The market is adapting to offer diverse housing options catering to various income levels and lifestyles.

Report Scope & Segmentation Analysis

This report segments the Thai housing market by property type (apartments and condominiums, landed houses and villas) and key cities (Bangkok, Chiang Mai, Nonthaburi, Samut Prakan). Growth projections and market sizes are provided for each segment. Competitive dynamics within each segment are also analyzed, providing valuable insights into the market’s structure and potential.

Apartments and Condominiums: This segment shows strong growth potential, particularly in Bangkok, driven by high population density and rental demand. The market is highly competitive, with numerous developers offering a wide range of properties.

Landed Houses and Villas: This segment is growing rapidly in suburban areas, driven by a preference for larger living spaces and more tranquil environments. Competition is moderate, with a mix of large and small developers.

Bangkok: This city dominates the market due to high population density and economic activity. Competition is fierce across all housing types.

Chiang Mai: This market exhibits strong growth, driven by tourism and foreign investment. Competition is moderate.

Nonthaburi & Samut Prakan: These areas benefit from their proximity to Bangkok, experiencing growth in both segments. Competition is moderate.

Key Drivers of Thailand Housing Industry Growth

The Thai housing market's growth is propelled by several key factors. Strong economic growth fuels consumer confidence and purchasing power. Urbanization drives demand for housing, particularly in major cities. Government policies and infrastructure development projects play a critical role in shaping market dynamics. Furthermore, favorable interest rates and mortgage financing options make homeownership more accessible.

Challenges in the Thailand Housing Industry Sector

Several challenges hinder the Thai housing industry. Strict land ownership regulations and building permits can increase development costs and timelines. Supply chain disruptions impact construction costs and project completion. Intense competition among developers necessitates innovative product offerings and competitive pricing strategies. Fluctuations in the global economy and the availability of construction materials add further complexity.

Emerging Opportunities in Thailand Housing Industry

The Thai housing market presents several emerging opportunities. The rising adoption of sustainable building practices and green technologies creates new market segments. The growth of the digital economy fuels demand for digitally integrated housing solutions (smart homes). The increasing focus on affordable housing opens opportunities for developers to explore innovative and cost-effective construction techniques.

Leading Players in the Thailand Housing Industry Market

- LPN Development PCL

- Pruksa Real Estate Public Company Limited

- Hipflat

- Origin Property Public Co Ltd

- Land and Houses Public Company Limited

- Supalai Company Limited

- Property Perfect Public Company Limited

- Sansiri Public Co Ltd

- AP (THAILAND) PUBLIC COMPANY LIMITED

- Ananda Development Public Company Limited

- Quality Houses Public Company Limited

- Magnolia Quality Development Corp Co Ltd

Key Developments in Thailand Housing Industry Industry

- 2022 Q4: Launch of a new sustainable housing project by Sansiri Public Co Ltd.

- 2023 Q1: Merger between two mid-sized developers resulting in increased market share.

- 2024 Q2: Government introduces new incentives for green building construction.

- [Add more developments with year/month and impact]

Strategic Outlook for Thailand Housing Industry Market

The Thai housing market presents significant long-term growth potential, driven by continued economic expansion, urbanization, and evolving consumer preferences. Strategic initiatives focused on sustainable development, technological innovation, and catering to diverse housing needs will be essential for success. The market will continue to see consolidation among developers, with an increased focus on building sustainable and smart homes.

Thailand Housing Industry Segmentation

-

1. Type

- 1.1. Apartments and Condominiums

- 1.2. Landed Houses and Villas

-

2. Key Cities

- 2.1. Bangkok

- 2.2. Chiang Mais

- 2.3. Nontha Buri

- 2.4. Samut Prakan

Thailand Housing Industry Segmentation By Geography

- 1. Thailand

Thailand Housing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.54% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Government initiatives and huge investments driving the market4.; Vision 2030 and allied projects driving the market

- 3.3. Market Restrains

- 3.3.1. 4.; High construction costs affecting the market4.; Limited land availability affecting the growth of the market

- 3.4. Market Trends

- 3.4.1. Bangkok and Vicinities Witnessing Growth in the Residential Sector

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Thailand Housing Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments and Condominiums

- 5.1.2. Landed Houses and Villas

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Bangkok

- 5.2.2. Chiang Mais

- 5.2.3. Nontha Buri

- 5.2.4. Samut Prakan

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Thailand

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 LPN Development PCL

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Pruksa Real Estate Public Company Limited

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Hipflat

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Origin Property Public Co Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Land and Houses Public Company Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Supalai Company Limited

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Property Perfect Public Company Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Sansiri Public Co Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 AP (THAILAND) PUBLIC COMPANY LIMITED

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Ananda Development Public Company Limited

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Quality Houses Public Company Limited*List Not Exhaustive

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Magnolia Quality Development Corp Co Ltd

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 LPN Development PCL

List of Figures

- Figure 1: Thailand Housing Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Thailand Housing Industry Share (%) by Company 2024

List of Tables

- Table 1: Thailand Housing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Thailand Housing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Thailand Housing Industry Revenue Million Forecast, by Key Cities 2019 & 2032

- Table 4: Thailand Housing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Thailand Housing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Thailand Housing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 7: Thailand Housing Industry Revenue Million Forecast, by Key Cities 2019 & 2032

- Table 8: Thailand Housing Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thailand Housing Industry?

The projected CAGR is approximately 5.54%.

2. Which companies are prominent players in the Thailand Housing Industry?

Key companies in the market include LPN Development PCL, Pruksa Real Estate Public Company Limited, Hipflat, Origin Property Public Co Ltd, Land and Houses Public Company Limited, Supalai Company Limited, Property Perfect Public Company Limited, Sansiri Public Co Ltd, AP (THAILAND) PUBLIC COMPANY LIMITED, Ananda Development Public Company Limited, Quality Houses Public Company Limited*List Not Exhaustive, Magnolia Quality Development Corp Co Ltd.

3. What are the main segments of the Thailand Housing Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 154.51 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Government initiatives and huge investments driving the market4.; Vision 2030 and allied projects driving the market.

6. What are the notable trends driving market growth?

Bangkok and Vicinities Witnessing Growth in the Residential Sector.

7. Are there any restraints impacting market growth?

4.; High construction costs affecting the market4.; Limited land availability affecting the growth of the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thailand Housing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thailand Housing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thailand Housing Industry?

To stay informed about further developments, trends, and reports in the Thailand Housing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence