Key Insights

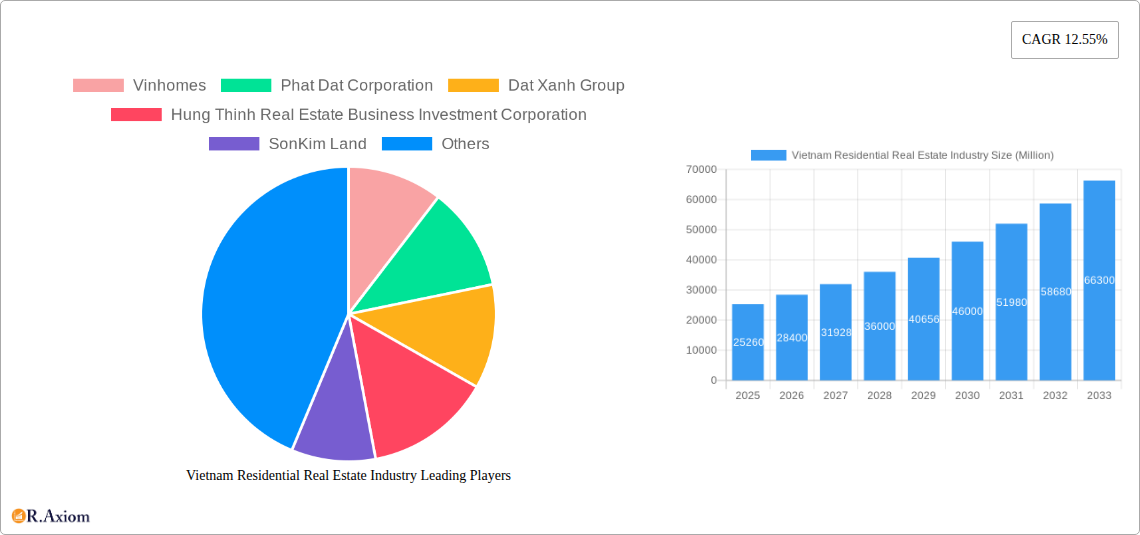

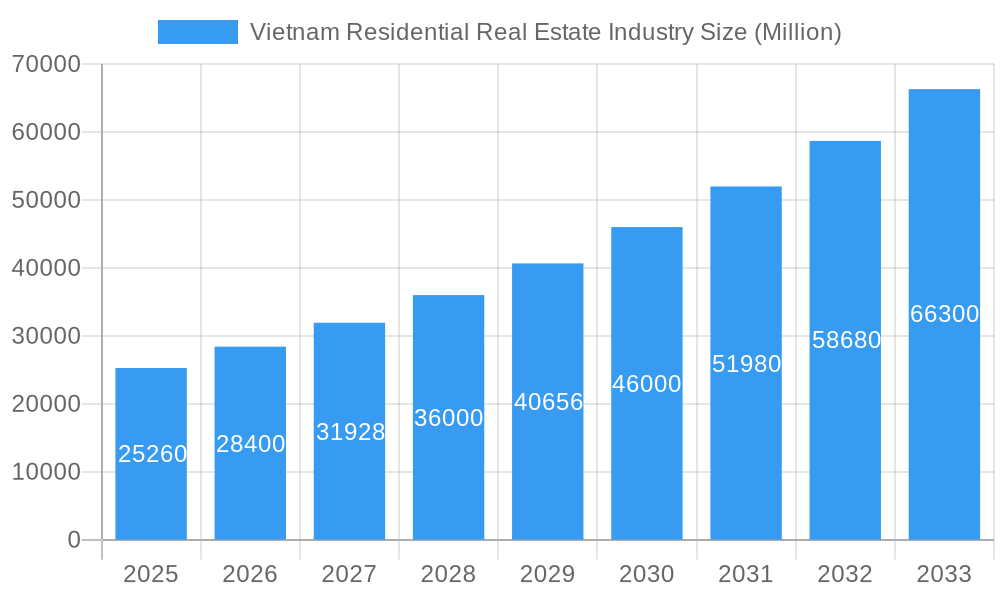

The Vietnam residential real estate market exhibits robust growth potential, projected to reach a market size of $25.26 billion in 2025, expanding at a Compound Annual Growth Rate (CAGR) of 12.55%. This growth is driven by several factors. Firstly, Vietnam's burgeoning economy and rising middle class fuel increasing demand for housing, particularly in major urban centers like Ho Chi Minh City, Hanoi, and Da Nang. Secondly, government initiatives aimed at improving infrastructure and attracting foreign investment contribute to market expansion. Thirdly, a preference for modern apartments and condominiums, alongside a continued demand for villas and landed houses, diversifies the market and fuels growth across different segments. Competition among major players like Vinhomes, Phat Dat Corporation, and Novaland Group further stimulates market activity and drives innovation in design and development. However, challenges remain, including land scarcity in prime locations and potential fluctuations in the national economy that could impact buyer confidence. Careful consideration of these factors will be crucial for developers navigating this dynamic market.

Vietnam Residential Real Estate Industry Market Size (In Billion)

Looking forward to 2033, the market is expected to continue its upward trajectory, albeit with a potentially moderating growth rate as it matures. While the initial CAGR of 12.55% may not be fully sustained throughout the forecast period, a continued strong economic performance in Vietnam, combined with ongoing urbanization and population growth, suggests a sustained period of significant growth. The segmentation into apartments/condominiums and villas/landed houses will likely continue to be important, with specific sub-segments – such as luxury properties or affordable housing – potentially experiencing different growth trajectories depending on market demand and government policy. The performance of key players will continue to be closely linked to the overall market conditions and their ability to adapt to evolving consumer preferences and economic shifts.

Vietnam Residential Real Estate Industry Company Market Share

Vietnam Residential Real Estate Industry: 2019-2033 Market Analysis & Forecast Report

This comprehensive report provides a detailed analysis of the Vietnam residential real estate industry, covering market dynamics, key players, and future growth prospects from 2019 to 2033. The report leverages extensive data and expert insights to offer actionable intelligence for investors, developers, and industry stakeholders. With a base year of 2025 and a forecast period spanning 2025-2033, this report is an invaluable resource for navigating the complexities of this rapidly evolving market. The total market size is estimated at xx Million USD in 2025, projected to reach xx Million USD by 2033.

Vietnam Residential Real Estate Industry Market Concentration & Innovation

This section analyzes the competitive landscape of Vietnam's residential real estate market, encompassing market concentration, innovation drivers, regulatory frameworks, and recent M&A activities. The market exhibits a moderately concentrated structure, with several large players holding significant market share. Vinhomes, Novaland Group, and Phat Dat Corporation are among the leading developers, while other major players include Dat Xanh Group, Hung Thinh Real Estate, Sun Group, and FLC Group. Precise market share data for 2024 is unavailable (xx%), but Vinhomes is likely to hold the largest share.

Innovation in the sector is driven by the increasing demand for sustainable and technologically advanced housing solutions. The government's focus on smart city initiatives fuels innovation in building materials, design, and property management. Regulatory frameworks, while generally supportive of growth, also present challenges, particularly concerning land acquisition and environmental regulations. Product substitutes, such as rental housing and co-living spaces, are increasingly competitive. End-user trends indicate a preference for high-quality, well-located properties with modern amenities. M&A activity remains robust, with deal values reaching xx Million USD in 2024. However, specifics on individual transactions are limited at this time (xx).

- Key Metrics: Market share (xx% in 2024, with Vinhomes estimated to hold the largest share), M&A deal values (xx Million USD in 2024).

- Key Players: Vinhomes, Novaland Group, Phat Dat Corporation, Dat Xanh Group, Hung Thinh Real Estate, Sun Group, FLC Group.

Vietnam Residential Real Estate Industry Industry Trends & Insights

The Vietnam residential real estate market is experiencing robust growth fueled by rapid urbanization, rising incomes, and favorable government policies. The Compound Annual Growth Rate (CAGR) from 2019 to 2024 is estimated at xx%, and this growth is expected to continue, albeit at a slightly moderated pace, into the forecast period. Market penetration of modern, high-rise apartments, particularly in Ho Chi Minh City and Hanoi, is high (xx%), exceeding that of villas and landed houses (xx%). Technological disruptions, such as proptech platforms and digital marketing strategies, are transforming the industry, increasing transparency and efficiency. Consumer preferences are shifting toward sustainable designs, smart home technologies, and convenient locations with access to amenities. Competitive dynamics are marked by intense competition among major developers, leading to strategic partnerships, innovative product offerings, and price adjustments.

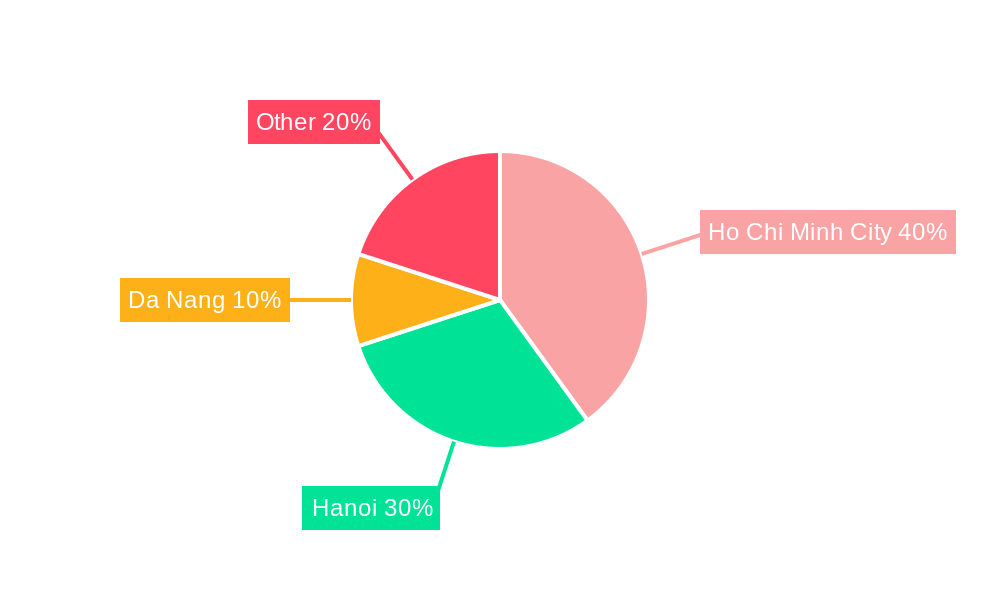

Dominant Markets & Segments in Vietnam Residential Real Estate Industry

Ho Chi Minh City and Hanoi remain the dominant markets, driving the majority of the overall market volume. Danang displays significant but smaller-scale growth.

- Ho Chi Minh City: Dominance is driven by its status as the economic and financial hub, attracting significant domestic and foreign investment. Strong economic growth and infrastructure development fuel demand.

- Hanoi: A rapidly growing capital city, Hanoi benefits from government investment in infrastructure and a large and expanding population.

- Danang: Tourism and foreign investment are key drivers for Danang's real estate sector, particularly in high-end villas and apartments.

Within property types, Apartments and Condominiums represent the largest segment, driven by affordability and higher population density in urban areas. Villas and Landed Houses continue to hold their own, especially in suburban areas and among high-net-worth individuals.

Vietnam Residential Real Estate Industry Product Developments

Product innovation focuses on sustainable building practices, smart home integration, and enhanced amenities. Developers are emphasizing energy-efficient designs, using eco-friendly materials, and incorporating technologies that improve convenience and security. This reflects a growing consumer demand for environmentally friendly and technologically advanced properties, boosting market competitiveness and attracting higher values.

Report Scope & Segmentation Analysis

This report segments the Vietnam residential real estate market by key cities (Ho Chi Minh City, Hanoi, Danang) and property types (Apartments and Condominiums, Villas and Landed Houses). Each segment's growth projections, market sizes, and competitive dynamics are analyzed in detail. The report's scope covers the historical period (2019-2024), base year (2025), estimated year (2025), and forecast period (2025-2033).

Key Drivers of Vietnam Residential Real Estate Industry Growth

Several factors are driving the growth of Vietnam’s residential real estate sector. Rapid urbanization and a growing middle class fuel demand. Government initiatives supporting infrastructure development and affordable housing further accelerate growth. Economic progress and increased foreign investment contribute substantially to the overall market expansion.

Challenges in the Vietnam Residential Real Estate Industry Sector

Challenges include land scarcity in major cities, stringent regulatory approvals, and potential fluctuations in the overall economy. Supply chain disruptions can cause delays and cost increases. Competition among developers remains intense, impacting pricing and profitability. These factors influence project timelines and overall financial stability.

Emerging Opportunities in Vietnam Residential Real Estate Industry

Opportunities exist in developing sustainable and eco-friendly housing solutions, integrating smart technologies, and expanding into secondary cities. The growing demand for co-living spaces and rental housing presents further expansion potential. These opportunities align with evolving consumer preferences and global trends.

Leading Players in the Vietnam Residential Real Estate Industry Market

- Vinhomes

- Phat Dat Corporation

- Dat Xanh Group

- Hung Thinh Real Estate Business Investment Corporation

- SonKim Land

- Sun Group

- Capital and Limited (List Not Exhaustive)

- FLC Group

- Rever

- Phu My Hung Development Corporation

- Novaland Group

Key Developments in Vietnam Residential Real Estate Industry Industry

- October 2023: Phat Dat's investment project of more than 10,000 billion VND in Binh Duong was approved for planning.

- November 2023: Phat Dat Real Estate and MB Bank signed a cooperation agreement for financial sponsorship of investors and customers for the Thuan An 1&2 high-rise housing complex (investment exceeding 10,800 billion VND).

Strategic Outlook for Vietnam Residential Real Estate Industry Market

The Vietnam residential real estate market presents significant long-term growth potential. Continued urbanization, economic expansion, and supportive government policies should fuel demand. Strategic partnerships, technological innovation, and a focus on sustainable development will be crucial for success in this dynamic market. The focus on sustainable development and technological innovation will shape the future success of developers in this market.

Vietnam Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Apartments and Condominiums

- 1.2. Villas and Landed Houses

-

2. Key Cities

- 2.1. Ho Chi Minh City

- 2.2. Hanoi

- 2.3. Danang

Vietnam Residential Real Estate Industry Segmentation By Geography

- 1. Vietnam

Vietnam Residential Real Estate Industry Regional Market Share

Geographic Coverage of Vietnam Residential Real Estate Industry

Vietnam Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments and Condominiums

- 5.1.2. Villas and Landed Houses

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Ho Chi Minh City

- 5.2.2. Hanoi

- 5.2.3. Danang

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Vietnam

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Vietnam Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Apartments and Condominiums

- 6.1.2. Villas and Landed Houses

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Ho Chi Minh City

- 6.2.2. Hanoi

- 6.2.3. Danang

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Vinhomes

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Phat Dat Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Dat Xanh Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hung Thinh Real Estate Business Investment Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 SonKim Land

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Sun Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Capital and Limited**List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 FLC Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rever

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Phu My Hung Development Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Novaland Group

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Vinhomes

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Vietnam Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Vietnam Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Vietnam Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Vietnam Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Vietnam Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Vietnam Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Vietnam Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Vietnam Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vietnam Residential Real Estate Industry?

The projected CAGR is approximately 12.55%.

2. Which companies are prominent players in the Vietnam Residential Real Estate Industry?

Key companies in the market include Vinhomes, Phat Dat Corporation, Dat Xanh Group, Hung Thinh Real Estate Business Investment Corporation, SonKim Land, Sun Group, Capital and Limited**List Not Exhaustive, FLC Group, Rever, Phu My Hung Development Corporation, Novaland Group.

3. What are the main segments of the Vietnam Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.26 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urbanization and Rising Disposable Income4.; Government Initiatives and Expanding Economy.

6. What are the notable trends driving market growth?

Rising Government Initiatives and Social Housing Development Policies.

7. Are there any restraints impacting market growth?

4.; Limited Land Availability4.; Economic Uncertainties.

8. Can you provide examples of recent developments in the market?

November 2023: Phat Dat Real Estate Development Joint Stock Company and Military Commercial Joint Stock Bank (MB Bank) signed a comprehensive cooperation agreement with the purpose of financial sponsorship for investors and customers. Products at Phat Dat projects. The sponsored project is the Thuan An 1&2 high-rise housing complex with a scale of 4.47 hectares, located in a prime location right in the central area of Thuan An City, connected to many large industrial clusters in Binh Duong. The project has completed its legality with an investment of more than 10,800 billion VND, including apartment products, shophouses, and townhouses.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vietnam Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vietnam Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vietnam Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Vietnam Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence