Key Insights

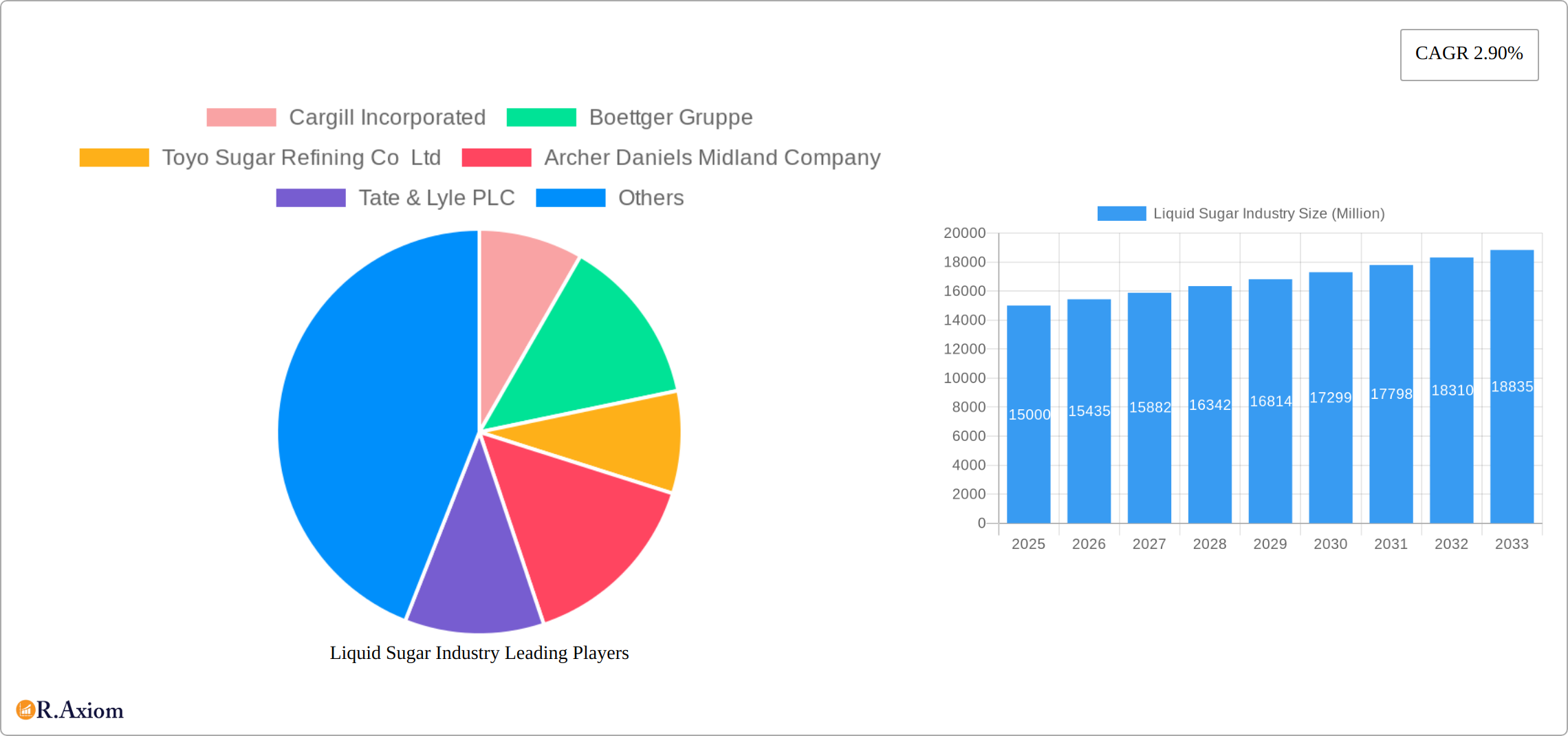

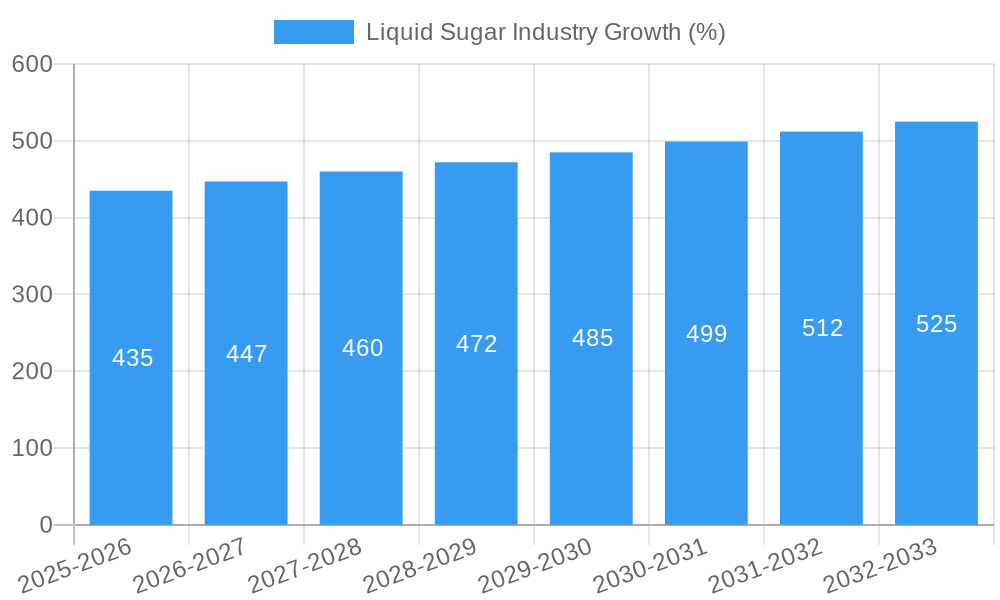

The global liquid sugar market, valued at approximately $XX million in 2025, is projected to experience steady growth, exhibiting a compound annual growth rate (CAGR) of 2.90% from 2025 to 2033. This growth is fueled by several key drivers. The increasing demand for convenient and efficient sweeteners in the food and beverage industry is a significant factor. Liquid sugar offers ease of handling and incorporation into various food products compared to granulated sugar, making it attractive to manufacturers, especially in large-scale operations. The rising popularity of ready-to-drink beverages, bakery items, and confectionery products further contributes to the market's expansion. Moreover, the growing awareness of health and wellness is indirectly driving demand for liquid sugar, particularly in the organic segment as it allows for precise sweetness control and enhances product quality. However, the market faces certain restraints, including price volatility of raw materials (sugarcane and sugar beet) and concerns about the high caloric content of sugar, leading to increased interest in sugar substitutes. The organic segment, though a smaller part of the market currently, shows promising growth potential driven by increasing consumer preference for natural and healthier food options.

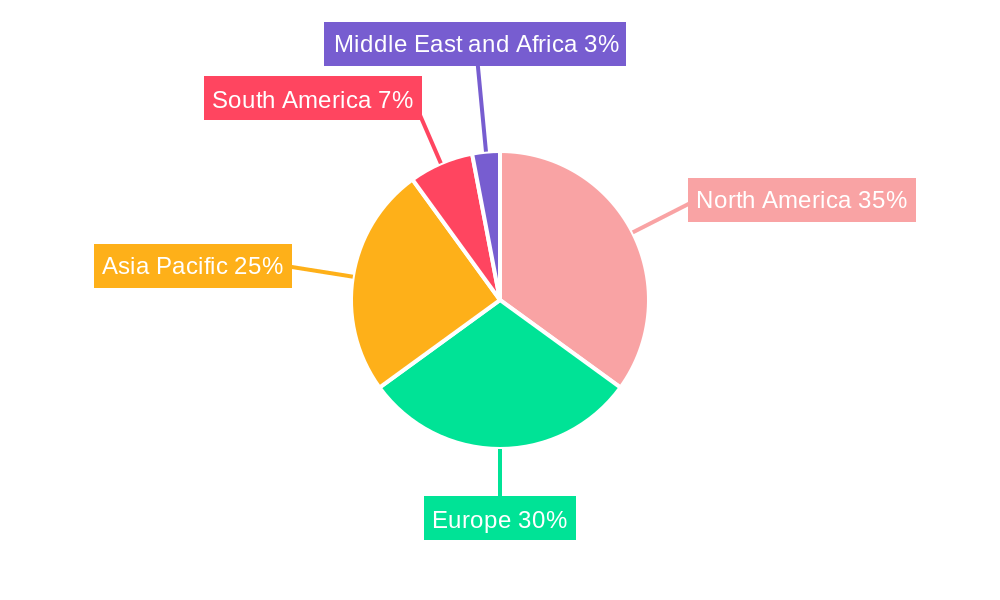

Segmentation reveals a diverse market landscape. The application segment is dominated by the food and beverage industry, with bakery, confectionery, and beverage applications collectively accounting for a significant portion of the overall demand. The growing baby food industry also contributes to the market, albeit to a lesser extent. Geographically, North America and Europe currently hold substantial market shares, driven by established food processing industries and high per capita consumption of sweetened products. However, the Asia-Pacific region is anticipated to exhibit significant growth potential in the coming years, fueled by rapid economic development, urbanization, and increasing disposable incomes in developing economies. Key players in this market, including Cargill Incorporated, Archer Daniels Midland Company, and Tate & Lyle PLC, are constantly innovating to enhance product offerings and cater to the changing demands of consumers and the industry. The competitive landscape is characterized by both large multinational corporations and regional players. Future growth hinges on maintaining a balance between meeting the demand for affordable, convenient sweeteners while addressing health and sustainability concerns.

Liquid Sugar Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the global liquid sugar industry, covering market size, segmentation, key players, trends, and future prospects. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report offers actionable insights for industry stakeholders, including manufacturers, suppliers, distributors, and investors. With a focus on key market drivers and challenges, this report serves as an invaluable resource for strategic decision-making.

Liquid Sugar Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the liquid sugar industry, exploring market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and merger & acquisition (M&A) activities.

The global liquid sugar market exhibits a moderately concentrated structure, with a few major players holding significant market share. While precise market share figures for individual companies are proprietary and vary depending on the specific segment (organic vs. conventional; applications etc.), Cargill Incorporated, Archer Daniels Midland Company, and Tate & Lyle PLC are consistently ranked among the top players globally. Their combined market share is estimated to be around xx% in 2025. Smaller players, such as Boettger Gruppe, Toyo Sugar Refining Co Ltd, Sucroliq S A P I DE C V, Galam Group, Zukan S L U, Nordzucker AG, and Sugar Australia Company Ltd, collectively account for a significant portion of the market, often focusing on regional niches or specialized applications.

Innovation Drivers:

- Technological advancements: Improved refining processes, efficient transportation and storage solutions, and the development of new sweetener technologies drive innovation.

- Consumer demand: Growing consumer preference for healthier and more natural sweeteners is driving the development of organic and sustainably sourced liquid sugar.

- Regulatory pressures: Stringent regulations regarding food safety and labeling are influencing innovation in product formulations and production processes.

M&A Activity: Over the historical period (2019-2024), M&A activity in the liquid sugar industry was moderate, with deal values averaging around xx Million USD per transaction. These activities primarily focused on expanding market reach, enhancing product portfolios, and securing access to raw materials.

Product Substitutes: The market faces competition from alternative sweeteners like high-fructose corn syrup, artificial sweeteners, and honey, impacting overall market share.

Liquid Sugar Industry Industry Trends & Insights

The global liquid sugar market is experiencing robust growth, driven by factors such as increasing demand from the food and beverage industry, rising consumer disposable incomes in emerging economies, and expanding applications across diverse sectors. The market is projected to register a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is primarily fueled by the escalating demand for liquid sugar in the confectionery, bakery, and beverage industries. Market penetration within these sectors is high and expected to continue rising due to the versatility of liquid sugar as a key ingredient.

Technological disruptions, such as the development of more efficient sugar refining technologies and the exploration of alternative sugar sources, contribute to improving production efficiency and lowering costs. However, consumer preferences are increasingly shifting towards healthier and more sustainable options, impacting market dynamics. For example, growing concerns about added sugar are driving demand for organic and sustainably sourced liquid sugar. The intense competition among established players and the emergence of new entrants necessitates strategic innovation and competitive pricing strategies.

Dominant Markets & Segments in Liquid Sugar Industry

The global liquid sugar market exhibits significant geographic diversity, with regional variations influencing market share and growth trajectories. While precise market dominance data is often proprietary and fluctuates annually, the Asia-Pacific region consistently emerges as a key player, driven by its high population density and rapidly expanding economies. Within this region, China and India are particularly significant markets. North America and Europe also maintain substantial market shares, characterized by established industry players and relatively high per capita consumption of liquid sugar.

Key Drivers of Regional Dominance:

- Economic Policies and Government Support: Supportive government policies and initiatives targeting agricultural development and food processing significantly impact regional market growth. Subsidies, tax incentives, and streamlined regulations can foster industry expansion.

- Robust Infrastructure: Efficient transportation networks, modern storage facilities, and streamlined distribution channels are essential for successful market operations. A well-developed infrastructure minimizes logistical challenges and ensures timely product delivery.

- Consumer Preferences and Cultural Factors: Regional variations in dietary habits, food and beverage consumption patterns, and cultural preferences directly influence the demand for liquid sugar. Understanding these nuances is vital for targeted market strategies.

Segment Dominance:

- Application-Based Segmentation: The beverage industry remains the dominant consumer of liquid sugar globally, owing to its widespread use in soft drinks, juices, and other ready-to-drink beverages. The confectionery and bakery sectors also represent significant and growing market segments, fueled by the continuous expansion of these industries. While a niche segment, the demand for liquid sugar in baby food applications is also experiencing notable growth.

- Product Type Segmentation: Conventional liquid sugar currently holds the largest market share due to its cost-effectiveness and widespread availability. However, the organic liquid sugar segment is experiencing robust growth, driven by increasing consumer awareness of health and wellness, and a preference for natural and sustainably produced ingredients. This trend reflects a broader shift towards clean-label products across various food and beverage categories.

Liquid Sugar Industry Product Developments

Recent product innovations focus on enhancing product quality, expanding applications, and catering to evolving consumer preferences. These include the development of organic liquid sugars, high-fructose liquid sugars with improved functionality, and customized liquid sugar blends tailored to specific applications. Companies are also leveraging technology to enhance the efficiency and sustainability of production processes. The competitive advantage lies in developing innovative products with superior quality, cost-effectiveness, and a strong sustainability profile that aligns with consumer demands.

Report Scope & Segmentation Analysis

This report segments the liquid sugar market based on origin (organic and conventional) and application (bakery, confectionery, beverages, baby foods, and other applications). Each segment is analyzed in detail, providing insights into market size, growth projections, and competitive dynamics for the period 2019-2033. The organic segment projects a higher CAGR than conventional due to growing health consciousness, while beverage remains the dominant application segment. Competition varies across segments, with a greater number of smaller players in the organic and niche application segments compared to the larger, more established players in the conventional and major application segments.

Key Drivers of Liquid Sugar Industry Growth

The sustained growth of the liquid sugar industry is propelled by a confluence of factors:

- Expanding Global Demand: The burgeoning global population and the continued growth of the food and beverage sector are fundamental drivers of increased liquid sugar demand. This is particularly evident in developing economies experiencing rising disposable incomes.

- Technological Advancements in Production: Continuous improvements in sugar refining and processing technologies enhance production efficiency, reduce waste, and improve product quality. Automation and precision engineering contribute to optimizing production processes.

- Favorable Economic Conditions and Rising Disposable Incomes: Rising disposable incomes in developing nations lead to increased consumer spending on processed foods and beverages, which directly translates to higher demand for liquid sugar.

- Globalization and International Trade: Increased global trade and interconnected supply chains facilitate the seamless flow of liquid sugar across international borders, fostering market expansion and access to wider consumer bases.

Challenges in the Liquid Sugar Industry Sector

Despite its growth potential, the liquid sugar industry faces several challenges that impact profitability and sustainability:

- Volatility in Raw Material Prices: Fluctuations in the prices of sugarcane and sugar beets, the primary raw materials for liquid sugar production, significantly impact production costs and profitability. Effective risk management strategies are crucial to mitigate these price swings.

- Stringent Regulatory Compliance: Meeting stringent food safety and labeling regulations necessitates significant investment in quality control and compliance measures, adding to the overall cost of production. This includes adhering to international standards and local regulations.

- Intense Competition from Alternative Sweeteners: The availability of alternative sweeteners, such as high-fructose corn syrup and artificial sweeteners, creates competitive pressure within the market. To maintain market share, producers must focus on differentiation and value-added propositions.

- Sustainability Concerns and Environmental Impact: Growing consumer awareness of the environmental impact of sugar production necessitates the adoption of sustainable agricultural practices and environmentally friendly processing methods. Meeting these expectations is becoming increasingly crucial for maintaining a positive brand image.

Emerging Opportunities in Liquid Sugar Industry

The liquid sugar industry presents several promising opportunities for growth and innovation:

- Rising Demand for Organic and Sustainably Sourced Sugar: The increasing consumer preference for organic and sustainably produced food products presents a significant opportunity for producers to cater to this growing market segment. Certifications and transparent supply chains are key to success in this area.

- Expansion into New and Emerging Markets: Untapped markets in rapidly developing economies in Asia and Africa offer significant growth potential for liquid sugar producers. Strategic market entry strategies are crucial for success in these regions.

- Development of Innovative Liquid Sugar Products: Creating specialized liquid sugar blends tailored to specific applications, such as functional beverages or specialized food products, can unlock new market segments and enhance profitability. Research and development play a vital role in this area.

- Value-Added Products and Functional Ingredients: Developing value-added products and incorporating liquid sugar as a functional ingredient in various food and beverage applications can enhance profitability and expand market reach.

Leading Players in the Liquid Sugar Industry Market

- Cargill Incorporated

- Boettger Gruppe

- Toyo Sugar Refining Co Ltd

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Sucroliq S A P I DE C V

- Galam Group

- Zukan S L U

- Nordzucker AG

- Sugar Australia Company Ltd

Key Developments in Liquid Sugar Industry Industry

- August 2022: The National Sugar Institute of Kanpur launched sugar syrup from jowar stem, offering a new, honey-like alternative. This development could significantly diversify liquid sugar sources.

- September 2022: Archer Daniels Midland Company opened a new science and technology center in China, focusing on innovation in the nutrition and health industry. This underscores the company's commitment to technological advancement in the liquid sugar market.

- January 2024: Elo Life Systems secured USD 20.5 Million in Series A2 funding to develop a natural high-intensity sweetener from watermelon juice (by 2026) and sugar beet (by 2027), representing a significant step towards sustainable and innovative sugar alternatives.

Strategic Outlook for Liquid Sugar Industry Market

The liquid sugar market is projected to experience continued growth, driven by consistent demand from the food and beverage sector and the ongoing development of innovative and sustainable sugar solutions. Key strategic priorities for industry players include expanding into new and emerging markets, developing specialized liquid sugar blends to cater to diverse consumer preferences, and leveraging technological advancements to enhance production efficiency and reduce costs. A strong emphasis on health and sustainability, coupled with a focus on meeting evolving consumer demands, will likely shape the future dynamics of the liquid sugar market, creating significant opportunities for those who can effectively adapt and innovate.

Liquid Sugar Industry Segmentation

-

1. Origin

- 1.1. Organic

- 1.2. Conventional

-

2. Application

- 2.1. Bakery

- 2.2. Confectionery

- 2.3. Beverages

- 2.4. Baby Foods

- 2.5. Other Applications

Liquid Sugar Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. France

- 2.5. Italy

- 2.6. Russia

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Liquid Sugar Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.90% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Demand for Organic Variants; Thriving Food and Beverage Industry

- 3.3. Market Restrains

- 3.3.1. Sugar Under Scrutiny with New Taxes and Label Regulations

- 3.4. Market Trends

- 3.4.1. Escalating Demand for Organic Variants

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Origin

- 5.1.1. Organic

- 5.1.2. Conventional

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Bakery

- 5.2.2. Confectionery

- 5.2.3. Beverages

- 5.2.4. Baby Foods

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Origin

- 6. North America Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Origin

- 6.1.1. Organic

- 6.1.2. Conventional

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Bakery

- 6.2.2. Confectionery

- 6.2.3. Beverages

- 6.2.4. Baby Foods

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Origin

- 7. Europe Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Origin

- 7.1.1. Organic

- 7.1.2. Conventional

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Bakery

- 7.2.2. Confectionery

- 7.2.3. Beverages

- 7.2.4. Baby Foods

- 7.2.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Origin

- 8. Asia Pacific Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Origin

- 8.1.1. Organic

- 8.1.2. Conventional

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Bakery

- 8.2.2. Confectionery

- 8.2.3. Beverages

- 8.2.4. Baby Foods

- 8.2.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Origin

- 9. South America Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Origin

- 9.1.1. Organic

- 9.1.2. Conventional

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Bakery

- 9.2.2. Confectionery

- 9.2.3. Beverages

- 9.2.4. Baby Foods

- 9.2.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Origin

- 10. Middle East and Africa Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Origin

- 10.1.1. Organic

- 10.1.2. Conventional

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Bakery

- 10.2.2. Confectionery

- 10.2.3. Beverages

- 10.2.4. Baby Foods

- 10.2.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Origin

- 11. North America Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 11.1.4 Rest of North America

- 12. Europe Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Spain

- 12.1.2 United Kingdom

- 12.1.3 Germany

- 12.1.4 France

- 12.1.5 Italy

- 12.1.6 Russia

- 12.1.7 Rest of Europe

- 13. Asia Pacific Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 Rest of Asia Pacific

- 14. South America Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 Brazil

- 14.1.2 Argentina

- 14.1.3 Rest of South America

- 15. Middle East and Africa Liquid Sugar Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 South Africa

- 15.1.2 Saudi Arabia

- 15.1.3 Rest of Middle East and Africa

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Cargill Incorporated

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Boettger Gruppe

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Toyo Sugar Refining Co Ltd

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Archer Daniels Midland Company

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Tate & Lyle PLC

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Sucroliq S A P I DE C V *List Not Exhaustive

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Galam Group

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Zukan S L U

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Nordzucker AG

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Sugar Australia Company Ltd

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Cargill Incorporated

List of Figures

- Figure 1: Global Liquid Sugar Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: South America Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Liquid Sugar Industry Revenue (Million), by Origin 2024 & 2032

- Figure 13: North America Liquid Sugar Industry Revenue Share (%), by Origin 2024 & 2032

- Figure 14: North America Liquid Sugar Industry Revenue (Million), by Application 2024 & 2032

- Figure 15: North America Liquid Sugar Industry Revenue Share (%), by Application 2024 & 2032

- Figure 16: North America Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Liquid Sugar Industry Revenue (Million), by Origin 2024 & 2032

- Figure 19: Europe Liquid Sugar Industry Revenue Share (%), by Origin 2024 & 2032

- Figure 20: Europe Liquid Sugar Industry Revenue (Million), by Application 2024 & 2032

- Figure 21: Europe Liquid Sugar Industry Revenue Share (%), by Application 2024 & 2032

- Figure 22: Europe Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Liquid Sugar Industry Revenue (Million), by Origin 2024 & 2032

- Figure 25: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Origin 2024 & 2032

- Figure 26: Asia Pacific Liquid Sugar Industry Revenue (Million), by Application 2024 & 2032

- Figure 27: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: South America Liquid Sugar Industry Revenue (Million), by Origin 2024 & 2032

- Figure 31: South America Liquid Sugar Industry Revenue Share (%), by Origin 2024 & 2032

- Figure 32: South America Liquid Sugar Industry Revenue (Million), by Application 2024 & 2032

- Figure 33: South America Liquid Sugar Industry Revenue Share (%), by Application 2024 & 2032

- Figure 34: South America Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: South America Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Liquid Sugar Industry Revenue (Million), by Origin 2024 & 2032

- Figure 37: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Origin 2024 & 2032

- Figure 38: Middle East and Africa Liquid Sugar Industry Revenue (Million), by Application 2024 & 2032

- Figure 39: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Application 2024 & 2032

- Figure 40: Middle East and Africa Liquid Sugar Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Liquid Sugar Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Liquid Sugar Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 3: Global Liquid Sugar Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Global Liquid Sugar Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Spain Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United Kingdom Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Germany Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Italy Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Russia Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Rest of Europe Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: China Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Japan Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: India Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Australia Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Rest of Asia Pacific Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 25: Brazil Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Argentina Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Rest of South America Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: South Africa Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Saudi Arabia Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Rest of Middle East and Africa Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Global Liquid Sugar Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 33: Global Liquid Sugar Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 34: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 35: United States Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Canada Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Mexico Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Rest of North America Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global Liquid Sugar Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 40: Global Liquid Sugar Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 41: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: Spain Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: United Kingdom Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Germany Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: France Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Italy Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Russia Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Europe Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Global Liquid Sugar Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 50: Global Liquid Sugar Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 51: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: China Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: Japan Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: India Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Australia Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Asia Pacific Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: Global Liquid Sugar Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 58: Global Liquid Sugar Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 59: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 60: Brazil Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Argentina Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 62: Rest of South America Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 63: Global Liquid Sugar Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 64: Global Liquid Sugar Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 65: Global Liquid Sugar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 66: South Africa Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 67: Saudi Arabia Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 68: Rest of Middle East and Africa Liquid Sugar Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Sugar Industry?

The projected CAGR is approximately 2.90%.

2. Which companies are prominent players in the Liquid Sugar Industry?

Key companies in the market include Cargill Incorporated, Boettger Gruppe, Toyo Sugar Refining Co Ltd, Archer Daniels Midland Company, Tate & Lyle PLC, Sucroliq S A P I DE C V *List Not Exhaustive, Galam Group, Zukan S L U, Nordzucker AG, Sugar Australia Company Ltd.

3. What are the main segments of the Liquid Sugar Industry?

The market segments include Origin, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Organic Variants; Thriving Food and Beverage Industry.

6. What are the notable trends driving market growth?

Escalating Demand for Organic Variants.

7. Are there any restraints impacting market growth?

Sugar Under Scrutiny with New Taxes and Label Regulations.

8. Can you provide examples of recent developments in the market?

January 2024: North Carolina-based Elo Life Systems closed a USD 20.5 million Series A2 round to accelerate the development of a natural high-intensity sweetener and Cavendish bananas engineered to resist the devastating Fusarium wilt fungal disease (TR4). The company aims to introduce a liquid sweetener from watermelon juice by 2026 and powdered sweeteners from sugar beets by 2027.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Sugar Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Sugar Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Sugar Industry?

To stay informed about further developments, trends, and reports in the Liquid Sugar Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence