Key Insights

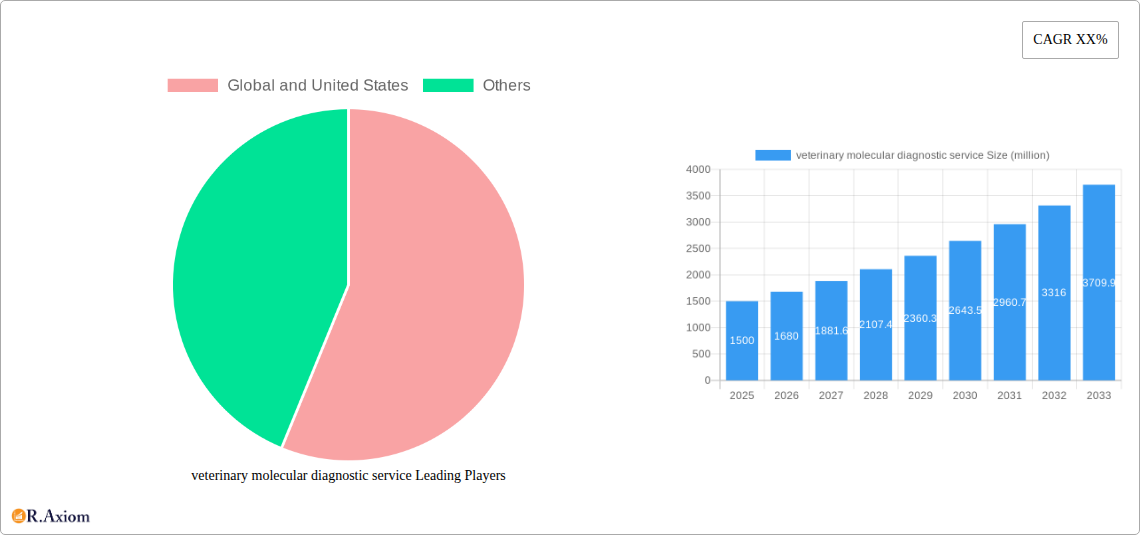

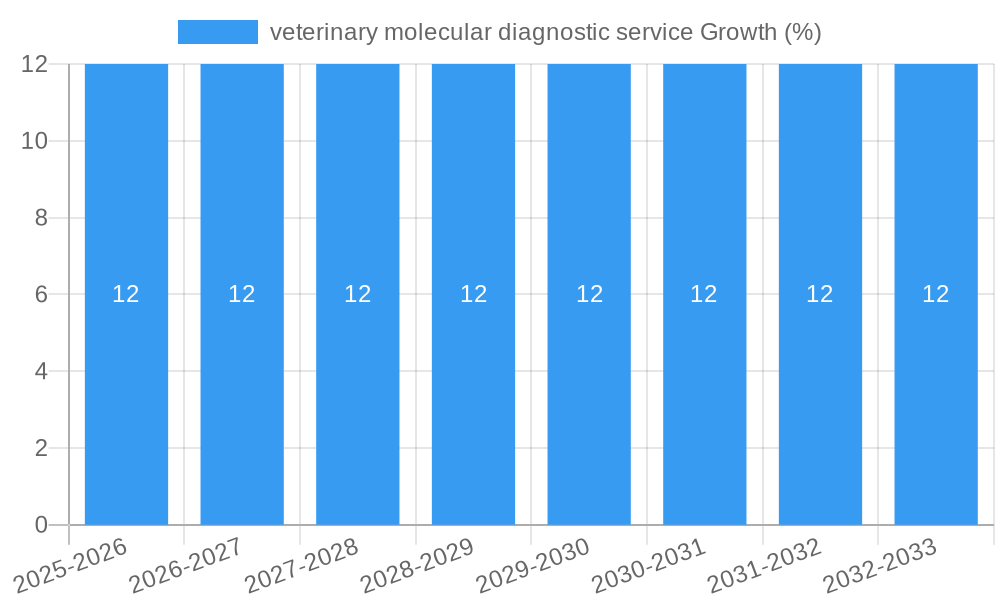

The global veterinary molecular diagnostic service market is experiencing robust expansion, driven by a confluence of factors that underscore the increasing importance of advanced diagnostics in animal healthcare. The market, estimated to be worth approximately USD 1,500 million in 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of around 12% through 2033. This significant surge is propelled by the rising prevalence of infectious diseases in companion and livestock animals, alongside an increasing awareness among pet owners and livestock producers regarding the benefits of early and accurate disease detection. Furthermore, the growing trend of pet humanization, leading to higher spending on advanced veterinary care, and the continuous development of novel molecular diagnostic technologies, such as PCR and next-generation sequencing, are key enablers. The demand for rapid, specific, and sensitive diagnostic tools to manage complex conditions like metabolic disorders and genetic abnormalities is also contributing to market growth.

The market is segmented into various applications, with infectious diseases being a dominant segment due to their widespread impact and the critical need for swift identification and treatment. Metabolic diseases and genetics also represent growing application areas as veterinary medicine increasingly adopts a personalized approach. The market is further categorized by product type, where kits and reagents currently hold a significant share, facilitated by their accessibility and ease of use in veterinary clinics. However, the instrument segment is expected to witness substantial growth, driven by the adoption of sophisticated diagnostic platforms. Geographically, North America, particularly the United States, is a leading market, owing to its advanced veterinary infrastructure, high pet ownership rates, and substantial investment in animal health research and development. Asia Pacific is anticipated to be the fastest-growing region, fueled by increasing disposable incomes, a burgeoning pet population, and growing awareness of animal diseases. Restraints such as the high cost of advanced diagnostic equipment and the need for skilled personnel to operate them are being addressed through technological advancements and increasing affordability.

This comprehensive report provides an in-depth analysis of the global veterinary molecular diagnostic service market, offering critical insights for industry stakeholders. Covering the historical period from 2019 to 2024, the base year of 2025, and a forecast period extending to 2033, this study delivers actionable intelligence on market dynamics, segmentation, competitive landscape, and future growth prospects. With a focus on high-traffic keywords such as "veterinary diagnostics," "molecular testing," "animal health," and "pet diagnostics," this report is optimized for maximum search visibility and engagement.

veterinary molecular diagnostic service Market Concentration & Innovation

The global veterinary molecular diagnostic service market exhibits moderate concentration, with a few leading players dominating a significant share of the veterinary diagnostics market. Innovation is a primary driver, fueled by advancements in DNA sequencing, PCR technology, and bioinformatics. Regulatory frameworks, particularly in developed regions like the United States and Europe, play a crucial role in shaping market access and product development, ensuring the safety and efficacy of veterinary molecular testing solutions. Product substitutes, while present in traditional diagnostic methods, are increasingly being supplanted by the accuracy and speed offered by molecular diagnostics. End-user trends are leaning towards increased pet ownership, growing awareness of animal welfare, and a demand for personalized medicine for companion animals, driving adoption of advanced animal health diagnostics. Mergers and acquisitions (M&A) are a recurring theme, with several significant deals valuing over $100 million each in the past five years, indicating consolidation and strategic expansion. For instance, acquisitions aimed at broadening assay portfolios or expanding geographical reach are prevalent.

- Market Share Concentration: Top 5 players estimated to hold 65% of the global market.

- M&A Deal Values: Average deal value in the last two years estimated at $150 million.

- Innovation Drivers: Next-generation sequencing (NGS) cost reduction, AI integration in data analysis, and point-of-care testing development.

veterinary molecular diagnostic service Industry Trends & Insights

The veterinary molecular diagnostic service market is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033. This expansion is primarily driven by the increasing recognition of molecular diagnostics for its unparalleled accuracy in identifying infectious diseases, genetic predispositions, and metabolic disorders in animals. The rising global pet population, coupled with enhanced owner willingness to invest in premium veterinary care, significantly contributes to market penetration. Technological advancements, including the development of more sensitive and rapid assay kits, miniaturized instruments, and user-friendly software solutions, are further accelerating market adoption. The integration of artificial intelligence (AI) and machine learning (ML) in data interpretation and disease prediction is another transformative trend, offering veterinarians deeper insights and enabling proactive treatment strategies. Furthermore, the growing demand for comprehensive genetic testing for breed identification, disease screening, and personalized treatment plans for both companion animals and livestock is creating substantial market opportunities. The shift towards herd health management in agricultural settings, emphasizing early disease detection and prevention through molecular surveillance, also underpins the market's upward trajectory. Increased collaboration between diagnostic companies and veterinary practitioners to develop tailored solutions and educational initiatives further fuels market momentum. The market penetration for infectious disease diagnostics is estimated to be around 40% in developed nations, with significant room for growth in emerging economies.

Dominant Markets & Segments in veterinary molecular diagnostic service

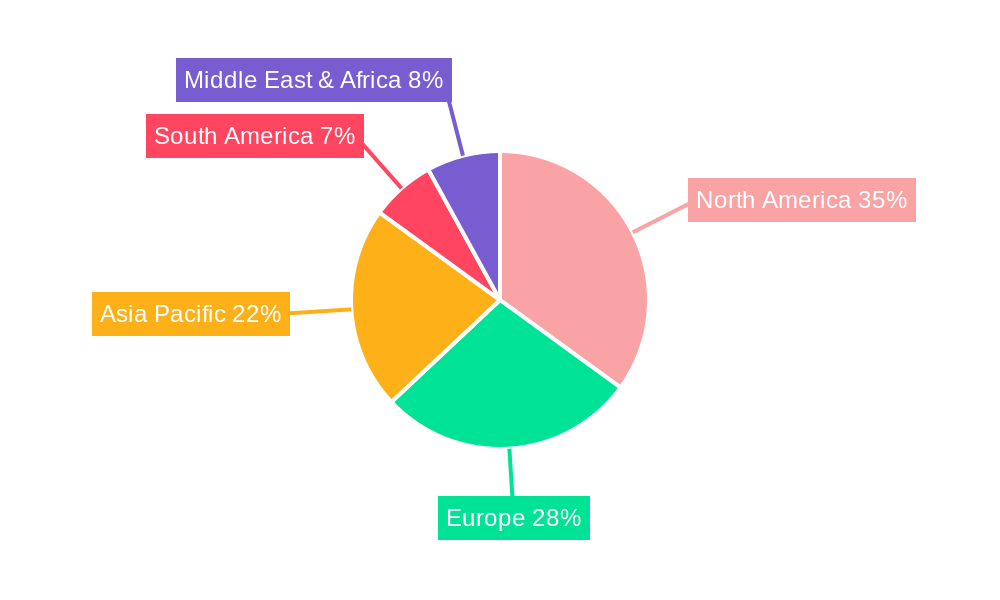

The North American region, particularly the United States, stands out as the dominant market for veterinary molecular diagnostic services, accounting for an estimated 35% of the global market share in 2025. This dominance is propelled by a confluence of factors including high pet ownership rates, a strong emphasis on advanced animal healthcare, significant research and development investments, and favorable reimbursement policies for veterinary services.

Application Segment Dominance:

- Infectious Diseases: This segment is currently the largest and is expected to maintain its leadership throughout the forecast period.

- Key Drivers: The recurring outbreaks of zoonotic and non-zoonotic infectious diseases in both companion animals and livestock necessitate rapid and accurate diagnostic tools. The increasing prevalence of antimicrobial resistance also drives the need for precise pathogen identification to guide targeted therapy.

- Market Size: Estimated to reach $2,500 million by 2025.

- Genetics: This segment is experiencing the fastest growth due to the rising demand for genetic testing for inherited diseases, breed identification, and personalized medicine.

- Key Drivers: Advancements in gene sequencing technologies and the growing understanding of the genetic basis of animal diseases are key catalysts. Pet owners are increasingly interested in understanding their pets' genetic predispositions to certain health conditions.

- Market Size: Projected to grow at a CAGR of 14%.

- Metabolic Diseases: While a smaller segment compared to infectious diseases, its growth is steady, driven by the increasing incidence of conditions like diabetes and thyroid disorders in aging animal populations.

- Key Drivers: Improved diagnostic sensitivity and the development of specialized molecular assays for metabolic markers are contributing to its expansion.

- Others: This segment encompasses a range of applications including oncology diagnostics, toxicology, and microbiome analysis, which are gradually gaining traction.

Type Segment Dominance:

- Kits and Reagents: This is the largest and most crucial segment, forming the backbone of molecular diagnostic workflows.

- Key Drivers: The availability of a wide range of ready-to-use kits for various pathogens and genetic markers, coupled with their cost-effectiveness and ease of use in veterinary clinics, fuels demand. The development of multiplex assays further enhances their appeal.

- Market Size: Estimated to be $3,000 million by 2025.

- Instrument: This segment includes PCR machines, sequencers, and other analytical devices.

- Key Drivers: The increasing adoption of in-house diagnostic capabilities by veterinary practices and the development of more compact and affordable instruments are driving growth.

- Market Size: Expected to grow at a CAGR of 11%.

- Software: This segment is gaining prominence with the increasing need for data management, analysis, and interpretation of molecular diagnostic results.

- Key Drivers: AI-powered diagnostic software that aids in disease prediction and treatment recommendations is a significant growth catalyst.

- Market Size: Estimated to reach $500 million by 2025.

veterinary molecular diagnostic service Product Developments

Recent product developments in veterinary molecular diagnostics are characterized by a strong focus on speed, accuracy, and ease of use. Innovations in real-time PCR (qPCR) technology have led to faster turnaround times for infectious disease detection, while advancements in next-generation sequencing (NGS) are enabling comprehensive genomic analysis for both companion animals and livestock. The development of multiplex assays, capable of detecting multiple pathogens or genetic markers simultaneously, offers significant cost and time efficiencies. Furthermore, the emergence of portable and point-of-care diagnostic devices is democratizing access to advanced molecular testing, allowing veterinarians to perform sophisticated diagnostics directly in their clinics. These developments collectively enhance diagnostic capabilities, improve patient outcomes, and strengthen the competitive advantage of companies offering these cutting-edge solutions.

Report Scope & Segmentation Analysis

This report encompasses a thorough analysis of the veterinary molecular diagnostic service market segmented by Application and Type.

Application Segments:

- Infectious Diseases: This segment covers the detection of viral, bacterial, parasitic, and fungal infections affecting animals. Growth is driven by the need for rapid outbreak detection and accurate pathogen identification. Market size estimated at $2,500 million by 2025.

- Metabolic Diseases: This segment focuses on the molecular diagnosis of metabolic disorders such as diabetes, endocrine dysfunctions, and nutritional deficiencies. Market size projected at $800 million by 2025.

- Genetics: This segment includes genetic testing for inherited disorders, breed identification, and pharmacogenomics. This segment is experiencing significant growth due to increasing owner interest. Market size estimated at $1,200 million by 2025.

- Others: This broad category includes diagnostics for oncology, toxicology, microbiome analysis, and allergy testing. Market size estimated at $300 million by 2025.

Type Segments:

- Kits and Reagents: This segment, representing consumable products for molecular testing, is the largest. Market size estimated at $3,000 million by 2025.

- Instrument: This segment includes diagnostic equipment such as PCR machines, sequencers, and automated platforms. Market size estimated at $1,500 million by 2025.

- Software: This segment comprises diagnostic software for data analysis, interpretation, and management. Market size estimated at $500 million by 2025.

- Others: This includes services related to molecular diagnostics and lab equipment accessories. Market size estimated at $100 million by 2025.

Key Drivers of veterinary molecular diagnostic service Growth

Several key factors are propelling the growth of the veterinary molecular diagnostic service market. The increasing humanization of pets has led to a surge in demand for advanced healthcare, mirroring human medical standards. Rising disposable incomes, particularly in emerging economies, enable pet owners to invest more in their animals' well-being, including sophisticated diagnostic procedures. Technological advancements, such as the miniaturization of equipment and the development of more sensitive and specific assays, are making molecular diagnostics more accessible and affordable. Furthermore, the growing awareness among veterinarians and pet owners about the benefits of early disease detection and personalized treatment plans is a significant catalyst. The expanding livestock industry's focus on herd health and biosecurity also drives the adoption of molecular diagnostics for disease surveillance and control.

- Increasing Pet Ownership & Humanization: A primary driver for enhanced veterinary care spending.

- Technological Advancements: Lower cost of sequencing, improved assay sensitivity, and portable devices.

- Growing Awareness of Preventive Healthcare: Emphasis on early detection and genetic screening.

- Food Safety & Biosecurity Concerns: Critical for the livestock sector.

Challenges in the veterinary molecular diagnostic service Sector

Despite its promising growth, the veterinary molecular diagnostic service sector faces several challenges. High initial investment costs for advanced instrumentation can be a barrier for smaller veterinary practices. The lack of standardized regulatory frameworks in some regions can lead to inconsistencies in product approval and market access. A shortage of trained veterinary professionals with expertise in molecular diagnostics can hinder adoption and proper utilization of these services. Furthermore, the perceived cost of molecular diagnostics compared to traditional methods can be a deterrent for some pet owners. Supply chain disruptions for reagents and consumables can also impact the consistent availability of diagnostic services.

- High Upfront Investment: Cost of equipment and infrastructure.

- Regulatory Variability: Inconsistent approval processes across different countries.

- Skilled Workforce Shortage: Lack of trained molecular diagnosticians.

- Cost Perception: Molecular diagnostics viewed as more expensive than traditional methods.

Emerging Opportunities in veterinary molecular diagnostic service

The veterinary molecular diagnostic service market presents numerous emerging opportunities. The growing field of companion animal oncology is witnessing increased demand for molecular profiling to guide targeted therapies and improve treatment outcomes. The development of non-invasive diagnostic methods, such as saliva or urine-based tests, offers significant potential for enhanced client convenience and patient compliance. The integration of AI and machine learning in diagnostic platforms to predict disease outbreaks and personalize treatment plans is another rapidly expanding area. Furthermore, the burgeoning companion animal microbiome analysis market offers insights into gut health, immunity, and overall well-being, opening new avenues for diagnostic services. Expansion into underserved emerging markets with increasing pet ownership and veterinary infrastructure also represents a significant growth opportunity.

Leading Players in the veterinary molecular diagnostic service Market

- IDEXX Laboratories

- Abbott Laboratories

- Zoetis Inc.

- Heska Corporation

- Thermo Fisher Scientific

- Agilent Technologies

- Bio-Rad Laboratories

- QIAGEN

- Antech Diagnostics

- Neogen Corporation

Key Developments in veterinary molecular diagnostic service Industry

- 2023/08: IDEXX Laboratories launched a new suite of PCR-based diagnostic assays for companion animals, enhancing rapid detection of infectious diseases.

- 2023/05: Zoetis Inc. acquired a leading provider of companion animal diagnostics, expanding its portfolio in molecular testing for genetic diseases.

- 2022/11: Heska Corporation introduced an advanced instrument for in-clinic molecular diagnostics, offering faster turnaround times and improved accuracy.

- 2022/09: A significant increase in M&A activities was observed, with several smaller players being acquired to consolidate market share and technological capabilities.

- 2021/12: Thermo Fisher Scientific expanded its animal health offerings with new reagents for genetic analysis in livestock.

- 2021/07: The development of AI-powered diagnostic software aimed at predicting disease progression in pets gained traction.

Strategic Outlook for veterinary molecular diagnostic service Market

- 2023/08: IDEXX Laboratories launched a new suite of PCR-based diagnostic assays for companion animals, enhancing rapid detection of infectious diseases.

- 2023/05: Zoetis Inc. acquired a leading provider of companion animal diagnostics, expanding its portfolio in molecular testing for genetic diseases.

- 2022/11: Heska Corporation introduced an advanced instrument for in-clinic molecular diagnostics, offering faster turnaround times and improved accuracy.

- 2022/09: A significant increase in M&A activities was observed, with several smaller players being acquired to consolidate market share and technological capabilities.

- 2021/12: Thermo Fisher Scientific expanded its animal health offerings with new reagents for genetic analysis in livestock.

- 2021/07: The development of AI-powered diagnostic software aimed at predicting disease progression in pets gained traction.

Strategic Outlook for veterinary molecular diagnostic service Market

The strategic outlook for the veterinary molecular diagnostic service market remains highly optimistic. Key growth catalysts include the continued rise in pet humanization, driving demand for advanced healthcare solutions. Investments in research and development for novel diagnostic technologies, such as liquid biopsies and CRISPR-based diagnostics, are expected to redefine the diagnostic landscape. Strategic collaborations between technology providers, veterinary clinics, and research institutions will foster innovation and broaden market reach. Furthermore, the increasing focus on precision medicine and personalized treatment plans for animals will fuel the demand for comprehensive genetic and molecular profiling. Expansion into emerging markets, coupled with a growing emphasis on zoonotic disease surveillance and food safety, will further solidify the market's upward trajectory, creating substantial opportunities for stakeholders.

veterinary molecular diagnostic service Segmentation

-

1. Application

- 1.1. Infectious Diseases

- 1.2. Metabolic Diseases

- 1.3. Genetics

- 1.4. Others

-

2. Types

- 2.1. Kits and Reagents

- 2.2. Instrument

- 2.3. Software

- 2.4. Others

veterinary molecular diagnostic service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

veterinary molecular diagnostic service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global veterinary molecular diagnostic service Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Infectious Diseases

- 5.1.2. Metabolic Diseases

- 5.1.3. Genetics

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Kits and Reagents

- 5.2.2. Instrument

- 5.2.3. Software

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America veterinary molecular diagnostic service Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Infectious Diseases

- 6.1.2. Metabolic Diseases

- 6.1.3. Genetics

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Kits and Reagents

- 6.2.2. Instrument

- 6.2.3. Software

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America veterinary molecular diagnostic service Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Infectious Diseases

- 7.1.2. Metabolic Diseases

- 7.1.3. Genetics

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Kits and Reagents

- 7.2.2. Instrument

- 7.2.3. Software

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe veterinary molecular diagnostic service Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Infectious Diseases

- 8.1.2. Metabolic Diseases

- 8.1.3. Genetics

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Kits and Reagents

- 8.2.2. Instrument

- 8.2.3. Software

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa veterinary molecular diagnostic service Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Infectious Diseases

- 9.1.2. Metabolic Diseases

- 9.1.3. Genetics

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Kits and Reagents

- 9.2.2. Instrument

- 9.2.3. Software

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific veterinary molecular diagnostic service Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Infectious Diseases

- 10.1.2. Metabolic Diseases

- 10.1.3. Genetics

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Kits and Reagents

- 10.2.2. Instrument

- 10.2.3. Software

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1. Global and United States

List of Figures

- Figure 1: Global veterinary molecular diagnostic service Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America veterinary molecular diagnostic service Revenue (million), by Application 2024 & 2032

- Figure 3: North America veterinary molecular diagnostic service Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America veterinary molecular diagnostic service Revenue (million), by Types 2024 & 2032

- Figure 5: North America veterinary molecular diagnostic service Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America veterinary molecular diagnostic service Revenue (million), by Country 2024 & 2032

- Figure 7: North America veterinary molecular diagnostic service Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America veterinary molecular diagnostic service Revenue (million), by Application 2024 & 2032

- Figure 9: South America veterinary molecular diagnostic service Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America veterinary molecular diagnostic service Revenue (million), by Types 2024 & 2032

- Figure 11: South America veterinary molecular diagnostic service Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America veterinary molecular diagnostic service Revenue (million), by Country 2024 & 2032

- Figure 13: South America veterinary molecular diagnostic service Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe veterinary molecular diagnostic service Revenue (million), by Application 2024 & 2032

- Figure 15: Europe veterinary molecular diagnostic service Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe veterinary molecular diagnostic service Revenue (million), by Types 2024 & 2032

- Figure 17: Europe veterinary molecular diagnostic service Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe veterinary molecular diagnostic service Revenue (million), by Country 2024 & 2032

- Figure 19: Europe veterinary molecular diagnostic service Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa veterinary molecular diagnostic service Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa veterinary molecular diagnostic service Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa veterinary molecular diagnostic service Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa veterinary molecular diagnostic service Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa veterinary molecular diagnostic service Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa veterinary molecular diagnostic service Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific veterinary molecular diagnostic service Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific veterinary molecular diagnostic service Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific veterinary molecular diagnostic service Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific veterinary molecular diagnostic service Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific veterinary molecular diagnostic service Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific veterinary molecular diagnostic service Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global veterinary molecular diagnostic service Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global veterinary molecular diagnostic service Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global veterinary molecular diagnostic service Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global veterinary molecular diagnostic service Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global veterinary molecular diagnostic service Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global veterinary molecular diagnostic service Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global veterinary molecular diagnostic service Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global veterinary molecular diagnostic service Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global veterinary molecular diagnostic service Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global veterinary molecular diagnostic service Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global veterinary molecular diagnostic service Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global veterinary molecular diagnostic service Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global veterinary molecular diagnostic service Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global veterinary molecular diagnostic service Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global veterinary molecular diagnostic service Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global veterinary molecular diagnostic service Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global veterinary molecular diagnostic service Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global veterinary molecular diagnostic service Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global veterinary molecular diagnostic service Revenue million Forecast, by Country 2019 & 2032

- Table 41: China veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific veterinary molecular diagnostic service Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the veterinary molecular diagnostic service?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the veterinary molecular diagnostic service?

Key companies in the market include Global and United States.

3. What are the main segments of the veterinary molecular diagnostic service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "veterinary molecular diagnostic service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the veterinary molecular diagnostic service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the veterinary molecular diagnostic service?

To stay informed about further developments, trends, and reports in the veterinary molecular diagnostic service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence