Key Insights

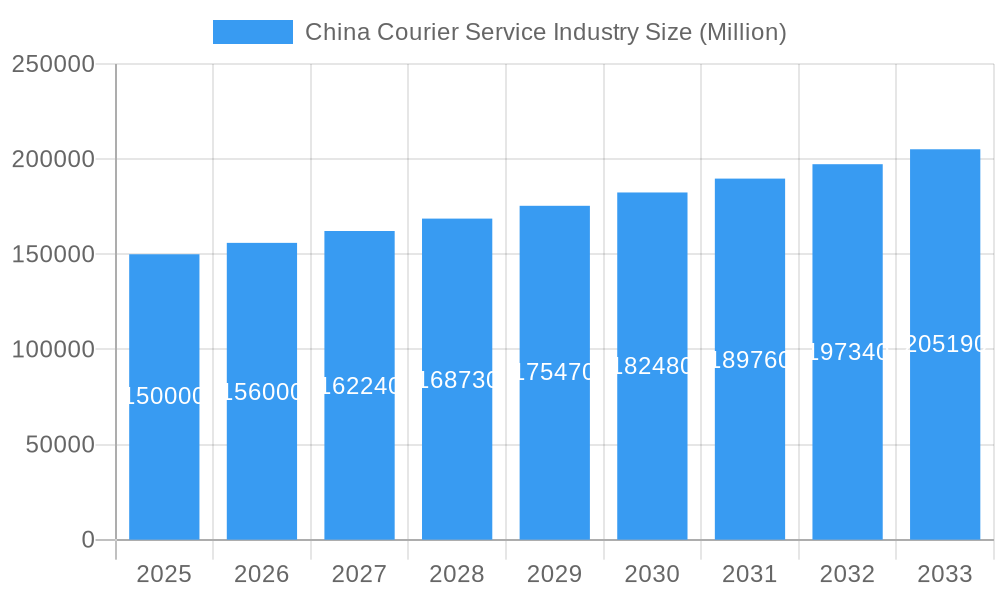

The China courier service industry is experiencing substantial growth, driven by the e-commerce boom and escalating consumer demand for expedited delivery. With a projected market size of 131.84 billion in 2025 and a CAGR of 7.21%, the sector is set for significant expansion through 2033. Key growth catalysts include the widespread adoption of online shopping, especially in lower-tier cities, and advancements in logistics infrastructure, such as enhanced sorting and delivery networks. The increasing preference for express delivery services and a rise in B2C transactions further fuel market expansion. E-commerce-related deliveries and express services are anticipated to dominate growth segments.

China Courier Service Industry Market Size (In Billion)

The industry faces intense competition from both domestic and international players. Maintaining consistent service quality and operational efficiency during rapid expansion are critical for success. Adapting to evolving consumer expectations and technological innovations, including AI-driven route optimization and automated sorting, is paramount. Future growth will depend on the industry's capacity for innovation and adaptation, particularly in sustainable delivery practices and managing increasing shipment volumes. B2C delivery and express services are expected to lead growth, aligning with global courier industry trends.

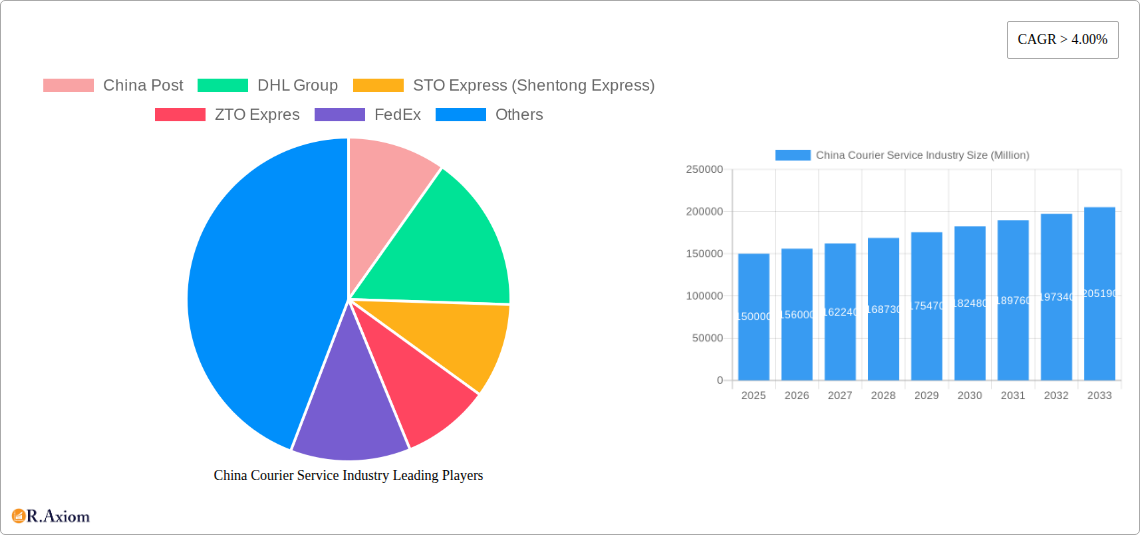

China Courier Service Industry Company Market Share

China Courier Service Industry Market Analysis: 2019-2033

This report offers an in-depth analysis of the China courier service industry, covering market size, segmentation, competitive dynamics, and future outlook. The analysis spans 2019-2033, with 2025 as the base year. Insights provided are valuable for industry stakeholders, investors, and businesses entering or operating within this dynamic market. The market, valued at 131.84 billion in 2025, is projected to reach significant future valuations by 2033.

China Courier Service Industry Market Concentration & Innovation

This section analyzes the level of market concentration within the China courier service industry, identifying key players and assessing their market share. We examine the drivers of innovation, including technological advancements, regulatory changes, and evolving consumer preferences. The impact of mergers and acquisitions (M&A) activity on market dynamics is also explored, along with an analysis of substitute products and services.

Market Concentration: The Chinese courier market exhibits a moderately concentrated structure, with a few dominant players holding significant market share. SF Express (KEX-SF), STO Express, Yunda Express, and ZTO Express constitute a significant portion of the market. However, the market also accommodates numerous smaller players, creating a diverse competitive landscape. We estimate that the top 5 players control approximately xx% of the market in 2025.

Innovation Drivers: Technological advancements, such as AI-powered sorting systems, drone delivery, and improved tracking technologies, are key innovation drivers. Government regulations promoting e-commerce growth and efficient logistics also play a crucial role.

Regulatory Framework: The Chinese government's policies concerning logistics and e-commerce heavily influence the industry. These regulations impact pricing, operational efficiency, and environmental sustainability. Changes in these policies can significantly alter market dynamics.

Product Substitutes: The emergence of alternative delivery models such as same-day delivery services and crowdsourced delivery platforms presents both challenges and opportunities for established players.

M&A Activity: The industry has witnessed significant M&A activity in recent years, with larger companies acquiring smaller players to expand their market reach and service capabilities. The total value of M&A deals in the period 2019-2024 is estimated at xx Million.

End-User Trends: The growing preference for faster delivery options and increased online shopping habits significantly influence industry growth.

China Courier Service Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the Chinese courier service industry. We analyze market growth drivers, technological disruptions, evolving consumer preferences, and the competitive landscape, focusing on both historical performance and future projections. The Compound Annual Growth Rate (CAGR) and market penetration rates are key metrics used to analyze market trends.

The industry is characterized by a high growth trajectory driven by e-commerce expansion, urbanization, and rising disposable incomes. Technological advancements, such as automation and AI, enhance efficiency and speed, creating a competitive advantage. Consumer preference for faster and more reliable delivery continues to drive demand for express courier services. The market exhibits intense competition, with players constantly innovating to improve service quality and expand their market share. The CAGR for the industry during the forecast period (2025-2033) is projected to be xx%. Market penetration in key areas such as rural areas remains a significant growth opportunity. The shift towards sustainable practices, driven by environmental concerns, presents another key trend influencing the industry.

Dominant Markets & Segments in China Courier Service Industry

This section identifies the dominant segments within the China courier service industry, based on destination, speed of delivery, business model, shipment weight, mode of transport, and end-user industry. Key drivers for each segment's dominance are analyzed.

Leading Segments:

Destination: Domestic courier services represent a significantly larger market share compared to international services due to the vast domestic e-commerce market.

Speed of Delivery: Express delivery services dominate due to consumer preference for speed and convenience.

Business Model: B2C (Business-to-Consumer) dominates, fueled by e-commerce growth.

Shipment Weight: Medium weight shipments represent the largest share, reflecting the typical size of online purchases.

Mode of Transport: Road transport constitutes the majority due to its extensive infrastructure and cost-effectiveness.

End-User Industry: E-commerce is the dominant end-user industry, driving the majority of courier service demand.

Key Drivers of Dominance:

Economic Policies: Government initiatives supporting e-commerce and logistics development have fueled growth in the domestic B2C segment.

Infrastructure Development: Extensive road networks support road transport's dominance.

Consumer Preferences: Demand for fast and reliable delivery drives the growth of express services and B2C model.

China Courier Service Industry Product Developments

The China courier service industry is witnessing significant product innovations, driven primarily by technological advancements. AI-powered sorting systems, automated warehouses, and real-time tracking capabilities are enhancing efficiency and customer experience. Drone deliveries and autonomous vehicles are emerging as potential solutions for last-mile delivery, addressing challenges in urban areas. These innovations provide significant competitive advantages, allowing companies to offer faster, more reliable, and cost-effective services.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the China courier service industry, segmented by destination (domestic and international), speed of delivery (express and non-express), business model (B2B, B2C, and C2C), shipment weight (light, medium, and heavy), mode of transport (air, road, and others), and end-user industry (e-commerce, BFSI, healthcare, manufacturing, primary industry, wholesale and retail trade, and others). Each segment's market size, growth projections, and competitive dynamics are thoroughly analyzed. The report's scope includes detailed market sizing, forecasts, competitor analysis, and an assessment of industry trends.

Key Drivers of China Courier Service Industry Growth

The growth of the China courier service industry is fueled by several key factors. The explosive growth of e-commerce is the primary driver, generating massive demand for delivery services. Government initiatives promoting digitalization and improved logistics infrastructure also contribute significantly. Technological advancements, particularly in automation and data analytics, are enhancing efficiency and reducing costs. Rising disposable incomes and urbanization are increasing consumer demand for convenient and efficient delivery options.

Challenges in the China Courier Service Industry Sector

The China courier service industry faces several challenges. Intense competition among numerous players leads to price pressures and reduced profit margins. Maintaining operational efficiency and managing fluctuating demand are ongoing challenges. Infrastructure limitations, particularly in rural areas, hinder efficient delivery. Stringent regulatory requirements add to operational complexities. Rising labor costs and fuel prices also impact profitability. The industry faces environmental concerns related to carbon emissions from transportation.

Emerging Opportunities in China Courier Service Industry

The China courier service industry presents numerous opportunities. Expansion into underserved rural markets holds significant potential. Technological advancements, such as drone delivery and autonomous vehicles, offer avenues for improving efficiency and reducing costs. Growth in cross-border e-commerce creates opportunities for international courier services. The increasing demand for specialized services, such as cold chain logistics for pharmaceuticals and time-sensitive deliveries, presents further opportunities. Sustainable and eco-friendly delivery solutions are gaining traction, presenting a significant opportunity for environmentally conscious businesses.

Leading Players in the China Courier Service Industry Market

- China Post

- DHL Group

- STO Express (Shentong Express)

- ZTO Express

- FedEx

- United Parcel Service of America Inc (UPS)

- Hongkong Post

- Yunda Express

- YTO Express

- La Poste Group

- SF Express (KEX-SF)

Key Developments in China Courier Service Industry Industry

June 2023: China Post launched its first integrated indoor and outdoor “Robot Plus” AI delivery solution. This represents a significant step towards automation and efficiency in last-mile delivery.

April 2023: China Post and Ping An Bank launched an intelligent archives service center, integrating auto finance and logistics services. This signifies a move towards integrated financial and logistics solutions.

March 2023: UPS partnered with Google Cloud to improve package tracking using RFID technology. This collaboration highlights the growing importance of data and technology in logistics.

Strategic Outlook for China Courier Service Industry Market

The China courier service industry is poised for continued growth, driven by e-commerce expansion, technological advancements, and supportive government policies. Opportunities exist in expanding into new markets, adopting innovative technologies, and providing specialized services. Players that can adapt to evolving consumer preferences, enhance operational efficiency, and embrace sustainable practices will be well-positioned for success. The market's future hinges on the ability of companies to navigate competitive pressures and leverage technological advancements to deliver superior customer experiences.

China Courier Service Industry Segmentation

-

1. Destination

- 1.1. Domestic

- 1.2. International

-

2. Speed Of Delivery

- 2.1. Express

- 2.2. Non-Express

-

3. Model

- 3.1. Business-to-Business (B2B)

- 3.2. Business-to-Consumer (B2C)

- 3.3. Consumer-to-Consumer (C2C)

-

4. Shipment Weight

- 4.1. Heavy Weight Shipments

- 4.2. Light Weight Shipments

- 4.3. Medium Weight Shipments

-

5. Mode Of Transport

- 5.1. Air

- 5.2. Road

- 5.3. Others

-

6. End User Industry

- 6.1. E-Commerce

- 6.2. Financial Services (BFSI)

- 6.3. Healthcare

- 6.4. Manufacturing

- 6.5. Primary Industry

- 6.6. Wholesale and Retail Trade (Offline)

- 6.7. Others

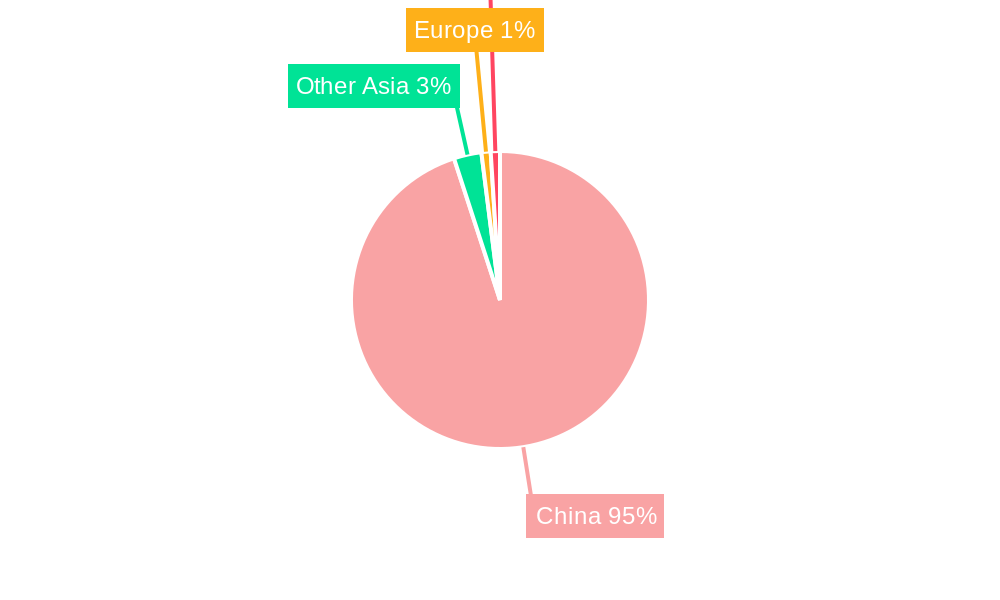

China Courier Service Industry Segmentation By Geography

- 1. China

China Courier Service Industry Regional Market Share

Geographic Coverage of China Courier Service Industry

China Courier Service Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Destination

- 5.1.1. Domestic

- 5.1.2. International

- 5.2. Market Analysis, Insights and Forecast - by Speed Of Delivery

- 5.2.1. Express

- 5.2.2. Non-Express

- 5.3. Market Analysis, Insights and Forecast - by Model

- 5.3.1. Business-to-Business (B2B)

- 5.3.2. Business-to-Consumer (B2C)

- 5.3.3. Consumer-to-Consumer (C2C)

- 5.4. Market Analysis, Insights and Forecast - by Shipment Weight

- 5.4.1. Heavy Weight Shipments

- 5.4.2. Light Weight Shipments

- 5.4.3. Medium Weight Shipments

- 5.5. Market Analysis, Insights and Forecast - by Mode Of Transport

- 5.5.1. Air

- 5.5.2. Road

- 5.5.3. Others

- 5.6. Market Analysis, Insights and Forecast - by End User Industry

- 5.6.1. E-Commerce

- 5.6.2. Financial Services (BFSI)

- 5.6.3. Healthcare

- 5.6.4. Manufacturing

- 5.6.5. Primary Industry

- 5.6.6. Wholesale and Retail Trade (Offline)

- 5.6.7. Others

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. China

- 5.1. Market Analysis, Insights and Forecast - by Destination

- 6. China Courier Service Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Destination

- 6.1.1. Domestic

- 6.1.2. International

- 6.2. Market Analysis, Insights and Forecast - by Speed Of Delivery

- 6.2.1. Express

- 6.2.2. Non-Express

- 6.3. Market Analysis, Insights and Forecast - by Model

- 6.3.1. Business-to-Business (B2B)

- 6.3.2. Business-to-Consumer (B2C)

- 6.3.3. Consumer-to-Consumer (C2C)

- 6.4. Market Analysis, Insights and Forecast - by Shipment Weight

- 6.4.1. Heavy Weight Shipments

- 6.4.2. Light Weight Shipments

- 6.4.3. Medium Weight Shipments

- 6.5. Market Analysis, Insights and Forecast - by Mode Of Transport

- 6.5.1. Air

- 6.5.2. Road

- 6.5.3. Others

- 6.6. Market Analysis, Insights and Forecast - by End User Industry

- 6.6.1. E-Commerce

- 6.6.2. Financial Services (BFSI)

- 6.6.3. Healthcare

- 6.6.4. Manufacturing

- 6.6.5. Primary Industry

- 6.6.6. Wholesale and Retail Trade (Offline)

- 6.6.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Destination

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Post

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 DHL Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 STO Express (Shentong Express)

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ZTO Expres

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FedEx

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 United Parcel Service of America Inc (UPS)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hongkong Post

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yunda Express

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 YTO Express

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 La Poste Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 SF Express (KEX-SF)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 China Post

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Courier Service Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Courier Service Industry Share (%) by Company 2025

List of Tables

- Table 1: China Courier Service Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 2: China Courier Service Industry Revenue billion Forecast, by Speed Of Delivery 2020 & 2033

- Table 3: China Courier Service Industry Revenue billion Forecast, by Model 2020 & 2033

- Table 4: China Courier Service Industry Revenue billion Forecast, by Shipment Weight 2020 & 2033

- Table 5: China Courier Service Industry Revenue billion Forecast, by Mode Of Transport 2020 & 2033

- Table 6: China Courier Service Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 7: China Courier Service Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: China Courier Service Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 9: China Courier Service Industry Revenue billion Forecast, by Speed Of Delivery 2020 & 2033

- Table 10: China Courier Service Industry Revenue billion Forecast, by Model 2020 & 2033

- Table 11: China Courier Service Industry Revenue billion Forecast, by Shipment Weight 2020 & 2033

- Table 12: China Courier Service Industry Revenue billion Forecast, by Mode Of Transport 2020 & 2033

- Table 13: China Courier Service Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 14: China Courier Service Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Courier Service Industry?

The projected CAGR is approximately 7.21%.

2. Which companies are prominent players in the China Courier Service Industry?

Key companies in the market include China Post, DHL Group, STO Express (Shentong Express), ZTO Expres, FedEx, United Parcel Service of America Inc (UPS), Hongkong Post, Yunda Express, YTO Express, La Poste Group, SF Express (KEX-SF).

3. What are the main segments of the China Courier Service Industry?

The market segments include Destination, Speed Of Delivery, Model, Shipment Weight, Mode Of Transport, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 131.84 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing production of chemical and allied products driving the market4.; Rising demand for green warehouses.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

4.; Stringent Rules and Regulations4.; Higher Costs.

8. Can you provide examples of recent developments in the market?

June 2023: China Post launched its first integrated indoor and outdoor “Robot Plus” AI delivery solution in China. The intelligent delivery solution relies on a combination of unmanned vehicles outdoors and robots indoors, constructing an integrated indoor and outdoor unmanned distribution mode and developing a last-mile logistics network with AI transport capacity sharing.April 2023: China Post and the Automobile Consumption Financial Center of Ping An Bank Co. Ltd launched an intelligent archives service center in Guangdong to promote the service integration of auto finance and express and logistics businesses.March 2023: UPS entered a partnership with Google Cloud, where Google will help UPS by putting radio-frequency identification chips on packages to track them efficiently.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Courier Service Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Courier Service Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Courier Service Industry?

To stay informed about further developments, trends, and reports in the China Courier Service Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence