Key Insights

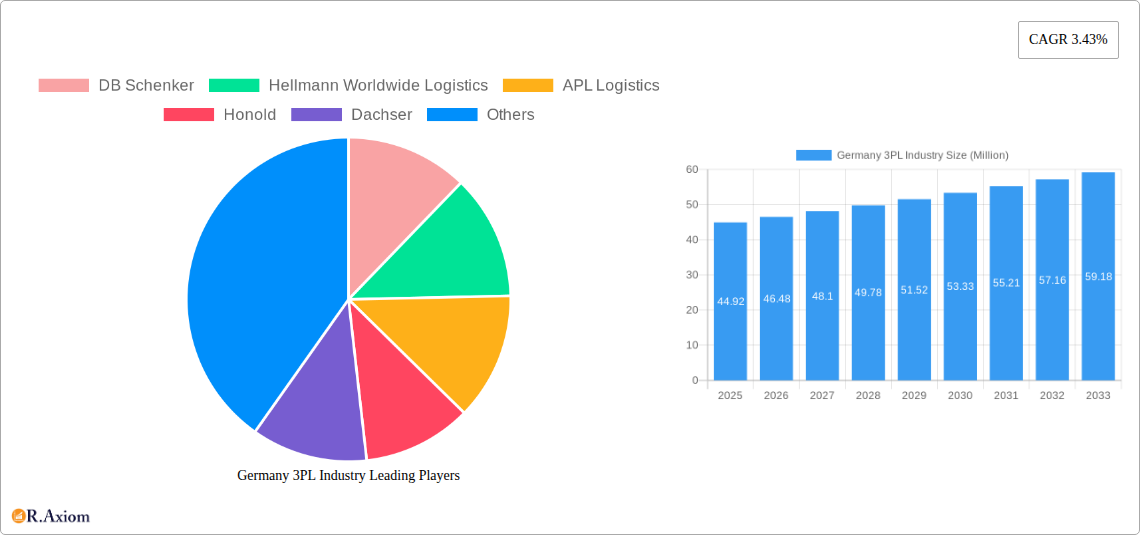

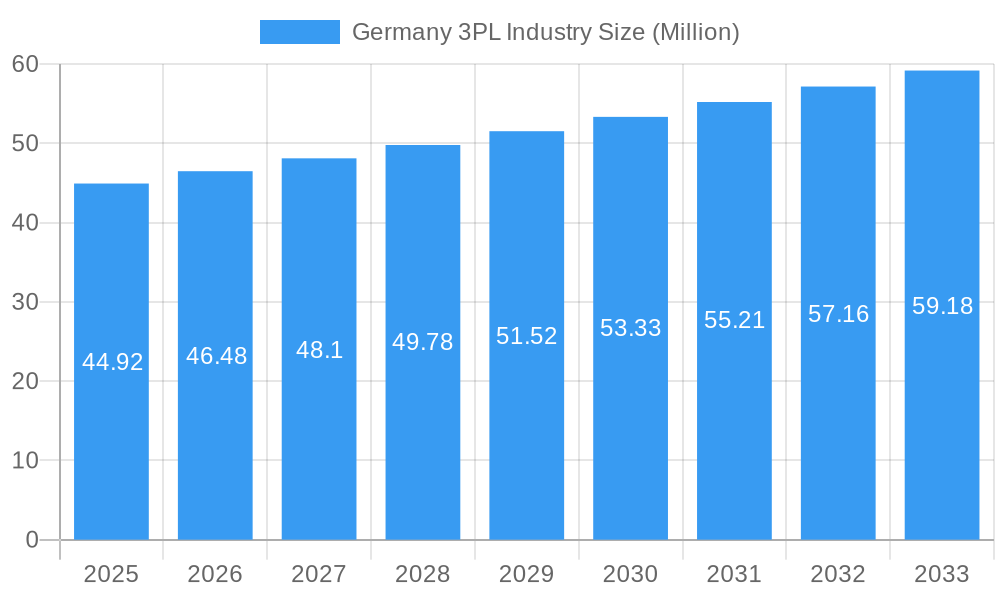

The German Third-Party Logistics (3PL) market is poised for steady expansion, with a projected market size of €44.92 million and an anticipated Compound Annual Growth Rate (CAGR) of 3.43% from 2019 to 2033. This growth is underpinned by robust demand across diverse sectors, particularly in domestic and international transportation management, and value-added warehousing and distribution services. The automotive industry continues to be a significant driver, alongside the burgeoning construction, consumer and retail (including e-commerce), and life sciences and healthcare sectors. The increasing adoption of advanced logistics solutions by manufacturing firms, coupled with the evolving needs of e-commerce, are crucial catalysts. Furthermore, a strong emphasis on supply chain optimization and efficiency by German businesses fuels the reliance on specialized 3PL providers. The market's trajectory indicates a sustained need for agile and technologically advanced logistics partners capable of navigating complex global supply chains.

Germany 3PL Industry Market Size (In Million)

Key trends shaping the German 3PL landscape include the increasing integration of digital technologies such as IoT, AI, and blockchain for enhanced visibility, automation, and predictive analytics within warehouses and transportation networks. The rise of e-commerce necessitates faster delivery times and sophisticated reverse logistics solutions, pushing 3PL providers to innovate their service offerings. Sustainability is also a growing concern, with a focus on green logistics, optimizing routes, and reducing carbon footprints. However, challenges such as rising operational costs, labor shortages, and the need for continuous infrastructure investment, particularly in digitalization and automation, present potential restraints. Despite these hurdles, the German 3PL market's inherent strengths, including its strategic location, advanced industrial base, and a well-established network of leading logistics companies like Deutsche Post DHL, DB Schenker, and Kuehne + Nagel, position it for continued resilience and growth.

Germany 3PL Industry Company Market Share

Germany 3PL Industry: Comprehensive Market Analysis and Strategic Outlook (2019–2033)

This in-depth report provides a granular analysis of the German Third-Party Logistics (3PL) industry, offering critical insights into market dynamics, growth drivers, and future trends. Covering the historical period of 2019-2024, a base and estimated year of 2025, and a comprehensive forecast period from 2025 to 2033, this report is an essential resource for logistics providers, shippers, investors, and industry stakeholders seeking to navigate and capitalize on the evolving German 3PL landscape. We explore market concentration, innovation, regulatory frameworks, end-user demands, and the competitive strategies of key players like Deutsche Post DHL, DB Schenker, Kuehne + Nagel, Dachser, and Hellmann Worldwide Logistics, among others. With a focus on key segments such as Domestic and International Transportation Management, Value-added Warehousing and Distribution, and end-users including Automobile, Consumer and Retail (E-commerce), and Life Sciences and Healthcare, this report equips you with actionable intelligence for strategic decision-making in one of Europe's most significant logistics markets.

Germany 3PL Industry Market Concentration & Innovation

The German 3PL market exhibits a moderately concentrated structure, with several large, established players like Deutsche Post DHL, DB Schenker, and Kuehne + Nagel holding significant market share, estimated to be over 60% collectively. This concentration is driven by substantial capital investment requirements, extensive network reach, and sophisticated technological capabilities. Innovation within the sector is a key differentiator, propelled by the increasing demand for digitalization, automation, and sustainability. Companies are actively investing in technologies such as AI-powered route optimization, IoT for real-time tracking, and robotic process automation in warehouses. Regulatory frameworks, particularly those concerning environmental standards and labor laws, play a crucial role in shaping operational strategies and fostering innovation in greener logistics solutions. Product substitutes, while present in the form of in-house logistics departments, are increasingly less viable for many businesses due to the complexity and cost-efficiency offered by specialized 3PL providers. End-user trends, such as the explosive growth of e-commerce, are forcing 3PLs to innovate rapidly in areas like last-mile delivery and returns management. Mergers and acquisitions (M&A) remain a significant strategy for market consolidation and capability expansion. Notable M&A activities in the past have seen deal values in the hundreds of millions of Euros, allowing larger players to acquire niche expertise or expand their geographic footprint. For instance, the acquisition of smaller, technology-focused logistics firms by established giants is a recurring theme. The industry's focus on innovation is not just about adopting new technologies but also about developing integrated service offerings that address the evolving needs of diverse end-user sectors.

Germany 3PL Industry Industry Trends & Insights

The German 3PL industry is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period. This expansion is underpinned by several key trends. Firstly, the burgeoning e-commerce sector is a primary growth driver, necessitating efficient and flexible fulfillment solutions, including advanced warehousing, last-mile delivery, and reverse logistics. This has led to an increased market penetration of specialized e-commerce logistics services. Secondly, the push towards sustainability and decarbonization across all industries is compelling 3PL providers to invest heavily in green logistics. This includes adopting electric and alternative fuel vehicles, optimizing route planning to reduce emissions, and developing carbon-neutral warehousing solutions. Deutsche Post DHL's significant investment in e-vehicles and climate-friendly operating sites, with a budget of EUR 300 million in 2022 alone, exemplifies this trend. Thirdly, digitalization and technological advancements are transforming the industry. The integration of AI, IoT, blockchain, and advanced analytics is enhancing operational efficiency, improving visibility, and enabling predictive capabilities throughout the supply chain. Companies are leveraging these technologies for everything from warehouse automation to predictive maintenance of fleets. Fourthly, the increasing complexity of global supply chains, coupled with geopolitical uncertainties, is driving demand for resilient and agile logistics networks. This has led to a greater reliance on 3PL providers who can offer end-to-end solutions and manage diverse risks. Consumer preferences are also evolving, with a growing emphasis on speed, transparency, and personalized delivery options. 3PLs are responding by investing in customer-centric technologies and flexible service models. Competitive dynamics are intensifying, with both established players and emerging innovators vying for market share. This competition is fostering a culture of continuous improvement and service differentiation, pushing the industry towards higher levels of service quality and efficiency. The market penetration of advanced logistics solutions is steadily increasing as businesses recognize the strategic advantage of outsourcing their logistics operations to specialized providers.

Dominant Markets & Segments in Germany 3PL Industry

Services Dominance:

Domestic Transportation Management: This segment holds a significant portion of the German 3PL market due to the country's strong manufacturing base and internal consumption. Key drivers include the need for efficient movement of goods between production sites, distribution centers, and end consumers.

- Economic Policies: Favorable trade policies and domestic economic growth directly stimulate demand for domestic transportation.

- Infrastructure: Germany's world-class road and rail infrastructure are crucial enablers for efficient domestic logistics.

- E-commerce Growth: The continued expansion of online retail significantly bolsters demand for last-mile delivery and inter-city freight movement.

Value-added Warehousing and Distribution: This segment is experiencing rapid growth, driven by the increasing complexity of supply chains and the demand for services beyond simple storage.

- E-commerce Fulfillment: The need for efficient picking, packing, and returns processing for online retailers is a major catalyst.

- Just-in-Time (JIT) Manufacturing: Industries like automotive rely heavily on precise inventory management and timely delivery of components, boosting demand for sophisticated warehousing.

- Customization and Personalization: 3PLs are offering services like kitting, assembly, and customized packaging to meet specific client needs.

International Transportation Management: While highly developed, this segment is susceptible to global economic fluctuations and geopolitical events. However, Germany's position as a major trading nation ensures its continued importance.

- Global Trade: Germany's export-oriented economy fuels continuous demand for international freight forwarding via sea, air, and land.

- Supply Chain Resilience: Companies are increasingly seeking integrated international solutions to manage the complexities and risks of global supply chains.

End User Dominance:

Consumer and Retail (including E-commerce): This sector is arguably the most dynamic and fastest-growing end-user segment for German 3PL services.

- E-commerce Explosion: The shift to online shopping has dramatically increased the volume of parcels and the demand for rapid, reliable delivery and efficient reverse logistics. 3PLs are critical in managing the complexity of online order fulfillment.

- Omnichannel Retail: Retailers are increasingly adopting omnichannel strategies, requiring 3PLs to integrate online and offline inventory management and delivery channels.

- Consumer Expectations: Consumers demand faster delivery times, real-time tracking, and flexible delivery options, pushing 3PLs to invest in technology and optimize last-mile networks.

Automobile: The German automotive industry, a cornerstone of its economy, is a major consumer of 3PL services, particularly for inbound logistics of components and outbound logistics of finished vehicles.

- Just-in-Time (JIT) and Just-in-Sequence (JIS): The automotive sector's reliance on lean manufacturing principles necessitates precise and timely delivery of parts to assembly lines.

- Global Supply Chains: The international nature of automotive manufacturing requires sophisticated global logistics networks for sourcing parts and distributing vehicles worldwide.

- Complex Logistics: Handling large, high-value vehicles and intricate component supply chains demands specialized logistics expertise.

Manufacturing: This broad sector encompasses various industries, each with unique logistics requirements, contributing significantly to the 3PL market.

- Industrial Goods: Efficient movement of raw materials, semi-finished products, and finished industrial goods is vital for production continuity.

- Supply Chain Optimization: Manufacturers seek 3PLs to streamline their supply chains, reduce costs, and improve efficiency through integrated logistics solutions.

- Specialized Handling: Depending on the product, specialized handling, storage, and transportation requirements can be extensive.

Germany 3PL Industry Product Developments

Recent product developments in the German 3PL industry are largely driven by technological innovation and the pursuit of sustainability. Companies are enhancing their service portfolios with advanced digital solutions, including AI-powered route optimization for reduced transit times and fuel consumption, and real-time visibility platforms leveraging IoT sensors for enhanced tracking and inventory management. The integration of robotics and automation in warehousing is improving efficiency and accuracy in order picking and packing. Furthermore, a significant focus is placed on developing green logistics products, such as carbon-neutral delivery options through electric fleets and optimized transportation modes like rail, as demonstrated by Deutsche Post DHL's "GoGreen Plus" portfolio. These developments aim to provide clients with greater efficiency, cost savings, enhanced transparency, and a reduced environmental footprint, thereby offering a competitive advantage in an increasingly discerning market.

Report Scope & Segmentation Analysis

This report meticulously analyzes the German Third-Party Logistics (3PL) industry across key service segments and end-user verticals. The Services scope encompasses Domestic Transportation Management, focusing on intra-country freight movement and last-mile delivery networks; International Transportation Management, covering global freight forwarding and cross-border logistics; and Value-added Warehousing and Distribution, which includes services like kitting, assembly, order fulfillment, and returns management. The End-User segmentation delves into the specific demands and logistics requirements of the Automobile sector, characterized by complex inbound and outbound supply chains; Construction, with its project-based and bulky material logistics; Consumer and Retail (including E-commerce), a high-growth area demanding fast, flexible, and efficient fulfillment; Life Sciences and Healthcare, requiring specialized handling, temperature control, and regulatory compliance; Manufacturing, covering a wide array of industrial and production logistics needs; and Other End Users, catering to diverse sectors. Each segment is analyzed for market size, growth projections, and competitive dynamics, providing a holistic view of the industry's structure and future potential.

Key Drivers of Germany 3PL Industry Growth

The growth of the German 3PL industry is propelled by several potent factors. The burgeoning e-commerce sector is a primary catalyst, demanding efficient fulfillment, last-mile delivery, and sophisticated returns management. Digitalization and technological advancements, including AI, IoT, and automation, are enhancing operational efficiency, visibility, and predictive capabilities across the supply chain. The increasing focus on sustainability and decarbonization is driving investment in green logistics, such as electric fleets and alternative fuels. Furthermore, the complexity of global supply chains and the need for resilience in the face of geopolitical uncertainties are increasing reliance on experienced 3PL providers for end-to-end solutions. Favorable economic policies and Germany's strong export-oriented economy also contribute to sustained demand for logistics services.

Challenges in the Germany 3PL Industry Sector

Despite robust growth, the German 3PL industry faces several challenges. Regulatory hurdles, particularly evolving environmental and labor laws, can increase operational costs and complexity. Intensifying competition from both established players and new entrants necessitates continuous innovation and efficiency improvements to maintain market share. Supply chain disruptions, stemming from global events, labor shortages, and infrastructure limitations, can impact delivery times and costs. The shortage of skilled labor, especially drivers and warehouse staff, remains a significant constraint on capacity. Furthermore, significant capital investment is required to adopt new technologies and sustainable solutions, which can be a barrier for smaller players. The pressure for cost optimization from clients, while driving efficiency, also squeezes profit margins.

Emerging Opportunities in Germany 3PL Industry

Emerging opportunities in the German 3PL industry are abundant and capitalize on current trends. The ongoing digital transformation presents opportunities for 3PLs that can offer advanced analytics, AI-driven optimization, and integrated digital platforms, thereby providing greater transparency and efficiency. The growing demand for sustainable logistics solutions opens doors for providers specializing in electric vehicle fleets, alternative fuels, and carbon-neutral operations. The expansion of e-commerce and omnichannel retail continues to fuel demand for specialized fulfillment, last-mile delivery, and reverse logistics services. There is also a significant opportunity in providing resilient and agile supply chain solutions to help businesses mitigate risks associated with global uncertainties. Furthermore, the increasing focus on circular economy principles and sustainable product lifecycles presents opportunities for 3PLs involved in repair, refurbishment, and recycling logistics.

Leading Players in the Germany 3PL Industry Market

- Deutsche Post DHL

- DB Schenker

- Kuehne + Nagel

- Dachser

- Hellmann Worldwide Logistics

- FIEGE Logistics

- Havi

- Honold

- Ziegler Logistics Deutschland

- Helm

- WemoveBW GmbH

- Rigterink Logistics

Key Developments in Germany 3PL Industry Industry

- Dec 2022: DACHSER plans to integrate 50 Mercedes-Benz eActros LongHaul units into its European fleet, underscoring a commitment to electric long-haul transportation and sustainable logistics.

- May 2022: Deutsche Post DHL added its 20,000th e-vehicle to its delivery fleet, marking a significant milestone in its sustainability efforts. The company allocated EUR 300 million in 2022 for green initiatives, including investments in climate-friendly operating sites and the acquisition of over 400 (bio) gas-powered trucks. Deutsche Post DHL also launched "GoGreen Plus" products to enable customers to actively reduce their carbon footprint through climate-friendly transport options like rail.

Strategic Outlook for Germany 3PL Industry Market

The strategic outlook for the German 3PL industry is exceptionally strong, driven by a confluence of evolving market demands and technological advancements. The continued expansion of e-commerce, coupled with the overarching trend towards sustainability, will necessitate sophisticated and green logistics solutions. 3PL providers that embrace digitalization, invest in electric and alternative fuel fleets, and optimize their networks for efficiency and resilience will be best positioned for success. Strategic partnerships and M&A activities are likely to continue as companies seek to expand capabilities, market reach, and technological expertise. The industry's future lies in offering integrated, data-driven, and environmentally responsible logistics services that adapt to the dynamic needs of a globalized and increasingly conscious marketplace. The investment in innovative technologies and sustainable practices will not only enhance operational performance but also serve as a critical differentiator in securing long-term growth and market leadership.

Germany 3PL Industry Segmentation

-

1. Services

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End User

- 2.1. Automobile

- 2.2. Construction

- 2.3. Consumer and Retail (including E-commerce)

- 2.4. Life Sciences and Healthcare

- 2.5. Manufacturing

- 2.6. Other End Users

Germany 3PL Industry Segmentation By Geography

- 1. Germany

Germany 3PL Industry Regional Market Share

Geographic Coverage of Germany 3PL Industry

Germany 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.43% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Automobile

- 5.2.2. Construction

- 5.2.3. Consumer and Retail (including E-commerce)

- 5.2.4. Life Sciences and Healthcare

- 5.2.5. Manufacturing

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Germany 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Automobile

- 6.2.2. Construction

- 6.2.3. Consumer and Retail (including E-commerce)

- 6.2.4. Life Sciences and Healthcare

- 6.2.5. Manufacturing

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hellmann Worldwide Logistics

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 APL Logistics

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Honold

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Dachser

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ziegler Logistics Deutschland**List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kuehne + Nagel

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 FIEGE Logistics

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Havi

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Helm

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 WemoveBW GmbH

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Rigterink Logistics

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Deutsche Post DHL

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany 3PL Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Germany 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany 3PL Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 2: Germany 3PL Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Germany 3PL Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Germany 3PL Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 5: Germany 3PL Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Germany 3PL Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany 3PL Industry?

The projected CAGR is approximately 3.43%.

2. Which companies are prominent players in the Germany 3PL Industry?

Key companies in the market include DB Schenker, Hellmann Worldwide Logistics, APL Logistics, Honold, Dachser, Ziegler Logistics Deutschland**List Not Exhaustive, Kuehne + Nagel, FIEGE Logistics, Havi, Helm, WemoveBW GmbH, Rigterink Logistics, Deutsche Post DHL.

3. What are the main segments of the Germany 3PL Industry?

The market segments include Services, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 44.92 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing E-commerce Sector.

6. What are the notable trends driving market growth?

Growth in the Automotive Sector to Drive the German 3PL Market.

7. Are there any restraints impacting market growth?

4.; Complicated Product Returns.

8. Can you provide examples of recent developments in the market?

Dec 2022: The logistics service provider DACHSER is planning to add 50 units of Mercedes-Benz eActros LongHaul, presented at IAA Transportation 2022, to its European fleet. The global company from Kempten signed a Letter of Intent with Mercedes-Benz Trucks to this end.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany 3PL Industry?

To stay informed about further developments, trends, and reports in the Germany 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence