Key Insights

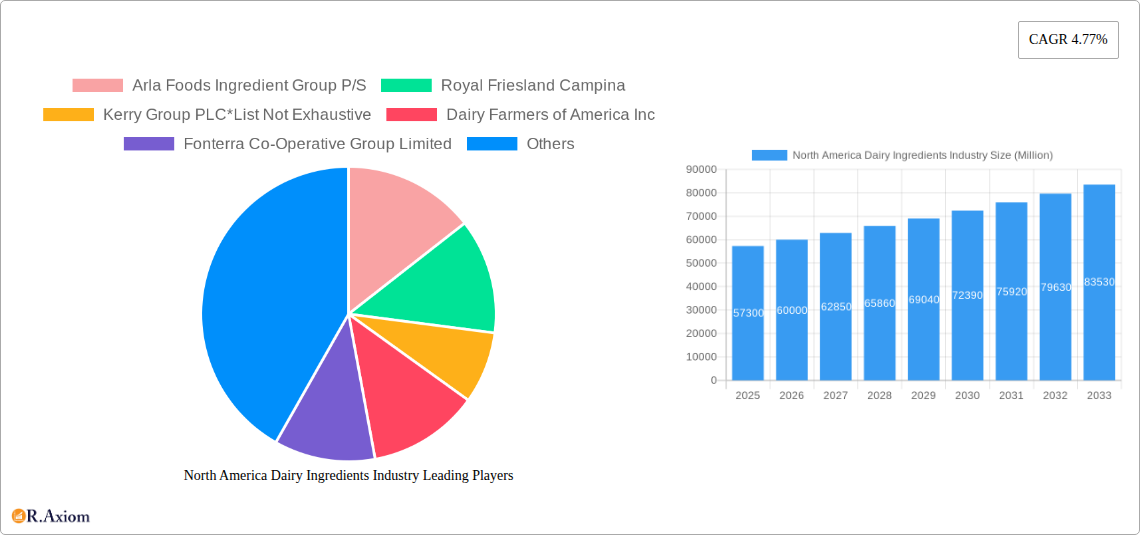

The North American dairy ingredients market, valued at $57.3 billion in 2025, is projected to experience robust growth, driven by increasing demand for convenient and nutritious food products. A compound annual growth rate (CAGR) of 4.77% from 2025 to 2033 indicates a significant expansion in market size. Key drivers include the rising popularity of functional foods and beverages incorporating dairy ingredients like whey protein for enhanced nutritional value and health benefits. The burgeoning sports nutrition sector, along with the expanding infant formula market, further fuels this growth. Growth in the bakery and confectionery sectors, where dairy ingredients provide texture and taste enhancement, also contributes significantly. While supply chain disruptions and fluctuating raw material prices pose challenges, innovation in dairy ingredient processing and the development of sustainable sourcing practices are mitigating these restraints. The market is segmented by type (milk powders, whey ingredients, casein and caseinates, etc.) and application (bakery, dairy products, infant formula, sports nutrition, etc.), providing varied opportunities for market players. The competitive landscape is characterized by both large multinational corporations and regional players, all vying for market share through product differentiation and strategic partnerships. North America, with its established dairy industry and high consumer spending on health-conscious products, commands a significant portion of this market.

Continued growth in the North American dairy ingredients market is expected, fueled by several factors. The increasing consumer awareness of health and wellness, coupled with rising disposable incomes, is driving demand for nutritious and convenient food options enriched with dairy ingredients. This is particularly evident in the sports nutrition and infant formula segments. Furthermore, ongoing research and development in dairy technology is leading to the creation of novel ingredients with enhanced functionalities, thereby expanding application possibilities across various food and beverage sectors. Growth is expected to be particularly robust in segments focused on clean-label products and sustainable sourcing, reflecting evolving consumer preferences. While potential challenges like regulatory changes and competition from plant-based alternatives exist, the inherent nutritional benefits of dairy ingredients and the ongoing innovations in the sector are likely to ensure continued market expansion throughout the forecast period.

North America Dairy Ingredients Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America dairy ingredients industry, covering market size, segmentation, key players, growth drivers, challenges, and future opportunities. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report leverages extensive primary and secondary research to deliver actionable insights for industry stakeholders, including manufacturers, suppliers, distributors, and investors.

North America Dairy Ingredients Industry Market Concentration & Innovation

The North America dairy ingredients market exhibits a moderately concentrated structure, with a few large players holding significant market share. Arla Foods Ingredient Group P/S, Royal Friesland Campina, Kerry Group PLC, Dairy Farmers of America Inc., Fonterra Co-Operative Group Limited, Groupe Lactalis, Saputo Inc., Kanegrade Ltd, Nestlé S.A., and Land O'Lakes, Inc. are among the key players, although the exact market share for each varies and precise figures are proprietary to market research firms. Innovation is driven by consumer demand for functional and health-oriented dairy ingredients, leading to the development of novel products like hydrolyzed whey protein and specialized milk protein concentrates. Regulatory frameworks, such as those related to food safety and labeling, significantly influence industry practices. Product substitutes, such as plant-based alternatives, present a growing competitive challenge. End-user trends, particularly increased demand from the sports nutrition and infant formula sectors, are driving market growth. The market has witnessed significant M&A activity in recent years, with deal values reaching xx Million. Examples include the acquisition of Dairy Farmers of America Inc. by Dean Foods Company (though this is a past event, it reflects historical activity). These mergers and acquisitions reshape market dynamics, creating larger entities and influencing market concentration.

- Market Concentration: Moderately concentrated with top players holding significant market share.

- Innovation Drivers: Consumer demand for functional foods, health-conscious products.

- Regulatory Framework: Stringent food safety and labeling regulations.

- Product Substitutes: Plant-based alternatives pose a growing threat.

- End-user Trends: Increased demand from sports nutrition and infant formula sectors.

- M&A Activity: Significant M&A activity in recent years with deal values reaching xx Million (historical data included).

North America Dairy Ingredients Industry Industry Trends & Insights

The North American dairy ingredients market is witnessing robust growth, driven by several key factors. The rising demand for convenient and nutritious food products, fueled by changing lifestyles and increasing health awareness, is a major catalyst. Technological advancements in dairy processing and ingredient formulation are enabling the development of innovative products with enhanced functionalities and improved shelf life. Consumer preferences are shifting towards healthier and more sustainable options, leading to increased demand for organic and naturally sourced dairy ingredients. Competitive dynamics are intense, with companies constantly striving to differentiate their products through innovation, branding, and strategic partnerships. The market exhibits a compound annual growth rate (CAGR) of xx% during the forecast period (2025-2033), with market penetration expected to reach xx% by 2033. Specific challenges like fluctuating milk prices and increasing competition from plant-based alternatives continue to impact industry growth.

Dominant Markets & Segments in North America Dairy Ingredients Industry

The United States is the dominant market within North America for dairy ingredients, owing to its large population, robust dairy industry, and significant consumption of dairy products. Within segments, Whey Ingredients, followed by Milk Powders, command the largest market shares by type, driven by their versatility and applications across various food and beverage sectors. In terms of applications, the infant milk formula segment shows strong growth potential due to rising birth rates and increasing awareness of the nutritional benefits of dairy-based infant formulas.

- By Type:

- Whey Ingredients: High demand driven by versatility and applications in various food products. Key drivers include advancements in whey processing technologies and increasing health awareness.

- Milk Powders: Strong demand from the food and beverage industry. Key drivers include cost-effectiveness and long shelf life.

- Milk Protein Concentrate and Isolate: Growing demand due to health benefits and functionalities in sports nutrition and functional foods. Key drivers include technological advancement and rising health consciousness.

- Casein and Caseinates: Steady demand with applications in dairy products and infant formula. Key drivers include versatility and functional properties.

- Lactose and Derivatives: Moderate growth potential, influenced by applications in confectionery and dairy products. Key drivers include cost-effectiveness and various applications.

- Others: Niche applications with moderate growth prospects.

- By Application:

- Infant Milk Formula: High growth potential due to rising birth rates and increased health awareness.

- Sports and Clinical Nutrition: Growing demand for protein-rich ingredients, fueled by health and fitness trends.

- Bakery and Confectionery: Steady demand due to widespread use of dairy ingredients in baked goods and confectionery.

- Dairy Products: High volume of use, driving significant demand for dairy ingredients.

North America Dairy Ingredients Industry Product Developments

Recent product innovations focus on enhancing the functional and nutritional properties of dairy ingredients. Companies are developing specialized whey protein concentrates and isolates with improved solubility, digestibility, and functional properties catering to the growing demand for clean label products and specialized applications in the sports nutrition and infant formula markets. Technological advancements like microencapsulation and membrane filtration are key drivers in improving the functionalities of these ingredients.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the North America dairy ingredients market, segmented by type (Milk Powders, Whole Milk Powders, Milk Protein Concentrate and Isolate, Whey Ingredients, Hydrolyzed Whey Protein (HWP), Lactose and Derivatives, Casein and Caseinates, Others) and application (Bakery and Confectionery, Dairy Products, Infant Milk Formula, Sports and Clinical Nutrition, Other Applications). Each segment's growth projections, market size (in Million), and competitive dynamics are detailed in the full report.

Key Drivers of North America Dairy Ingredients Industry Growth

Several factors contribute to the industry's growth. The rising demand for convenient and nutritious food products, driven by changing lifestyles and increased health consciousness, is a primary driver. Technological advancements in dairy processing and ingredient formulation are leading to innovative products with improved functionalities. The increasing adoption of dairy ingredients in various food and beverage applications further fuels market expansion. Government support and investments in dairy research and development create a favorable environment for growth.

Challenges in the North America Dairy Ingredients Industry Sector

The industry faces several challenges. Fluctuating milk prices impact profitability and pricing strategies. Increasing competition from plant-based alternatives necessitates innovation and product differentiation. Stringent regulatory requirements concerning food safety and labeling necessitate compliance, which can add costs. Supply chain disruptions caused by geopolitical events and extreme weather can impact ingredient availability.

Emerging Opportunities in North America Dairy Ingredients Industry

The growth of functional foods and beverages, particularly those targeting specific health concerns, presents significant opportunities. The increasing demand for clean-label and sustainable ingredients opens doors for new product innovations. Expanding into new markets, such as emerging economies with growing middle classes, also presents potential. Investing in research and development to enhance the nutritional and functional properties of dairy ingredients ensures market competitiveness.

Leading Players in the North America Dairy Ingredients Industry Market

- Arla Foods Ingredient Group P/S

- Royal Friesland Campina

- Kerry Group PLC

- Dairy Farmers of America Inc

- Fonterra Co-Operative Group Limited

- Groupe Lactalis

- Saputo Inc

- Kanegrade Ltd

- Nestlé S.A.

- Land O'Lakes, Inc.

Key Developments in North America Dairy Ingredients Industry Industry

- 2022: Arla Foods Ingredient Group P/S launches new whey protein concentrates.

- 2021: Acquisition of Dairy Farmers of America Inc. by Dean Foods Company (historical event).

- 2020: Partnership between Fonterra Co-Operative Group Limited and DSM to develop novel dairy ingredients. (Further specific dates and details for other developments would need to be filled in from the available data.)

Strategic Outlook for North America Dairy Ingredients Industry Market

The North America dairy ingredients market holds significant growth potential, driven by factors such as increasing health consciousness, changing consumer preferences, and technological advancements. Companies focused on innovation, sustainability, and product differentiation are poised to succeed. The market will continue to see a shift towards specialized dairy ingredients tailored to meet specific functional and nutritional demands, particularly in the infant nutrition, sports nutrition, and functional food sectors. Strategic partnerships and collaborations will play a critical role in driving innovation and market expansion.

North America Dairy Ingredients Industry Segmentation

-

1. Type

-

1.1. Milk Powders

- 1.1.1. Skimmed Milk Powders

- 1.1.2. Whole Milk Powders

- 1.2. Milk Protein Concentrate and Milk Protein Isolate

-

1.3. Whey Ingredients

- 1.3.1. Whey Protein Concentrate (WPC)

- 1.3.2. Whey Protein Isolate (WPI)

- 1.3.3. Hydrolyzed Whey Protein (HWP)

- 1.4. Lactose and Derivatives

- 1.5. Casein And Caseinates

- 1.6. Others

-

1.1. Milk Powders

-

2. Application

- 2.1. Bakery and Confectionery

- 2.2. Dairy Products

- 2.3. Infant Milk Formula

- 2.4. Sports and Clinical Nutrition

- 2.5. Other Applications

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

- 3.4. Rest of North America

North America Dairy Ingredients Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Dairy Ingredients Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.77% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing demand for sports nutritional supplements

- 3.3. Market Restrains

- 3.3.1. Rising demand for plant-based protein

- 3.4. Market Trends

- 3.4.1. Whole Milk Powders Drove the Market Sales

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Milk Powders

- 5.1.1.1. Skimmed Milk Powders

- 5.1.1.2. Whole Milk Powders

- 5.1.2. Milk Protein Concentrate and Milk Protein Isolate

- 5.1.3. Whey Ingredients

- 5.1.3.1. Whey Protein Concentrate (WPC)

- 5.1.3.2. Whey Protein Isolate (WPI)

- 5.1.3.3. Hydrolyzed Whey Protein (HWP)

- 5.1.4. Lactose and Derivatives

- 5.1.5. Casein And Caseinates

- 5.1.6. Others

- 5.1.1. Milk Powders

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Bakery and Confectionery

- 5.2.2. Dairy Products

- 5.2.3. Infant Milk Formula

- 5.2.4. Sports and Clinical Nutrition

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.3.4. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Milk Powders

- 6.1.1.1. Skimmed Milk Powders

- 6.1.1.2. Whole Milk Powders

- 6.1.2. Milk Protein Concentrate and Milk Protein Isolate

- 6.1.3. Whey Ingredients

- 6.1.3.1. Whey Protein Concentrate (WPC)

- 6.1.3.2. Whey Protein Isolate (WPI)

- 6.1.3.3. Hydrolyzed Whey Protein (HWP)

- 6.1.4. Lactose and Derivatives

- 6.1.5. Casein And Caseinates

- 6.1.6. Others

- 6.1.1. Milk Powders

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Bakery and Confectionery

- 6.2.2. Dairy Products

- 6.2.3. Infant Milk Formula

- 6.2.4. Sports and Clinical Nutrition

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.3.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Canada North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Milk Powders

- 7.1.1.1. Skimmed Milk Powders

- 7.1.1.2. Whole Milk Powders

- 7.1.2. Milk Protein Concentrate and Milk Protein Isolate

- 7.1.3. Whey Ingredients

- 7.1.3.1. Whey Protein Concentrate (WPC)

- 7.1.3.2. Whey Protein Isolate (WPI)

- 7.1.3.3. Hydrolyzed Whey Protein (HWP)

- 7.1.4. Lactose and Derivatives

- 7.1.5. Casein And Caseinates

- 7.1.6. Others

- 7.1.1. Milk Powders

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Bakery and Confectionery

- 7.2.2. Dairy Products

- 7.2.3. Infant Milk Formula

- 7.2.4. Sports and Clinical Nutrition

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.3.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Mexico North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Milk Powders

- 8.1.1.1. Skimmed Milk Powders

- 8.1.1.2. Whole Milk Powders

- 8.1.2. Milk Protein Concentrate and Milk Protein Isolate

- 8.1.3. Whey Ingredients

- 8.1.3.1. Whey Protein Concentrate (WPC)

- 8.1.3.2. Whey Protein Isolate (WPI)

- 8.1.3.3. Hydrolyzed Whey Protein (HWP)

- 8.1.4. Lactose and Derivatives

- 8.1.5. Casein And Caseinates

- 8.1.6. Others

- 8.1.1. Milk Powders

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Bakery and Confectionery

- 8.2.2. Dairy Products

- 8.2.3. Infant Milk Formula

- 8.2.4. Sports and Clinical Nutrition

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.3.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of North America North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Milk Powders

- 9.1.1.1. Skimmed Milk Powders

- 9.1.1.2. Whole Milk Powders

- 9.1.2. Milk Protein Concentrate and Milk Protein Isolate

- 9.1.3. Whey Ingredients

- 9.1.3.1. Whey Protein Concentrate (WPC)

- 9.1.3.2. Whey Protein Isolate (WPI)

- 9.1.3.3. Hydrolyzed Whey Protein (HWP)

- 9.1.4. Lactose and Derivatives

- 9.1.5. Casein And Caseinates

- 9.1.6. Others

- 9.1.1. Milk Powders

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Bakery and Confectionery

- 9.2.2. Dairy Products

- 9.2.3. Infant Milk Formula

- 9.2.4. Sports and Clinical Nutrition

- 9.2.5. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.3.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. United States North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 11. Canada North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 12. Mexico North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 13. Rest of North America North America Dairy Ingredients Industry Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Arla Foods Ingredient Group P/S

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Royal Friesland Campina

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Kerry Group PLC*List Not Exhaustive

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Dairy Farmers of America Inc

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Fonterra Co-Operative Group Limited

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Groupe Lactalis

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Saputo Inc

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Kanegrade Ltd

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Nestlé S.A.

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Land O'Lakes Inc.

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.1 Arla Foods Ingredient Group P/S

List of Figures

- Figure 1: North America Dairy Ingredients Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Dairy Ingredients Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Dairy Ingredients Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Dairy Ingredients Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 3: North America Dairy Ingredients Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: North America Dairy Ingredients Industry Volume K Tons Forecast, by Type 2019 & 2032

- Table 5: North America Dairy Ingredients Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 6: North America Dairy Ingredients Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 7: North America Dairy Ingredients Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: North America Dairy Ingredients Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 9: North America Dairy Ingredients Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: North America Dairy Ingredients Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 11: North America Dairy Ingredients Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: North America Dairy Ingredients Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 13: United States North America Dairy Ingredients Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United States North America Dairy Ingredients Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 15: Canada North America Dairy Ingredients Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Dairy Ingredients Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Dairy Ingredients Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Mexico North America Dairy Ingredients Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 19: Rest of North America North America Dairy Ingredients Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of North America North America Dairy Ingredients Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 21: North America Dairy Ingredients Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 22: North America Dairy Ingredients Industry Volume K Tons Forecast, by Type 2019 & 2032

- Table 23: North America Dairy Ingredients Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 24: North America Dairy Ingredients Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 25: North America Dairy Ingredients Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Dairy Ingredients Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 27: North America Dairy Ingredients Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: North America Dairy Ingredients Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 29: North America Dairy Ingredients Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 30: North America Dairy Ingredients Industry Volume K Tons Forecast, by Type 2019 & 2032

- Table 31: North America Dairy Ingredients Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 32: North America Dairy Ingredients Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 33: North America Dairy Ingredients Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 34: North America Dairy Ingredients Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 35: North America Dairy Ingredients Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: North America Dairy Ingredients Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 37: North America Dairy Ingredients Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 38: North America Dairy Ingredients Industry Volume K Tons Forecast, by Type 2019 & 2032

- Table 39: North America Dairy Ingredients Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 40: North America Dairy Ingredients Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 41: North America Dairy Ingredients Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 42: North America Dairy Ingredients Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 43: North America Dairy Ingredients Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 44: North America Dairy Ingredients Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 45: North America Dairy Ingredients Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 46: North America Dairy Ingredients Industry Volume K Tons Forecast, by Type 2019 & 2032

- Table 47: North America Dairy Ingredients Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 48: North America Dairy Ingredients Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 49: North America Dairy Ingredients Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 50: North America Dairy Ingredients Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 51: North America Dairy Ingredients Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: North America Dairy Ingredients Industry Volume K Tons Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Dairy Ingredients Industry?

The projected CAGR is approximately 4.77%.

2. Which companies are prominent players in the North America Dairy Ingredients Industry?

Key companies in the market include Arla Foods Ingredient Group P/S, Royal Friesland Campina, Kerry Group PLC*List Not Exhaustive, Dairy Farmers of America Inc, Fonterra Co-Operative Group Limited, Groupe Lactalis, Saputo Inc, Kanegrade Ltd, Nestlé S.A., Land O'Lakes, Inc..

3. What are the main segments of the North America Dairy Ingredients Industry?

The market segments include Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 57300 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing demand for sports nutritional supplements.

6. What are the notable trends driving market growth?

Whole Milk Powders Drove the Market Sales.

7. Are there any restraints impacting market growth?

Rising demand for plant-based protein.

8. Can you provide examples of recent developments in the market?

Significant developments in the North America dairy ingredients industry include product launches, acquisitions, and partnerships. Examples include the launch of new whey protein concentrates by Arla Foods Ingredient Group P/S, the acquisition of Dairy Farmers of America Inc. by Dean Foods Company, and the partnership between Fonterra Co-Operative Group Limited and DSM to develop novel dairy ingredients.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Dairy Ingredients Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Dairy Ingredients Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Dairy Ingredients Industry?

To stay informed about further developments, trends, and reports in the North America Dairy Ingredients Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence