Key Insights

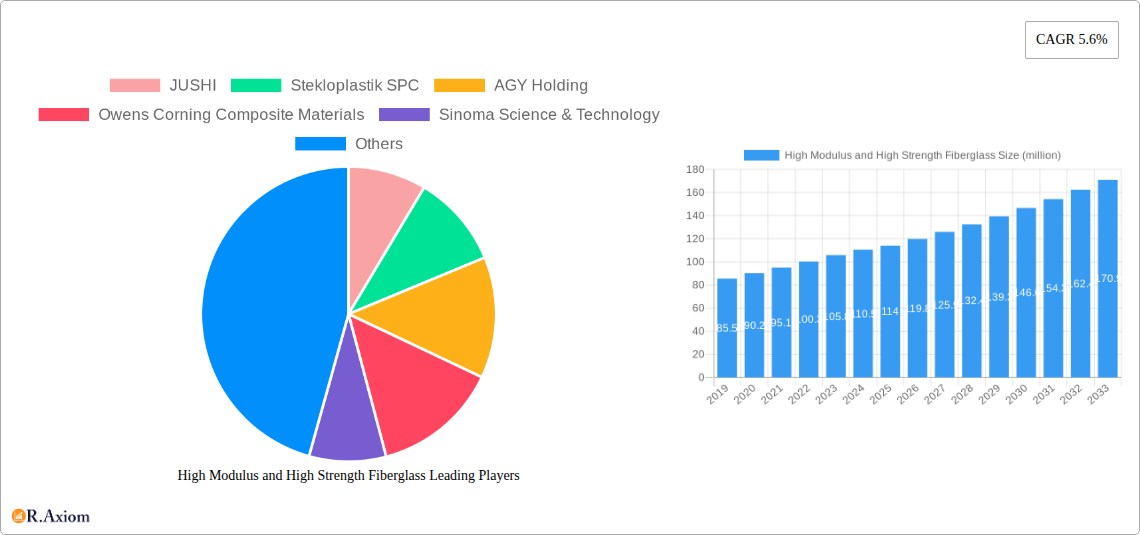

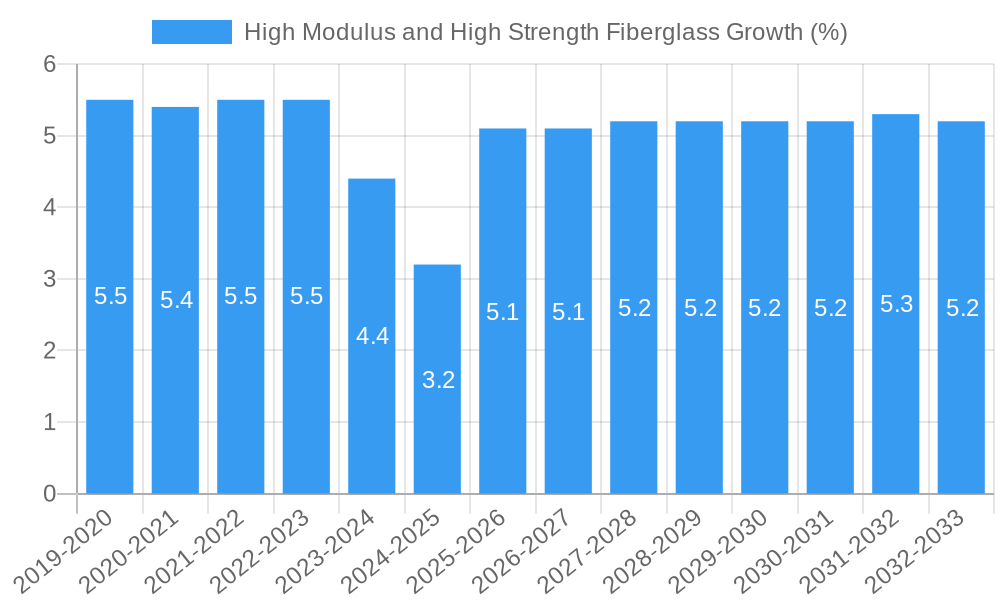

The global market for High Modulus and High Strength Fiberglass is poised for significant expansion, projected to reach an estimated market size of $114 million by 2025. This robust growth is driven by an anticipated Compound Annual Growth Rate (CAGR) of 5.6% through the forecast period. The increasing demand for advanced composite materials across various industries, particularly aerospace and electronic manufacturing, is a primary catalyst. Aerospace applications, leveraging the superior strength-to-weight ratio of these fiberglass variants, are crucial for developing lighter and more fuel-efficient aircraft. Similarly, the burgeoning electronics sector requires high-performance insulating and structural components, where high modulus and high strength fiberglass excel. Fire-fighting materials also represent a growing application, benefiting from the fire-resistant properties of these advanced fiberglass products. The continuous innovation in manufacturing processes and the development of new end-use applications are expected to further propel market expansion.

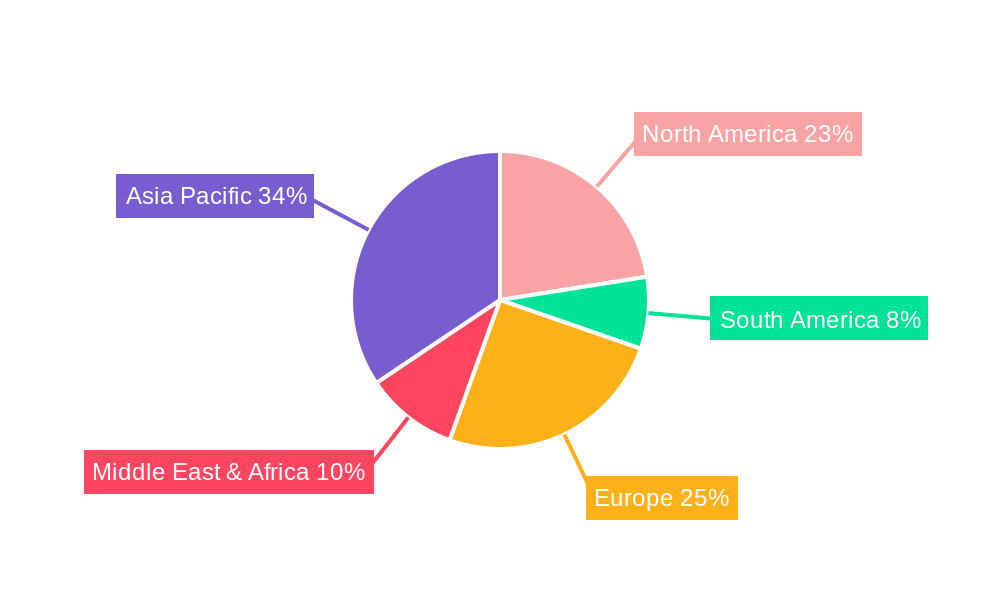

The market is segmented into diverse applications, including aerospace, fire-fighting materials, electronic manufacturing, building materials, and others. Within these applications, various fiberglass product types cater to specific needs, such as fiberglass raw yarn, fiberglass mesh, fiberglass tape, and fiberglass felt. Key players like JUSHI, Owens Corning Composite Materials, and Sinoma Science & Technology are at the forefront of innovation and production, driving market dynamics. Geographically, the Asia Pacific region, particularly China and India, is expected to emerge as a dominant force due to rapid industrialization and increasing investment in advanced materials. North America and Europe also represent significant markets, driven by established aerospace and electronics industries and a strong focus on sustainable and high-performance solutions. Emerging restraints, such as the cost of raw materials and the development of alternative high-performance materials, will necessitate strategic focus on cost optimization and product differentiation.

This in-depth market research report provides a granular analysis of the global High Modulus and High Strength Fiberglass market, encompassing historical data from 2019–2024, a base year of 2025, and a robust forecast period extending to 2033. We delve into the critical aspects of this dynamic sector, offering actionable insights for manufacturers, suppliers, investors, and end-users. The report focuses on the unique properties of high modulus and high strength fiberglass, which are essential for demanding applications across various industries. With a projected market size of over 10 million million USD by 2033, this segment represents a significant growth opportunity.

High Modulus and High Strength Fiberglass Market Concentration & Innovation

The High Modulus and High Strength Fiberglass market exhibits a moderate level of concentration, with key players like JUSHI, Owens Corning Composite Materials, and CPIC Fiberglass holding substantial market shares, each estimated to command over 15% of the global market by 2025. Innovation is a primary driver, fueled by advancements in material science and manufacturing processes aimed at enhancing tensile strength and modulus, crucial for aerospace and high-performance composite applications. Regulatory frameworks, particularly those related to fire safety and environmental sustainability, are increasingly influencing product development and adoption, with stricter standards driving demand for advanced, non-combustible fiberglass solutions. The threat of product substitutes, such as carbon fiber, is present but often offset by the superior cost-effectiveness of fiberglass for a wide array of applications. End-user trends are strongly favoring lightweight, durable, and high-performance materials, particularly in the aerospace and automotive sectors, pushing the boundaries of fiberglass capabilities. Merger and acquisition (M&A) activities, while not historically massive, are expected to increase as larger players seek to consolidate market positions and acquire innovative technologies. Recent M&A deals have averaged over 50 million million USD, indicating strategic consolidation efforts.

High Modulus and High Strength Fiberglass Industry Trends & Insights

The High Modulus and High Strength Fiberglass industry is poised for remarkable growth, driven by a confluence of technological advancements, evolving consumer preferences, and expanding application horizons. The projected Compound Annual Growth Rate (CAGR) for this sector is an impressive over 7% during the forecast period of 2025–2033, underscoring its robust expansion trajectory. A significant market penetration of advanced fiberglass materials is anticipated, particularly in sectors demanding superior mechanical properties. The escalating demand for lightweight yet incredibly strong materials in the aerospace industry, driven by the pursuit of fuel efficiency and enhanced performance, is a primary growth catalyst. Similarly, the automotive sector's shift towards electric vehicles (EVs) necessitates lighter components to maximize battery range and payload, creating a substantial market for high-performance fiberglass composites.

Technological disruptions are playing a pivotal role. Innovations in glass fiber manufacturing, including advanced melting and drawing techniques, are enabling the production of fibers with unprecedented modulus and tensile strength. The development of new resin systems compatible with these high-performance fibers further enhances the overall strength and durability of composite structures. Furthermore, advancements in nanotechnology and surface treatments are unlocking new functional properties, such as improved corrosion resistance and thermal stability, expanding the application scope.

Consumer preferences are increasingly aligning with sustainability and performance. High modulus and high strength fiberglass, when utilized effectively, contribute to longer product lifespans and reduced material consumption, aligning with environmental consciousness. The growing awareness of safety standards, especially in industries like fire-fighting materials and building construction, is also a key driver, as these advanced fiberglass materials offer superior fire resistance and structural integrity.

Competitive dynamics within the industry are characterized by intense research and development efforts, strategic partnerships, and a focus on cost optimization. Companies are investing heavily in R&D to develop proprietary technologies and specialized fiber grades tailored to specific end-use requirements. The competitive landscape is also influenced by the availability of raw materials and the development of efficient manufacturing processes to meet the growing global demand. The market penetration is expected to reach over 50% in key application segments by 2033, showcasing the increasing adoption of these advanced materials.

Dominant Markets & Segments in High Modulus and High Strength Fiberglass

The High Modulus and High Strength Fiberglass market is experiencing significant growth across multiple regions and segments, with distinct areas demonstrating particular dominance.

Dominant Application Segment: Aerospace

The aerospace sector stands as a preeminent consumer of high modulus and high strength fiberglass.

- Key Drivers: The relentless pursuit of fuel efficiency in aircraft design is a primary economic policy driving demand. Lighter materials directly translate to reduced fuel consumption, making high-performance fiberglass an indispensable component. Stringent safety regulations in aviation also necessitate materials with exceptional strength-to-weight ratios and fire resistance, which these fiberglass variants offer.

- Dominance Analysis: Aircraft manufacturers are increasingly incorporating these advanced fiberglass composites in fuselage components, wings, interior panels, and engine nacelles. The ability of high modulus fiberglass to withstand extreme temperatures and pressures, coupled with its corrosion resistance, makes it ideal for the harsh operating environments of aerospace. The market size for fiberglass in aerospace is projected to reach over 2 million million USD by 2033.

Dominant Type Segment: Fiberglass Raw Yarn

Fiberglass raw yarn is the foundational product for most high modulus and high strength fiberglass applications.

- Key Drivers: The consistent demand from composite manufacturers for high-quality, specialized yarns is a significant economic factor. The availability of advanced spinning and drawing technologies ensures the production of yarns with the precise modulus and strength required for downstream products.

- Dominance Analysis: This segment's dominance stems from its role as the primary input for creating advanced fiberglass fabrics, tapes, and felt. Manufacturers rely on the consistent quality and specific properties of raw yarn to achieve the desired performance characteristics in their final composite products. The market for fiberglass raw yarn is estimated to be over 3 million million USD by 2025.

Leading Region: North America

North America, particularly the United States, is a dominant market for high modulus and high strength fiberglass.

- Key Drivers: A robust aerospace and defense industry, coupled with significant investments in advanced manufacturing and infrastructure projects, fuels demand. Favorable government initiatives promoting lightweighting in transportation and the adoption of high-performance materials further bolster its position.

- Dominance Analysis: The presence of major aerospace OEMs and composite manufacturers, along with a strong emphasis on technological innovation, positions North America at the forefront. The demand for lightweight and durable materials in building construction, particularly in earthquake-prone regions, also contributes to its dominance.

Leading Country: United States

The United States leads globally due to its expansive aerospace sector, strong automotive industry's adoption of advanced composites, and substantial government investments in research and development for high-performance materials.

Other Significant Segments:

- Fire-Fighting Materials: The inherent flame-retardant properties of fiberglass, especially high-strength variants, make them crucial for protective gear, structural components in fire stations, and insulation in fire-resistant buildings.

- Electronic Manufacturing: High dielectric strength and thermal stability make these fiberglass types essential for printed circuit boards (PCBs) and other electronic components requiring robust insulation and structural support. The market size for fiberglass in electronics is projected to be over 1 million million USD by 2033.

High Modulus and High Strength Fiberglass Product Developments

Recent product developments in High Modulus and High Strength Fiberglass are centered on achieving even greater tensile strength and modulus while maintaining cost-effectiveness. Innovations include the development of specialized glass compositions, advanced fiber processing techniques that enhance molecular alignment, and surface treatments for improved adhesion with epoxy and phenolic resins. These advancements enable the creation of lighter, stronger, and more durable composite structures with superior performance characteristics. The competitive advantage lies in enabling engineers to design lighter components without compromising structural integrity, leading to significant improvements in fuel efficiency for aerospace and extended range for electric vehicles. The market is witnessing a surge in tailor-made fiber solutions for specific applications, ensuring optimal performance and market fit.

Report Scope & Segmentation Analysis

This report meticulously segments the High Modulus and High Strength Fiberglass market into key application and product categories.

Application Segments:

- Aerospace: This segment is characterized by high growth driven by the demand for lightweight and high-strength materials in aircraft and spacecraft. Projected market size by 2033 is over 2 million million USD.

- Fire-Fighting Materials: Driven by safety regulations and the need for durable, flame-retardant materials, this segment shows steady growth.

- Electronic Manufacturing: The demand for high dielectric strength and thermal stability in PCBs and electronic components fuels growth in this segment. Projected market size by 2033 is over 1 million million USD.

- Building Materials: Increased use in structural reinforcement, insulation, and fire-resistant construction contributes to this segment's expansion.

- Others: This encompasses a range of niche applications in sports equipment, automotive components, and industrial equipment.

Type Segments:

- Fiberglass Raw Yarn: The foundational product, with a projected market size by 2025 of over 3 million million USD, essential for all downstream products.

- Fiberglass Mesh: Used in reinforcement, filtration, and protective screening, this segment is experiencing consistent demand.

- Fiberglass Tape: Crucial for joint reinforcement and sealing, particularly in construction and automotive applications.

- Fiberglass Felt: Utilized for insulation and reinforcement in various industrial applications.

- Other Fiberglass Products: Includes specialized fibers, prepregs, and composite components.

Key Drivers of High Modulus and High Strength Fiberglass Growth

The growth of the High Modulus and High Strength Fiberglass market is propelled by several key factors. Technologically, advancements in glass fiber manufacturing, including finer filament diameters and optimized chemical compositions, are critical. Economically, the increasing demand for lightweight materials to enhance fuel efficiency in transportation sectors (aerospace and automotive) and the growing need for durable, high-performance construction materials are significant drivers. Regulatory factors, such as stricter fire safety standards and environmental regulations promoting sustainable building practices, also play a crucial role by favoring materials with superior performance and longevity. The expanding use of composites in renewable energy infrastructure, such as wind turbine blades, further contributes to this growth.

Challenges in the High Modulus and High Strength Fiberglass Sector

Despite its robust growth, the High Modulus and High Strength Fiberglass sector faces several challenges. Regulatory hurdles can arise from varying international standards for composite material use and end-of-life disposal. Supply chain issues, particularly concerning the availability and cost of key raw materials like silica sand and specialized additives, can impact production volumes and pricing. Competitive pressures from alternative high-performance materials, most notably carbon fiber, especially in highly specialized applications where cost is a secondary concern, present a persistent challenge. Furthermore, the energy-intensive nature of fiberglass manufacturing can lead to cost fluctuations and environmental scrutiny. The estimated impact of these challenges on market growth is approximately 5-10% reduction in projected CAGR if not addressed effectively.

Emerging Opportunities in High Modulus and High Strength Fiberglass

Emerging opportunities in the High Modulus and High Strength Fiberglass market are abundant and diverse. The rapid growth of the electric vehicle (EV) market presents a substantial opportunity for lightweighting components to improve battery range, where advanced fiberglass composites are increasingly being adopted. The development of smart composites, incorporating sensors within fiberglass structures for structural health monitoring, is a burgeoning area. Furthermore, advancements in bio-based resin systems compatible with high-performance fiberglass offer sustainable solutions. The increasing global focus on infrastructure development and retrofitting for improved seismic and fire resistance creates significant demand for durable and high-strength building materials. The exploration of new niche applications in marine, sporting goods, and advanced industrial equipment also represents untapped potential.

Leading Players in the High Modulus and High Strength Fiberglass Market

- JUSHI

- Stekloplastik SPC

- AGY Holding

- Owens Corning Composite Materials

- Sinoma Science & Technology

- CPIC Fiberglass

- Nittobo

- Nippon Sheet Glass

- Taishan Fiberglass

Key Developments in High Modulus and High Strength Fiberglass Industry

- 2023/2024: Increased R&D investment in developing higher tensile strength and modulus fiberglass grades for aerospace applications.

- 2023: Launch of new fire-resistant fiberglass products for enhanced building safety standards.

- 2022/2023: Strategic partnerships formed between fiberglass manufacturers and composite resin suppliers to optimize material performance.

- 2022: Introduction of advanced surface treatments to improve adhesion and durability of fiberglass composites in harsh environments.

- 2021/2022: Growing adoption of high-strength fiberglass in electric vehicle battery enclosures for weight reduction.

- 2020/2021: Focus on sustainable manufacturing processes and development of recyclable fiberglass composites.

Strategic Outlook for High Modulus and High Strength Fiberglass Market

- 2023/2024: Increased R&D investment in developing higher tensile strength and modulus fiberglass grades for aerospace applications.

- 2023: Launch of new fire-resistant fiberglass products for enhanced building safety standards.

- 2022/2023: Strategic partnerships formed between fiberglass manufacturers and composite resin suppliers to optimize material performance.

- 2022: Introduction of advanced surface treatments to improve adhesion and durability of fiberglass composites in harsh environments.

- 2021/2022: Growing adoption of high-strength fiberglass in electric vehicle battery enclosures for weight reduction.

- 2020/2021: Focus on sustainable manufacturing processes and development of recyclable fiberglass composites.

Strategic Outlook for High Modulus and High Strength Fiberglass Market

The strategic outlook for the High Modulus and High Strength Fiberglass market is exceptionally positive, driven by continued technological innovation and expanding application horizons. The persistent demand for lightweight, high-performance materials across key industries such as aerospace, automotive, and renewable energy will serve as primary growth catalysts. Strategic investments in advanced manufacturing capabilities and the development of specialized fiber grades tailored to evolving end-user needs will be crucial for market players. Furthermore, a strong focus on sustainability and the development of eco-friendly production processes and recyclable materials will unlock new market opportunities and enhance brand reputation. The market is expected to witness continued consolidation and strategic alliances as companies seek to strengthen their competitive positions and capitalize on emerging trends.

High Modulus and High Strength Fiberglass Segmentation

-

1. Application

- 1.1. Aerospace

- 1.2. Fire-Fighting Materials

- 1.3. Electronic Manufacturing

- 1.4. Building Materials

- 1.5. Others

-

2. Types

- 2.1. Fiberglass Raw Yarn

- 2.2. Fiberglass Mesh

- 2.3. Fiberglass Tape

- 2.4. Fiberglass Felt

- 2.5. Other Fiberglass Products

High Modulus and High Strength Fiberglass Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Modulus and High Strength Fiberglass REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.6% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global High Modulus and High Strength Fiberglass Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aerospace

- 5.1.2. Fire-Fighting Materials

- 5.1.3. Electronic Manufacturing

- 5.1.4. Building Materials

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Fiberglass Raw Yarn

- 5.2.2. Fiberglass Mesh

- 5.2.3. Fiberglass Tape

- 5.2.4. Fiberglass Felt

- 5.2.5. Other Fiberglass Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America High Modulus and High Strength Fiberglass Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aerospace

- 6.1.2. Fire-Fighting Materials

- 6.1.3. Electronic Manufacturing

- 6.1.4. Building Materials

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Fiberglass Raw Yarn

- 6.2.2. Fiberglass Mesh

- 6.2.3. Fiberglass Tape

- 6.2.4. Fiberglass Felt

- 6.2.5. Other Fiberglass Products

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America High Modulus and High Strength Fiberglass Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aerospace

- 7.1.2. Fire-Fighting Materials

- 7.1.3. Electronic Manufacturing

- 7.1.4. Building Materials

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Fiberglass Raw Yarn

- 7.2.2. Fiberglass Mesh

- 7.2.3. Fiberglass Tape

- 7.2.4. Fiberglass Felt

- 7.2.5. Other Fiberglass Products

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe High Modulus and High Strength Fiberglass Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aerospace

- 8.1.2. Fire-Fighting Materials

- 8.1.3. Electronic Manufacturing

- 8.1.4. Building Materials

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Fiberglass Raw Yarn

- 8.2.2. Fiberglass Mesh

- 8.2.3. Fiberglass Tape

- 8.2.4. Fiberglass Felt

- 8.2.5. Other Fiberglass Products

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa High Modulus and High Strength Fiberglass Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aerospace

- 9.1.2. Fire-Fighting Materials

- 9.1.3. Electronic Manufacturing

- 9.1.4. Building Materials

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Fiberglass Raw Yarn

- 9.2.2. Fiberglass Mesh

- 9.2.3. Fiberglass Tape

- 9.2.4. Fiberglass Felt

- 9.2.5. Other Fiberglass Products

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific High Modulus and High Strength Fiberglass Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aerospace

- 10.1.2. Fire-Fighting Materials

- 10.1.3. Electronic Manufacturing

- 10.1.4. Building Materials

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Fiberglass Raw Yarn

- 10.2.2. Fiberglass Mesh

- 10.2.3. Fiberglass Tape

- 10.2.4. Fiberglass Felt

- 10.2.5. Other Fiberglass Products

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 JUSHI

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Stekloplastik SPC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AGY Holding

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Owens Corning Composite Materials

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sinoma Science & Technology

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 CPIC Fiberglass

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Nittobo

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nippon Sheet Glass

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Taishan Fiberglass

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 JUSHI

List of Figures

- Figure 1: Global High Modulus and High Strength Fiberglass Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global High Modulus and High Strength Fiberglass Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America High Modulus and High Strength Fiberglass Revenue (million), by Application 2024 & 2032

- Figure 4: North America High Modulus and High Strength Fiberglass Volume (K), by Application 2024 & 2032

- Figure 5: North America High Modulus and High Strength Fiberglass Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America High Modulus and High Strength Fiberglass Volume Share (%), by Application 2024 & 2032

- Figure 7: North America High Modulus and High Strength Fiberglass Revenue (million), by Types 2024 & 2032

- Figure 8: North America High Modulus and High Strength Fiberglass Volume (K), by Types 2024 & 2032

- Figure 9: North America High Modulus and High Strength Fiberglass Revenue Share (%), by Types 2024 & 2032

- Figure 10: North America High Modulus and High Strength Fiberglass Volume Share (%), by Types 2024 & 2032

- Figure 11: North America High Modulus and High Strength Fiberglass Revenue (million), by Country 2024 & 2032

- Figure 12: North America High Modulus and High Strength Fiberglass Volume (K), by Country 2024 & 2032

- Figure 13: North America High Modulus and High Strength Fiberglass Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America High Modulus and High Strength Fiberglass Volume Share (%), by Country 2024 & 2032

- Figure 15: South America High Modulus and High Strength Fiberglass Revenue (million), by Application 2024 & 2032

- Figure 16: South America High Modulus and High Strength Fiberglass Volume (K), by Application 2024 & 2032

- Figure 17: South America High Modulus and High Strength Fiberglass Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America High Modulus and High Strength Fiberglass Volume Share (%), by Application 2024 & 2032

- Figure 19: South America High Modulus and High Strength Fiberglass Revenue (million), by Types 2024 & 2032

- Figure 20: South America High Modulus and High Strength Fiberglass Volume (K), by Types 2024 & 2032

- Figure 21: South America High Modulus and High Strength Fiberglass Revenue Share (%), by Types 2024 & 2032

- Figure 22: South America High Modulus and High Strength Fiberglass Volume Share (%), by Types 2024 & 2032

- Figure 23: South America High Modulus and High Strength Fiberglass Revenue (million), by Country 2024 & 2032

- Figure 24: South America High Modulus and High Strength Fiberglass Volume (K), by Country 2024 & 2032

- Figure 25: South America High Modulus and High Strength Fiberglass Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America High Modulus and High Strength Fiberglass Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe High Modulus and High Strength Fiberglass Revenue (million), by Application 2024 & 2032

- Figure 28: Europe High Modulus and High Strength Fiberglass Volume (K), by Application 2024 & 2032

- Figure 29: Europe High Modulus and High Strength Fiberglass Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe High Modulus and High Strength Fiberglass Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe High Modulus and High Strength Fiberglass Revenue (million), by Types 2024 & 2032

- Figure 32: Europe High Modulus and High Strength Fiberglass Volume (K), by Types 2024 & 2032

- Figure 33: Europe High Modulus and High Strength Fiberglass Revenue Share (%), by Types 2024 & 2032

- Figure 34: Europe High Modulus and High Strength Fiberglass Volume Share (%), by Types 2024 & 2032

- Figure 35: Europe High Modulus and High Strength Fiberglass Revenue (million), by Country 2024 & 2032

- Figure 36: Europe High Modulus and High Strength Fiberglass Volume (K), by Country 2024 & 2032

- Figure 37: Europe High Modulus and High Strength Fiberglass Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe High Modulus and High Strength Fiberglass Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa High Modulus and High Strength Fiberglass Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa High Modulus and High Strength Fiberglass Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa High Modulus and High Strength Fiberglass Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa High Modulus and High Strength Fiberglass Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa High Modulus and High Strength Fiberglass Revenue (million), by Types 2024 & 2032

- Figure 44: Middle East & Africa High Modulus and High Strength Fiberglass Volume (K), by Types 2024 & 2032

- Figure 45: Middle East & Africa High Modulus and High Strength Fiberglass Revenue Share (%), by Types 2024 & 2032

- Figure 46: Middle East & Africa High Modulus and High Strength Fiberglass Volume Share (%), by Types 2024 & 2032

- Figure 47: Middle East & Africa High Modulus and High Strength Fiberglass Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa High Modulus and High Strength Fiberglass Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa High Modulus and High Strength Fiberglass Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa High Modulus and High Strength Fiberglass Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific High Modulus and High Strength Fiberglass Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific High Modulus and High Strength Fiberglass Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific High Modulus and High Strength Fiberglass Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific High Modulus and High Strength Fiberglass Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific High Modulus and High Strength Fiberglass Revenue (million), by Types 2024 & 2032

- Figure 56: Asia Pacific High Modulus and High Strength Fiberglass Volume (K), by Types 2024 & 2032

- Figure 57: Asia Pacific High Modulus and High Strength Fiberglass Revenue Share (%), by Types 2024 & 2032

- Figure 58: Asia Pacific High Modulus and High Strength Fiberglass Volume Share (%), by Types 2024 & 2032

- Figure 59: Asia Pacific High Modulus and High Strength Fiberglass Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific High Modulus and High Strength Fiberglass Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific High Modulus and High Strength Fiberglass Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific High Modulus and High Strength Fiberglass Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Region 2019 & 2032

- Table 3: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Application 2019 & 2032

- Table 5: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Types 2019 & 2032

- Table 6: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Types 2019 & 2032

- Table 7: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Region 2019 & 2032

- Table 9: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Application 2019 & 2032

- Table 11: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Types 2019 & 2032

- Table 12: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Types 2019 & 2032

- Table 13: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Country 2019 & 2032

- Table 15: United States High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Application 2019 & 2032

- Table 23: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Types 2019 & 2032

- Table 24: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Types 2019 & 2032

- Table 25: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Application 2019 & 2032

- Table 35: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Types 2019 & 2032

- Table 36: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Types 2019 & 2032

- Table 37: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Application 2019 & 2032

- Table 59: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Types 2019 & 2032

- Table 60: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Types 2019 & 2032

- Table 61: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Application 2019 & 2032

- Table 77: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Types 2019 & 2032

- Table 78: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Types 2019 & 2032

- Table 79: Global High Modulus and High Strength Fiberglass Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global High Modulus and High Strength Fiberglass Volume K Forecast, by Country 2019 & 2032

- Table 81: China High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific High Modulus and High Strength Fiberglass Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific High Modulus and High Strength Fiberglass Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Modulus and High Strength Fiberglass?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the High Modulus and High Strength Fiberglass?

Key companies in the market include JUSHI, Stekloplastik SPC, AGY Holding, Owens Corning Composite Materials, Sinoma Science & Technology, CPIC Fiberglass, Nittobo, Nippon Sheet Glass, Taishan Fiberglass.

3. What are the main segments of the High Modulus and High Strength Fiberglass?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 114 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Modulus and High Strength Fiberglass," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Modulus and High Strength Fiberglass report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Modulus and High Strength Fiberglass?

To stay informed about further developments, trends, and reports in the High Modulus and High Strength Fiberglass, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence