Key Insights

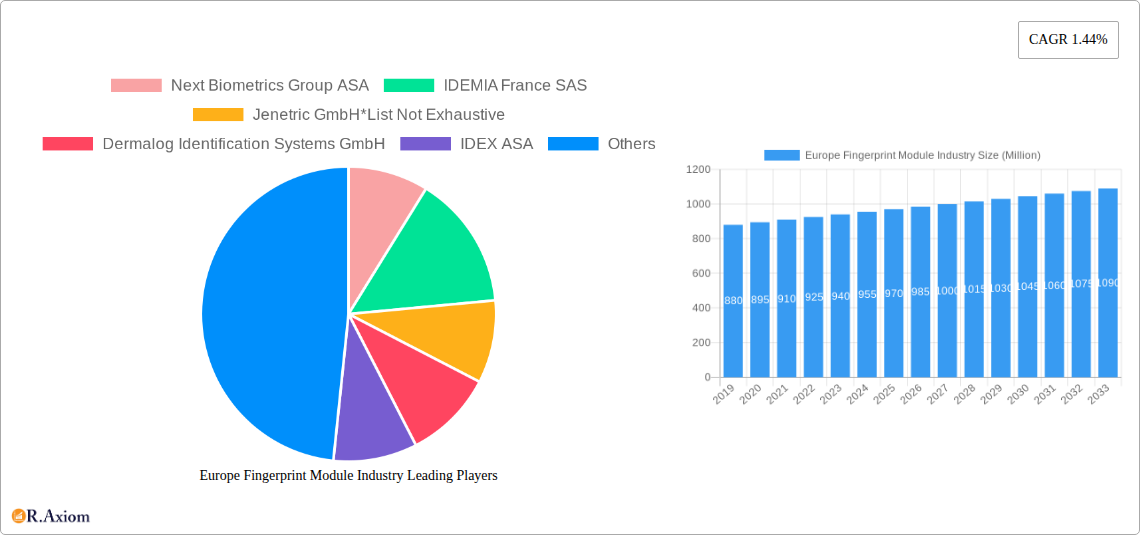

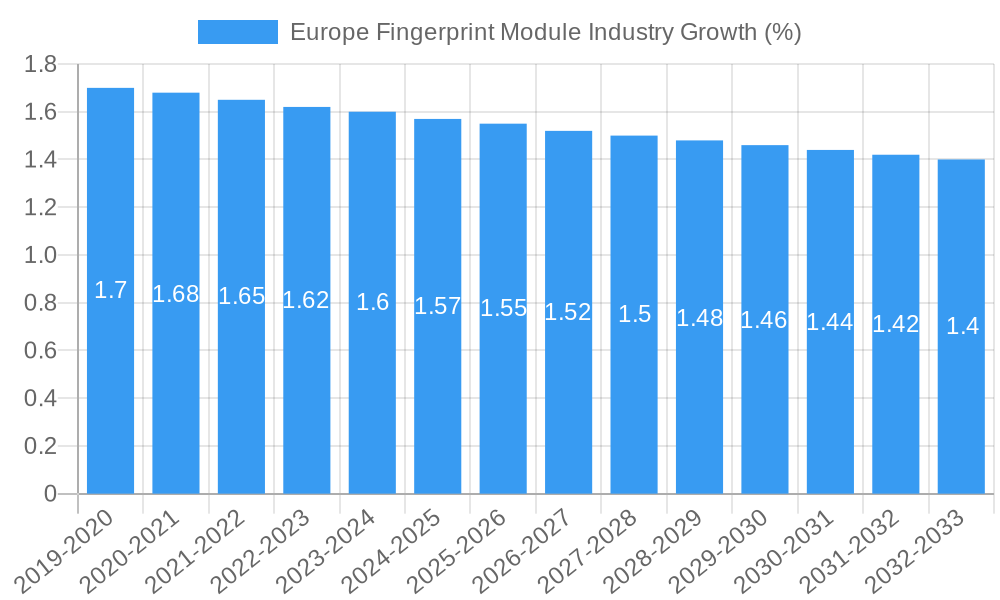

The European Fingerprint Module Industry is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 1.44% over the forecast period of 2025-2033. While this growth rate is modest, it reflects a mature market where fingerprint module integration is already widespread in key applications. The market's current valuation, estimated at around $950 million in 2025, is driven by the pervasive demand for enhanced security and authentication across various sectors. Consumer electronics, particularly smartphones and tablets, continue to be the primary demand generator, with ongoing advancements in sensor technology and user convenience fueling adoption. However, the increasing integration of fingerprint modules in laptops, smartcards, and the rapidly expanding Internet of Things (IoT) ecosystem are emerging as significant growth contributors. The BFSI (Banking, Financial Services, and Insurance) sector also plays a crucial role, leveraging fingerprint technology for secure transactions and customer verification.

Several factors shape the trajectory of the European fingerprint module market. The relentless pursuit of robust security solutions across both consumer and enterprise landscapes acts as a strong driver. Advancements in optical and capacitive sensor technologies offer improved accuracy, speed, and cost-effectiveness, making them more appealing for a wider range of devices. The growing adoption of biometric authentication in government and military applications further solidifies market demand. Conversely, the market faces restraints such as the increasing commoditization of basic fingerprint technology, leading to price pressures, and the emergence of alternative biometric modalities like facial recognition, which may offer a perceived higher level of convenience in certain use cases. Furthermore, stringent data privacy regulations, while essential for consumer trust, can introduce complexities in deployment and data management. Despite these challenges, the inherent reliability and established user familiarity with fingerprint scanning are expected to sustain its relevance and drive incremental market expansion.

The Europe Fingerprint Module Industry is characterized by a moderate to high market concentration, with a few key players holding significant market share. Innovation is a primary driver, fueled by ongoing advancements in biometric technologies and increasing demand for enhanced security solutions across various applications. Regulatory frameworks, particularly those concerning data privacy and biometric data protection, play a crucial role in shaping product development and market access, notably GDPR compliance. While direct product substitutes are limited, the emergence of alternative biometric modalities like facial recognition and iris scanning presents an indirect competitive threat. End-user trends are overwhelmingly focused on seamless integration, improved accuracy, and cost-effectiveness, driving demand for advanced capacitive and ultrasonic fingerprint sensors. Mergers and acquisitions (M&A) activities are strategic, aimed at consolidating market presence, acquiring new technologies, and expanding product portfolios. For instance, significant M&A deals valued in the tens to hundreds of millions of Euros are anticipated to reshape the competitive landscape. Companies like IDEMIA France SAS and Fingerprint Cards AB are at the forefront of these consolidation efforts.

Europe Fingerprint Module Industry Industry Trends & Insights

The Europe Fingerprint Module Industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033. This expansion is primarily propelled by the escalating demand for secure and convenient authentication methods across a multitude of consumer electronics and enterprise applications. The increasing penetration of smartphones and tablets, which are now standard in most European households, continues to be a dominant market segment, with over 85% of new devices incorporating fingerprint sensors. Laptops and personal computers are also witnessing a significant uptake in fingerprint module integration, driven by corporate security mandates and the desire for a frictionless user experience, with market penetration expected to surpass 60% by 2028. The burgeoning Internet of Things (IoT) ecosystem, encompassing smart homes, wearables, and industrial devices, presents a substantial growth avenue, with an estimated market penetration of over 40% by the forecast period's end.

Technological disruptions are at the heart of this industry's evolution. The shift from traditional optical fingerprint sensors to more advanced capacitive and increasingly ultrasonic technologies is a defining trend. Ultrasonic sensors, offering superior performance in terms of speed, accuracy, and the ability to work with wet or dirty fingers, are gaining traction, particularly in premium smartphone segments and for high-security applications in the BFSI and Government sectors. This technological evolution is enabling thinner and more aesthetically integrated sensor designs, further enhancing consumer appeal. Consumer preferences are shifting towards invisible or under-display fingerprint sensors, driven by the desire for seamless device aesthetics and a more intuitive user experience. Companies are investing heavily in research and development to meet these demands, with R&D spending in the sector estimated to reach over 300 million Euros annually by 2027.

Competitive dynamics are intensifying, with established players continually innovating and emerging companies seeking niche market penetration. Strategic partnerships between sensor manufacturers, device OEMs, and software providers are becoming increasingly crucial for end-to-end solution delivery. The focus on cybersecurity, coupled with the convenience offered by fingerprint authentication, ensures a sustained demand. Furthermore, the growing adoption of biometric payment systems and secure access controls within the BFSI sector, along with stringent security requirements in Military and Defense applications, are creating significant market opportunities. The overall market size is expected to reach approximately 2.5 billion Euros by 2033, with Europe representing a substantial portion of this global market.

Dominant Markets & Segments in Europe Fingerprint Module Industry

The Europe Fingerprint Module Industry is dominated by Western European countries, with Germany, France, and the United Kingdom leading the market in terms of adoption and technological advancement. The robust consumer electronics manufacturing base, strong financial services sector, and proactive government initiatives promoting digital security are key drivers of this dominance. Economic policies that encourage innovation and investment in high-technology sectors further bolster their market position. Infrastructure development, particularly in secure digital payment systems and government identity solutions, plays a critical role in driving the demand for fingerprint modules.

Application Segment Dominance:

- Smartphones/Tablets: This segment continues to be the largest and most influential, driven by high consumer adoption rates and the ubiquitous presence of these devices. Over 90% of smartphones and 75% of tablets sold in Europe in the base year 2025 are equipped with fingerprint modules. The demand for faster, more accurate, and under-display sensors fuels innovation and market growth within this segment.

- Laptops: The increasing focus on enterprise security and the growing trend of remote work have significantly boosted the adoption of fingerprint modules in laptops. Market penetration is projected to reach 65% by 2028, with a steady demand for integrated solutions that enhance user productivity and data protection.

- Smartcards: While currently a smaller segment, smartcards are showing significant growth potential, particularly in payment and access control applications. The increasing demand for secure payment solutions and the development of next-generation smart identity cards are expected to drive this segment, with a projected market size of over 150 million Euros by 2030.

- IoT and Other Applications: This segment, encompassing wearables, smart home devices, and industrial automation, represents a rapidly expanding frontier. The need for secure, low-power, and cost-effective authentication solutions for a diverse range of connected devices is driving innovation and adoption. Market penetration is expected to exceed 45% by 2033, with substantial growth fueled by emerging smart city initiatives and the proliferation of connected industrial equipment.

End-user Industry Dominance:

- Consumer Electronics: This remains the largest end-user industry, primarily driven by the demand from the smartphone, tablet, and laptop markets. The desire for enhanced security and convenient authentication methods makes fingerprint modules an indispensable component.

- BFSI (Banking, Financial Services, and Insurance): This sector is a key growth driver, with the increasing adoption of biometric authentication for mobile banking, secure transactions, and identity verification. The stringent security requirements of financial institutions necessitate reliable and advanced fingerprint solutions.

- Government: Governments worldwide are increasingly implementing biometric identification systems for national ID cards, border control, and secure access to public services. The demand for robust and tamper-proof fingerprint modules for these applications is substantial, with significant investment in secure identity management programs.

- Military and Defense: This sector demands the highest levels of security and reliability, making fingerprint modules crucial for access control to sensitive facilities and equipment, as well as for soldier identification.

Type Segment Dynamics:

- Capacitive: This technology continues to hold a significant market share due to its maturity, cost-effectiveness, and widespread adoption in mid-range to high-end consumer electronics.

- Optical: While still present, optical sensors are gradually losing market share to capacitive and ultrasonic technologies in premium segments, though they remain relevant in specific low-cost applications.

- Ultrasonic: This is the fastest-growing segment, driven by its superior performance characteristics and its ability to enable in-display fingerprint sensing, appealing to the demand for seamless device integration.

Europe Fingerprint Module Industry Product Developments

Product development in the Europe Fingerprint Module Industry is heavily focused on enhancing sensor performance, miniaturization, and seamless integration. Innovations include the development of ultra-thin, under-display capacitive and ultrasonic sensors that offer improved speed and accuracy, even with wet or dirty fingers. Companies are also concentrating on incorporating advanced anti-spoofing technologies to counter sophisticated attempts at biometric fraud. The integration of fingerprint modules with other biometric modalities and the development of AI-powered authentication algorithms are key competitive advantages being pursued. The trend towards lower power consumption is critical for battery-sensitive IoT devices.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Europe Fingerprint Module Industry, segmenting the market by Type, Application, and End-user Industry.

Type: The analysis covers Optical, Capacitive, Thermal, and Ultrasonic fingerprint modules. Capacitive sensors are expected to maintain a strong market presence due to their established performance and cost-effectiveness. However, Ultrasonic technology is projected to witness the highest growth rate, driven by its superior capabilities and adoption in premium devices. Thermal sensors, while niche, are being explored for specific industrial and medical applications. The market size for fingerprint modules is projected to grow significantly across all types, with Ultrasonic segments expected to contribute substantially to the overall market value of approximately 2.5 billion Euros by 2033.

Application: Key applications include Smartphones/Tablets, Laptops, Smartcards, and IoT and Other Applications. Smartphones/Tablets will continue to dominate the market share, with robust growth expected. The Laptops segment is experiencing steady expansion due to increasing enterprise security needs. Smartcards, though smaller, present a high-growth opportunity, particularly in secure payment and identity management. The IoT segment is poised for explosive growth, driven by the proliferation of connected devices across various sectors, with market penetration expected to exceed 45% by 2033.

End-user Industry: The report examines the Military and Defense, Consumer Electronics, BFSI, Government, and Other End-user Industries. Consumer Electronics will remain the largest segment, with substantial contributions from the smartphone and tablet markets. The BFSI sector is a significant growth catalyst, driven by the demand for secure digital banking and transaction authentication. Government applications, including national ID and border control, represent a stable and substantial demand. The Military and Defense sector requires high-performance, secure solutions, contributing to the demand for advanced technologies.

Key Drivers of Europe Fingerprint Module Industry Growth

The Europe Fingerprint Module Industry's growth is underpinned by several key drivers. Firstly, the relentless demand for enhanced security and data protection across both consumer and enterprise sectors is paramount. Secondly, the increasing proliferation of connected devices, particularly in the burgeoning IoT ecosystem, necessitates secure authentication solutions. Thirdly, advancements in biometric sensor technology, leading to improved accuracy, speed, and cost-effectiveness, are making fingerprint modules more accessible and desirable. Fourthly, government initiatives promoting digital identity and secure e-governance services are creating significant market opportunities. Finally, the growing consumer preference for convenience and seamless user experiences fuels the adoption of fingerprint authentication in everyday devices.

Challenges in the Europe Fingerprint Module Industry Sector

Despite its robust growth, the Europe Fingerprint Module Industry faces several challenges. Regulatory hurdles, particularly regarding data privacy and the handling of biometric information under GDPR, necessitate stringent compliance measures and can increase development costs. Supply chain disruptions, as witnessed in recent global events, can impact component availability and lead to price volatility. Intensifying competition from both established players and new entrants drives down profit margins. Furthermore, the emergence of alternative biometric technologies, such as advanced facial recognition and iris scanning, presents a competitive threat, especially in specific application segments. Overcoming these challenges requires continuous innovation, strategic partnerships, and agile supply chain management.

Emerging Opportunities in Europe Fingerprint Module Industry

Emerging opportunities in the Europe Fingerprint Module Industry are multifaceted. The rapid expansion of the Internet of Things (IoT) ecosystem, encompassing smart homes, wearables, and industrial automation, offers a vast untapped market for secure and integrated fingerprint sensors. The growing demand for contactless authentication solutions in a post-pandemic world presents opportunities for advanced, in-display, and potentially even remote fingerprint sensing technologies. The integration of fingerprint modules with payment systems, especially in emerging markets and for contactless payment devices, represents a significant growth avenue. Furthermore, the development of specialized fingerprint sensors for medical devices and healthcare applications, enabling secure patient data access and device authentication, is a promising niche.

Leading Players in the Europe Fingerprint Module Industry Market

- Next Biometrics Group ASA

- IDEMIA France SAS

- Jenetric GmbH

- Dermalog Identification Systems GmbH

- IDEX ASA

- Gemalto NV

- NuData Security

- Fingerprint Cards AB

- TDK Corporation

- Egis Technology Inc

Key Developments in Europe Fingerprint Module Industry Industry

- 2023 October: Fingerprint Cards AB announces a new generation of under-display capacitive sensors with enhanced performance and lower power consumption.

- 2024 January: IDEMIA France SAS partners with a leading automotive manufacturer to integrate advanced fingerprint authentication into vehicle access and ignition systems.

- 2024 March: Jenetric GmbH introduces an ultra-compact ultrasonic fingerprint module designed for secure access control in compact IoT devices.

- 2024 April: Next Biometrics Group ASA expands its portfolio with a focus on fingerprint solutions for industrial and military applications, emphasizing ruggedness and reliability.

- 2024 June: Dermalog Identification Systems GmbH secures a major contract for a national border control and citizen identification project, highlighting the growing government demand.

- 2024 September: Gemalto NV (now part of Thales) showcases innovative solutions for secure payment cards with integrated fingerprint sensors, enhancing transaction security.

- 2025 February: IDEX ASA unveils a flexible, large-area fingerprint sensor technology suitable for applications beyond traditional device surfaces.

- 2025 April: TDK Corporation announces advancements in its piezo-electric technology for next-generation ultrasonic fingerprint sensors, promising higher resolution and faster acquisition.

Strategic Outlook for Europe Fingerprint Module Industry Market

- 2023 October: Fingerprint Cards AB announces a new generation of under-display capacitive sensors with enhanced performance and lower power consumption.

- 2024 January: IDEMIA France SAS partners with a leading automotive manufacturer to integrate advanced fingerprint authentication into vehicle access and ignition systems.

- 2024 March: Jenetric GmbH introduces an ultra-compact ultrasonic fingerprint module designed for secure access control in compact IoT devices.

- 2024 April: Next Biometrics Group ASA expands its portfolio with a focus on fingerprint solutions for industrial and military applications, emphasizing ruggedness and reliability.

- 2024 June: Dermalog Identification Systems GmbH secures a major contract for a national border control and citizen identification project, highlighting the growing government demand.

- 2024 September: Gemalto NV (now part of Thales) showcases innovative solutions for secure payment cards with integrated fingerprint sensors, enhancing transaction security.

- 2025 February: IDEX ASA unveils a flexible, large-area fingerprint sensor technology suitable for applications beyond traditional device surfaces.

- 2025 April: TDK Corporation announces advancements in its piezo-electric technology for next-generation ultrasonic fingerprint sensors, promising higher resolution and faster acquisition.

Strategic Outlook for Europe Fingerprint Module Industry Market

The strategic outlook for the Europe Fingerprint Module Industry is overwhelmingly positive, driven by sustained demand for secure and convenient authentication. Future growth will be catalyzed by the ongoing technological evolution towards ultrasonic and in-display sensors, which will enable more seamless integration into next-generation devices. Expansion into the rapidly growing IoT market will unlock significant revenue streams. Strategic partnerships and collaborations between sensor manufacturers, device OEMs, and software providers will be crucial for delivering comprehensive security solutions. Furthermore, the increasing focus on cybersecurity regulations and data protection will continue to drive the adoption of reliable biometric technologies. The industry is well-positioned to capitalize on the global trend towards a more secure and digitally connected world.

Europe Fingerprint Module Industry Segmentation

-

1. Type

- 1.1. Optical

- 1.2. Capacitive

- 1.3. Thermal

- 1.4. Ultrasonic

-

2. Application

- 2.1. Smartphones/Tablets

- 2.2. Laptops

- 2.3. Smartcards

- 2.4. IoT and Other Applications

-

3. End-user Industry

- 3.1. Military and Defense

- 3.2. Consumer Electronics

- 3.3. BFSI

- 3.4. Government

- 3.5. Other End-user Industries

Europe Fingerprint Module Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Fingerprint Module Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 1.44% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Need for Secured Security and Business Applications

- 3.3. Market Restrains

- 3.3.1 ; Increase in Adoption of Substitute Technologies

- 3.3.2 Such as Face and Iris Scanning

- 3.4. Market Trends

- 3.4.1. BFSI Industry is Expected to Drive the Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Optical

- 5.1.2. Capacitive

- 5.1.3. Thermal

- 5.1.4. Ultrasonic

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Smartphones/Tablets

- 5.2.2. Laptops

- 5.2.3. Smartcards

- 5.2.4. IoT and Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Military and Defense

- 5.3.2. Consumer Electronics

- 5.3.3. BFSI

- 5.3.4. Government

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Fingerprint Module Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Next Biometrics Group ASA

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 IDEMIA France SAS

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Jenetric GmbH*List Not Exhaustive

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Dermalog Identification Systems GmbH

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 IDEX ASA

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Gemalto NV

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 NuData Security

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Fingerprint Cards AB

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 TDK Corporation

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Egis Technology Inc

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Next Biometrics Group ASA

List of Figures

- Figure 1: Europe Fingerprint Module Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Fingerprint Module Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Fingerprint Module Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Fingerprint Module Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Fingerprint Module Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Europe Fingerprint Module Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: Europe Fingerprint Module Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Fingerprint Module Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Fingerprint Module Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 15: Europe Fingerprint Module Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 16: Europe Fingerprint Module Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 17: Europe Fingerprint Module Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United Kingdom Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Germany Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Italy Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Spain Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Netherlands Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Belgium Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Sweden Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Norway Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Poland Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Denmark Europe Fingerprint Module Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Fingerprint Module Industry?

The projected CAGR is approximately 1.44%.

2. Which companies are prominent players in the Europe Fingerprint Module Industry?

Key companies in the market include Next Biometrics Group ASA, IDEMIA France SAS, Jenetric GmbH*List Not Exhaustive, Dermalog Identification Systems GmbH, IDEX ASA, Gemalto NV, NuData Security, Fingerprint Cards AB, TDK Corporation, Egis Technology Inc.

3. What are the main segments of the Europe Fingerprint Module Industry?

The market segments include Type, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Need for Secured Security and Business Applications.

6. What are the notable trends driving market growth?

BFSI Industry is Expected to Drive the Market Growth.

7. Are there any restraints impacting market growth?

; Increase in Adoption of Substitute Technologies. Such as Face and Iris Scanning.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Fingerprint Module Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Fingerprint Module Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Fingerprint Module Industry?

To stay informed about further developments, trends, and reports in the Europe Fingerprint Module Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence