Key Insights

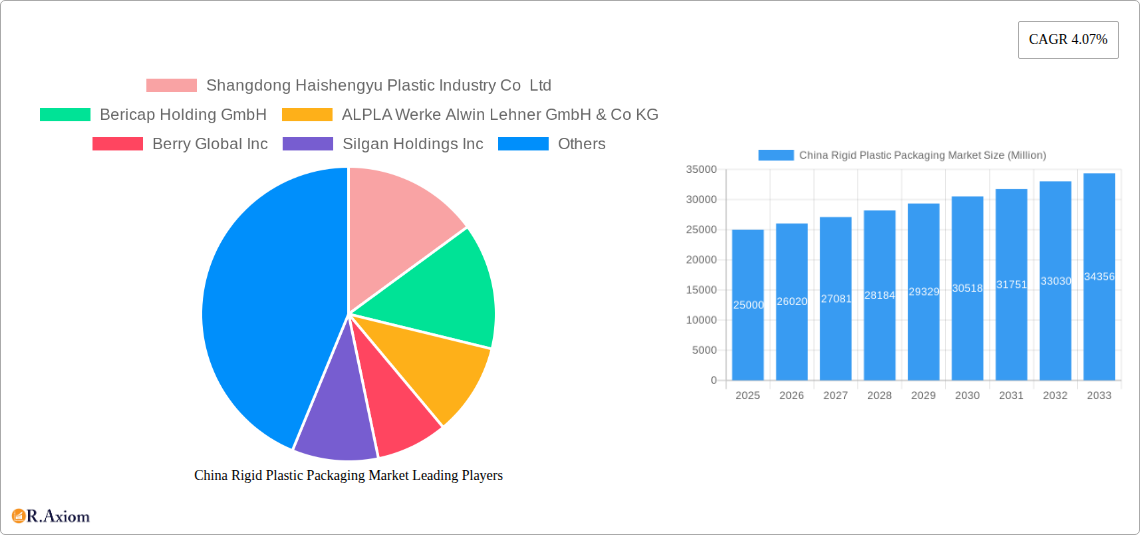

The China rigid plastic packaging market is poised for significant expansion, propelled by the nation's burgeoning consumer goods sector, with key segments including food & beverages, pharmaceuticals, and personal care. The market size is projected to reach $9.68 million in 2025, exhibiting a compound annual growth rate (CAGR) of 4.07%. This growth is underpinned by increasing disposable incomes, rapid urbanization, and a growing consumer preference for convenient, ready-to-consume products. The demand for lightweight, durable, and cost-effective packaging solutions further amplifies the market's potential. Technological advancements, such as the development of recyclable and biodegradable plastics, are influencing market dynamics, though challenges in widespread adoption and recycling infrastructure persist. Leading market participants, including Shandong Haishengyu Plastic Industry Co Ltd, Bericap Holding GmbH, and ALPLA Werke Alwin Lehner GmbH & Co KG, are prioritizing innovation and strategic collaborations to address evolving market demands.

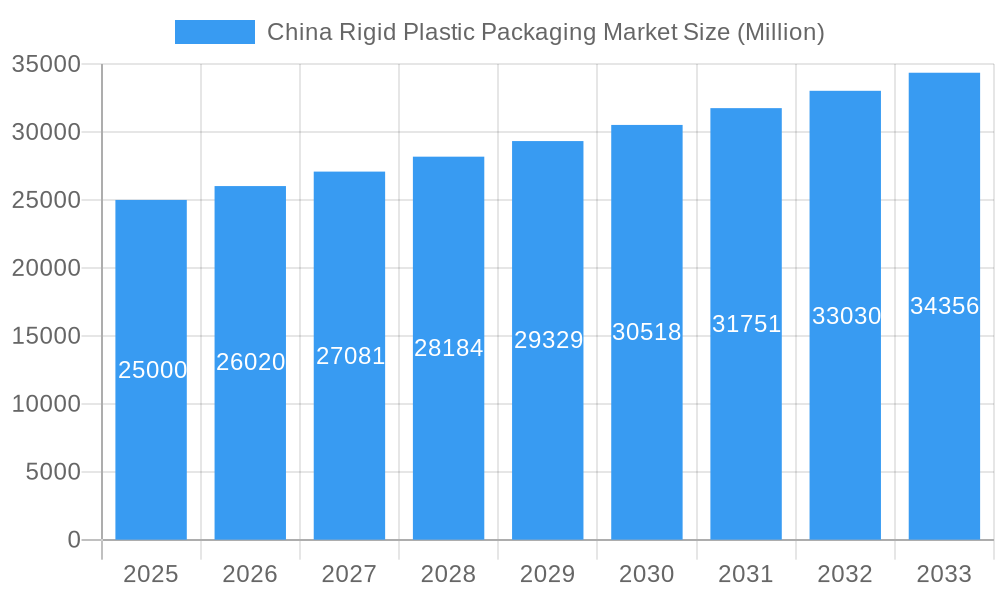

China Rigid Plastic Packaging Market Market Size (In Million)

Notwithstanding the positive outlook, the market encounters certain constraints. Stringent environmental regulations designed to curb plastic waste are compelling manufacturers to invest in sustainable packaging alternatives, potentially affecting short-term production costs. Volatility in raw material prices, particularly for petroleum-based plastics, presents another obstacle, compounded by rising competition from alternative materials such as paper and glass. Nevertheless, the long-term growth trajectory remains robust, driven by sustained expansion in the consumer goods sector and continuous innovation in sustainable rigid plastic packaging technologies. Market segmentation is expected to become more specialized, with tailored packaging solutions for specific product categories gaining traction. Growth is anticipated to be particularly pronounced in China's rapidly developing economic regions, further contributing to overall market expansion.

China Rigid Plastic Packaging Market Company Market Share

China Rigid Plastic Packaging Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the China Rigid Plastic Packaging market, offering valuable insights for industry stakeholders, investors, and strategic decision-makers. The study covers the period 2019-2033, with 2025 as the base year and a forecast period extending to 2033. The report leverages rigorous data analysis and market research methodologies to deliver actionable intelligence on market size, growth drivers, challenges, opportunities, and competitive dynamics. The report value is xx Million.

China Rigid Plastic Packaging Market Market Concentration & Innovation

The China rigid plastic packaging market exhibits a moderately concentrated landscape, with a few dominant players and numerous smaller, regional companies. Market share is constantly shifting due to mergers & acquisitions (M&A) activities and the emergence of innovative packaging solutions. In 2024, the top 5 players held approximately xx% of the market share. M&A activity has been significant, with deal values exceeding xx Million in the past five years, driven by the pursuit of economies of scale and expansion into new segments. Regulatory frameworks, including those concerning recyclability and sustainability, are significantly influencing innovation. Product substitutes, such as biodegradable alternatives, are gaining traction, posing a challenge to traditional rigid plastic packaging. End-user trends, particularly a growing preference for convenience and eco-friendly packaging, are driving demand for innovative materials and designs.

- Key Players Market Share (2024 Estimate): xx% (Top 5 Players)

- M&A Deal Value (2019-2024): Over xx Million

- Key Innovation Drivers: Sustainability concerns, e-commerce growth, and evolving consumer preferences.

- Regulatory Impact: Increasing focus on recyclability and reduction of plastic waste.

China Rigid Plastic Packaging Market Industry Trends & Insights

The China rigid plastic packaging market is experiencing dynamic growth and significant evolution. Projections indicate a robust Compound Annual Growth Rate (CAGR) of 6.5% to 7.5% between 2025 and 2033, underscoring its substantial expansion. This upward trajectory is propelled by a confluence of powerful economic and societal forces. Key among these are the persistent rise in disposable incomes, a burgeoning e-commerce sector that necessitates efficient and protective packaging, and the ever-increasing demand for safely packaged food and beverage products to meet the needs of a large and growing population. Furthermore, technological advancements are playing a pivotal role. The adoption of innovative lightweighting technologies is reducing material usage and transportation costs, while advancements in recycling processes and the development of more sustainable materials are addressing environmental concerns and appealing to eco-conscious consumers. Consumer preferences are demonstrably shifting, with a pronounced emphasis on sustainable, convenient, and aesthetically pleasing packaging solutions. This shift is directly influencing material choices, with a growing demand for recycled and bio-based plastics, as well as influencing product design to enhance user experience and recyclability. The competitive landscape is characterized by intense rivalry among established global and domestic players, alongside the strategic emergence of agile new entrants who are often at the forefront of offering novel product designs and specialized services. The market penetration of sustainable packaging materials is steadily increasing, with an anticipated market share of 30% to 35% by 2033, reflecting a significant move towards a circular economy.

Dominant Markets & Segments in China Rigid Plastic Packaging Market

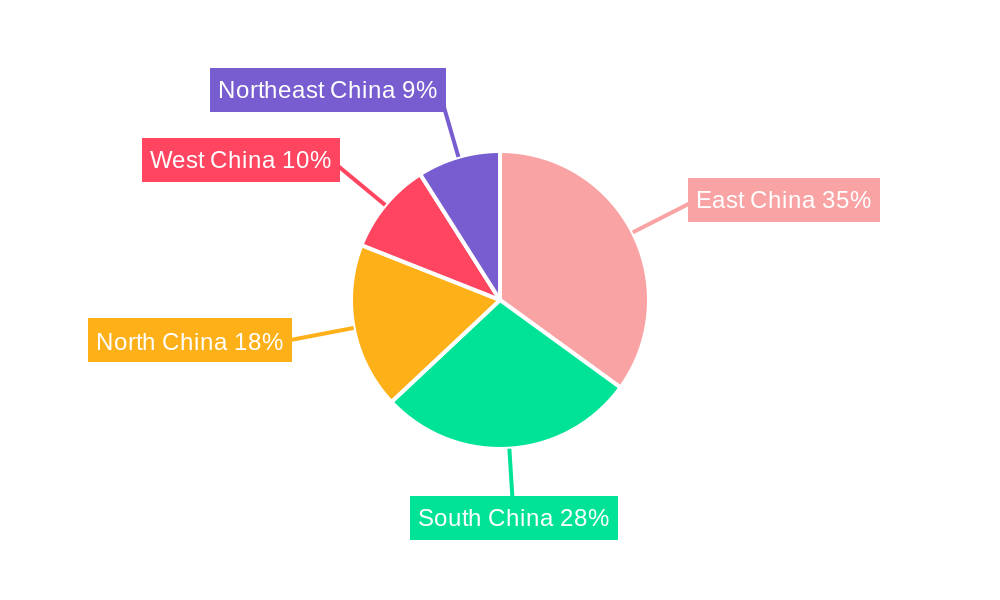

The coastal regions of China continue to be the epicenters of demand for rigid plastic packaging. Provinces such as Guangdong, Jiangsu, and Zhejiang stand out as the dominant markets. This dominance is intrinsically linked to their high population densities, thriving industrial bases that serve as both producers and consumers of packaged goods, and their well-developed infrastructure, particularly in logistics and transportation. These regions benefit from efficient supply chains, proximity to major urban consumption hubs, and a generally supportive economic and regulatory environment that fosters business growth and innovation in the packaging sector.

-

Key Drivers in Dominant Regions:

- Strong and diverse industrial base, encompassing manufacturing of consumer goods, food & beverages, and pharmaceuticals.

- Exceptional population density, leading to high per capita consumption of packaged products.

- Extensive and well-established logistics and transportation infrastructure, ensuring efficient distribution.

- Favorable government policies and economic zones that encourage investment and industrial development.

- High levels of consumer spending power and evolving lifestyle preferences.

- Dominance Analysis: The synergistic effect of concentrated manufacturing capabilities and significant consumption centers in these coastal regions creates a self-reinforcing cycle of demand for rigid plastic packaging solutions, solidifying their market dominance.

China Rigid Plastic Packaging Market Product Developments

Recent product innovations focus on lightweighting, enhanced barrier properties, and improved recyclability. Advances in materials science and manufacturing technologies have led to the development of more sustainable and functional packaging solutions. These innovations offer competitive advantages by meeting growing consumer demands for eco-friendly and convenient products. Examples include the increasing use of recycled PET (rPET) and the development of bio-based plastics.

Report Scope & Segmentation Analysis

This comprehensive report provides an in-depth analysis of the China rigid plastic packaging market, meticulously segmenting it to offer granular insights. The market is analyzed across key dimensions: material type (including PET, HDPE, PP, PVC, and other emerging materials), packaging type (encompassing bottles, containers, jars, tubs, closures, and other specialized formats), end-use industry (covering food and beverages, pharmaceuticals, cosmetics and personal care, household goods, industrial goods, and others), and by region. For each segment, the report delivers detailed growth projections, current market size estimations, and a thorough competitive landscape analysis. This granular approach enables stakeholders to identify specific growth opportunities, understand segment-specific dynamics, and formulate targeted strategies for success within the broader Chinese rigid plastic packaging market.

Key Drivers of China Rigid Plastic Packaging Market Growth

Several factors are driving the growth of the China rigid plastic packaging market. Firstly, the burgeoning e-commerce sector fuels demand for protective packaging. Secondly, rising disposable incomes increase consumer spending on packaged goods. Thirdly, government initiatives promoting industrial development stimulate production activities. Finally, technological advancements in packaging materials and manufacturing processes continuously enhance product functionality and sustainability.

Challenges in the China Rigid Plastic Packaging Market Sector

Despite its significant growth, the China rigid plastic packaging market navigates a complex landscape of challenges. The most prominent is the increasing stringency of environmental regulations pertaining to plastic waste management and reduction. The government's heightened focus on sustainability and circular economy principles necessitates greater investment in recycling infrastructure and the development of alternative, eco-friendlier materials. Fluctuations in the prices of key raw materials, such as crude oil derivatives, and ongoing global supply chain disruptions can significantly impact production costs, lead times, and overall profitability, requiring robust risk management strategies. The market is also characterized by intense competition, not only from established domestic and international players but also from emerging companies offering disruptive solutions. This necessitates continuous innovation, operational efficiency improvements, and aggressive cost optimization strategies to maintain market share and profitability. These collective challenges are estimated to impact market growth by a potential loss of USD 500-700 Million annually due to increased compliance costs, raw material volatility, and the need for strategic adaptation.

Emerging Opportunities in China Rigid Plastic Packaging Market

Significant opportunities exist within the China rigid plastic packaging market. The increasing demand for sustainable and eco-friendly packaging presents a significant opportunity for businesses offering recycled and bio-based solutions. Furthermore, the growth of the e-commerce sector presents opportunities for specialized packaging solutions designed to protect goods during transit. The development of new technologies focusing on improved recyclability and lightweighting will increase this market potential.

Leading Players in the China Rigid Plastic Packaging Market Market

- Shandong Haishengyu Plastic Industry Co., Ltd.

- Bericap Holding GmbH

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Berry Global Inc.

- Silgan Holdings Inc.

- Taizhou Huangyan Baitong Plastic Co., Ltd.

- Ningbo Kinpack Commodity Co., Ltd.

- PBM Plastic Co., Ltd.

- Gerresheimer AG

- Amcor Group GmbH

- AptarGroup, Inc.

- Wihuri Group (e.g., Wipak)

- RPC Group (now part of Berry Global)

Key Developments in China Rigid Plastic Packaging Market Industry

- April 2024: Coca-Cola launched 500ml bottles made from 100% recycled PET (rPET) sourced from its China facilities in Hong Kong. This highlights the growing adoption of recycled materials and circular economy principles.

- August 2024: ALPLA Werke Alwin Lehner GmbH & Co KG partnered with Zerooo to develop reusable PET packaging for personal care and cosmetics, reflecting the increasing focus on sustainable packaging solutions.

Strategic Outlook for China Rigid Plastic Packaging Market Market

The future of the China rigid plastic packaging market is bright, driven by continued economic growth, expanding consumption, and the increasing adoption of sustainable packaging solutions. Companies focusing on innovation, sustainability, and efficient supply chain management will be best positioned to capitalize on the growth opportunities within this dynamic market. The long-term outlook is positive, with a projected continued expansion into new markets and applications.

China Rigid Plastic Packaging Market Segmentation

-

1. Product Type

- 1.1. Bottles and Jars

- 1.2. Trays and Containers

- 1.3. Caps and Closures

- 1.4. Intermediate Bulk Containers (IBCs)

- 1.5. Drums

- 1.6. Pallets

- 1.7. Other Product Types

-

2. Material

-

2.1. Polyethylene (PE)

- 2.1.1. LDPE & LLDPE

- 2.1.2. HDPE

- 2.2. Polyethylene Terephthalate (PET)

- 2.3. Polypropylene (PP)

- 2.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 2.5. Polyvinyl Chloride (PVC)

- 2.6. Other Rigid Plastic Packaging Materials

-

2.1. Polyethylene (PE)

-

3. End-Use Industries

-

3.1. Food**

- 3.1.1. Candy & Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, and Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Food Products

-

3.2. Foodservice**

- 3.2.1. Quick Service Restaurants (QSRs)

- 3.2.2. Full-Service Restaurants (FSRs)

- 3.2.3. Coffee and Snack Outlets

- 3.2.4. Retail Establishments

- 3.2.5. Institutional

- 3.2.6. Hospitality

- 3.2.7. Other Foodservice End Uses

- 3.3. Beverage

- 3.4. Healthcare

- 3.5. Cosmetics and Personal Care

- 3.6. Industrial

- 3.7. Building and Construction

- 3.8. Automotive

- 3.9. Other En

-

3.1. Food**

China Rigid Plastic Packaging Market Segmentation By Geography

- 1. China

China Rigid Plastic Packaging Market Regional Market Share

Geographic Coverage of China Rigid Plastic Packaging Market

China Rigid Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.07% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Bottles and Jars

- 5.1.2. Trays and Containers

- 5.1.3. Caps and Closures

- 5.1.4. Intermediate Bulk Containers (IBCs)

- 5.1.5. Drums

- 5.1.6. Pallets

- 5.1.7. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Polyethylene (PE)

- 5.2.1.1. LDPE & LLDPE

- 5.2.1.2. HDPE

- 5.2.2. Polyethylene Terephthalate (PET)

- 5.2.3. Polypropylene (PP)

- 5.2.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 5.2.5. Polyvinyl Chloride (PVC)

- 5.2.6. Other Rigid Plastic Packaging Materials

- 5.2.1. Polyethylene (PE)

- 5.3. Market Analysis, Insights and Forecast - by End-Use Industries

- 5.3.1. Food**

- 5.3.1.1. Candy & Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, and Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Food Products

- 5.3.2. Foodservice**

- 5.3.2.1. Quick Service Restaurants (QSRs)

- 5.3.2.2. Full-Service Restaurants (FSRs)

- 5.3.2.3. Coffee and Snack Outlets

- 5.3.2.4. Retail Establishments

- 5.3.2.5. Institutional

- 5.3.2.6. Hospitality

- 5.3.2.7. Other Foodservice End Uses

- 5.3.3. Beverage

- 5.3.4. Healthcare

- 5.3.5. Cosmetics and Personal Care

- 5.3.6. Industrial

- 5.3.7. Building and Construction

- 5.3.8. Automotive

- 5.3.9. Other En

- 5.3.1. Food**

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. China Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Bottles and Jars

- 6.1.2. Trays and Containers

- 6.1.3. Caps and Closures

- 6.1.4. Intermediate Bulk Containers (IBCs)

- 6.1.5. Drums

- 6.1.6. Pallets

- 6.1.7. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Polyethylene (PE)

- 6.2.1.1. LDPE & LLDPE

- 6.2.1.2. HDPE

- 6.2.2. Polyethylene Terephthalate (PET)

- 6.2.3. Polypropylene (PP)

- 6.2.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 6.2.5. Polyvinyl Chloride (PVC)

- 6.2.6. Other Rigid Plastic Packaging Materials

- 6.2.1. Polyethylene (PE)

- 6.3. Market Analysis, Insights and Forecast - by End-Use Industries

- 6.3.1. Food**

- 6.3.1.1. Candy & Confectionery

- 6.3.1.2. Frozen Foods

- 6.3.1.3. Fresh Produce

- 6.3.1.4. Dairy Products

- 6.3.1.5. Dry Foods

- 6.3.1.6. Meat, Poultry, and Seafood

- 6.3.1.7. Pet Food

- 6.3.1.8. Other Food Products

- 6.3.2. Foodservice**

- 6.3.2.1. Quick Service Restaurants (QSRs)

- 6.3.2.2. Full-Service Restaurants (FSRs)

- 6.3.2.3. Coffee and Snack Outlets

- 6.3.2.4. Retail Establishments

- 6.3.2.5. Institutional

- 6.3.2.6. Hospitality

- 6.3.2.7. Other Foodservice End Uses

- 6.3.3. Beverage

- 6.3.4. Healthcare

- 6.3.5. Cosmetics and Personal Care

- 6.3.6. Industrial

- 6.3.7. Building and Construction

- 6.3.8. Automotive

- 6.3.9. Other En

- 6.3.1. Food**

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shangdong Haishengyu Plastic Industry Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bericap Holding GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 ALPLA Werke Alwin Lehner GmbH & Co KG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Berry Global Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Silgan Holdings Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Taizhou Huangyan Baitong Plastic Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ningbo Kinpack Commodity Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PBM Plastic Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Gerresheimer AG

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Amcor Group GmbH

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Aptar Group Inc 8 2 Heat Map Analysis8 3 Competitor Analysis - Emerging vs Established Player

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Shangdong Haishengyu Plastic Industry Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Rigid Plastic Packaging Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: China Rigid Plastic Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: China Rigid Plastic Packaging Market Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: China Rigid Plastic Packaging Market Revenue million Forecast, by Material 2020 & 2033

- Table 3: China Rigid Plastic Packaging Market Revenue million Forecast, by End-Use Industries 2020 & 2033

- Table 4: China Rigid Plastic Packaging Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: China Rigid Plastic Packaging Market Revenue million Forecast, by Product Type 2020 & 2033

- Table 6: China Rigid Plastic Packaging Market Revenue million Forecast, by Material 2020 & 2033

- Table 7: China Rigid Plastic Packaging Market Revenue million Forecast, by End-Use Industries 2020 & 2033

- Table 8: China Rigid Plastic Packaging Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Rigid Plastic Packaging Market?

The projected CAGR is approximately 4.07%.

2. Which companies are prominent players in the China Rigid Plastic Packaging Market?

Key companies in the market include Shangdong Haishengyu Plastic Industry Co Ltd, Bericap Holding GmbH, ALPLA Werke Alwin Lehner GmbH & Co KG, Berry Global Inc, Silgan Holdings Inc, Taizhou Huangyan Baitong Plastic Co Ltd, Ningbo Kinpack Commodity Co Ltd, PBM Plastic Co Ltd, Gerresheimer AG, Amcor Group GmbH, Aptar Group Inc 8 2 Heat Map Analysis8 3 Competitor Analysis - Emerging vs Established Player.

3. What are the main segments of the China Rigid Plastic Packaging Market?

The market segments include Product Type, Material, End-Use Industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.68 million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Premium Food and Beverage Products in the Country; Surge in Sustainable Product Innovations in the Market.

6. What are the notable trends driving market growth?

Food Segment Estimated to Have Significant Share in the Market.

7. Are there any restraints impacting market growth?

Rising Demand for Premium Food and Beverage Products in the Country; Surge in Sustainable Product Innovations in the Market.

8. Can you provide examples of recent developments in the market?

August 2024: ALPLA Werke Alwin Lehner GmbH & Co KG, an Austria-based company with operations in China, teamed up with Zerooo to create reusable PET packaging tailored for personal care and cosmetic products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Rigid Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Rigid Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Rigid Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the China Rigid Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence