Key Insights

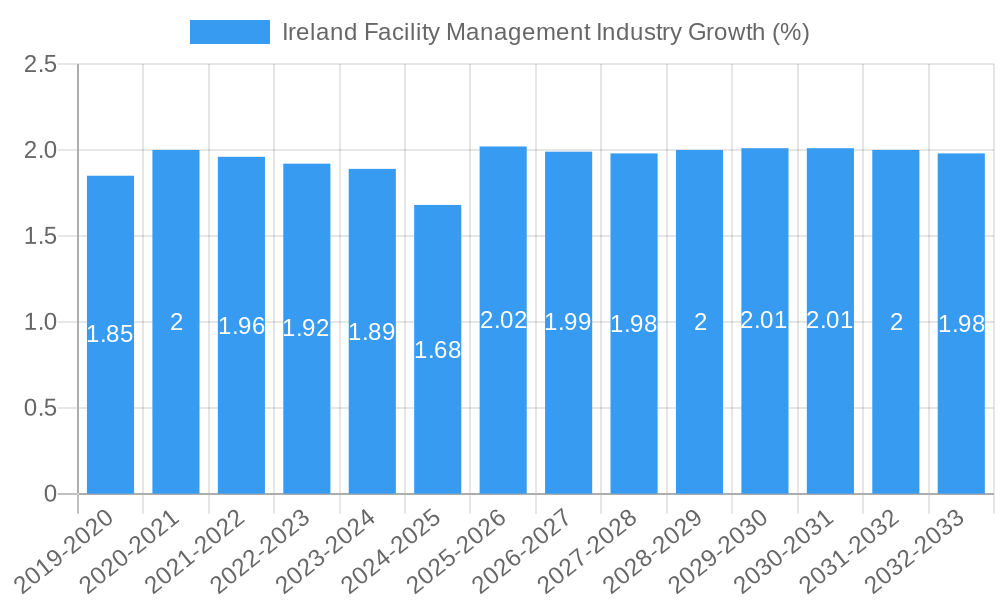

The Irish Facility Management (FM) industry is poised for steady expansion, with an estimated market size of €3.02 million in 2025, projecting a Compound Annual Growth Rate (CAGR) of 2.05% through 2033. This growth is underpinned by several key drivers. The increasing complexity of modern workplaces, coupled with a growing emphasis on operational efficiency and cost optimization, is compelling businesses across all sectors to adopt more sophisticated FM strategies. Furthermore, a heightened awareness of environmental, social, and governance (ESG) principles is driving demand for sustainable FM practices, including energy management, waste reduction, and resource optimization. The "smart building" revolution, integrating technology for enhanced building performance and occupant experience, is also a significant catalyst. Trends such as the rise of integrated FM solutions, offering a holistic approach to managing all facility aspects, and the increasing adoption of technology, including AI and IoT for predictive maintenance and real-time monitoring, are shaping the market landscape. The demand for both hard FM services (like maintenance and engineering) and soft FM services (such as cleaning, security, and catering) remains robust, catering to diverse end-user segments including commercial, institutional, public/infrastructure, and industrial sectors.

Despite the positive outlook, certain restraints are influencing the market's trajectory. A notable challenge is the shortage of skilled FM professionals, which can impact service quality and operational effectiveness. Additionally, the initial investment required for advanced FM technologies and the potential resistance to change within organizations can pose barriers to adoption. The evolving regulatory landscape, particularly concerning health, safety, and environmental standards, also necessitates continuous adaptation and investment from FM providers. However, the inherent value proposition of efficient facility management, which includes improved asset longevity, enhanced employee productivity, and reduced operational risks, continues to drive market penetration. The competitive landscape features both established global players and emerging local providers, fostering innovation and a drive for service excellence. The industry is characterized by a shift towards more outcome-based service delivery, where providers are increasingly measured by the tangible benefits they bring to their clients.

Ireland Facility Management Industry Market Concentration & Innovation

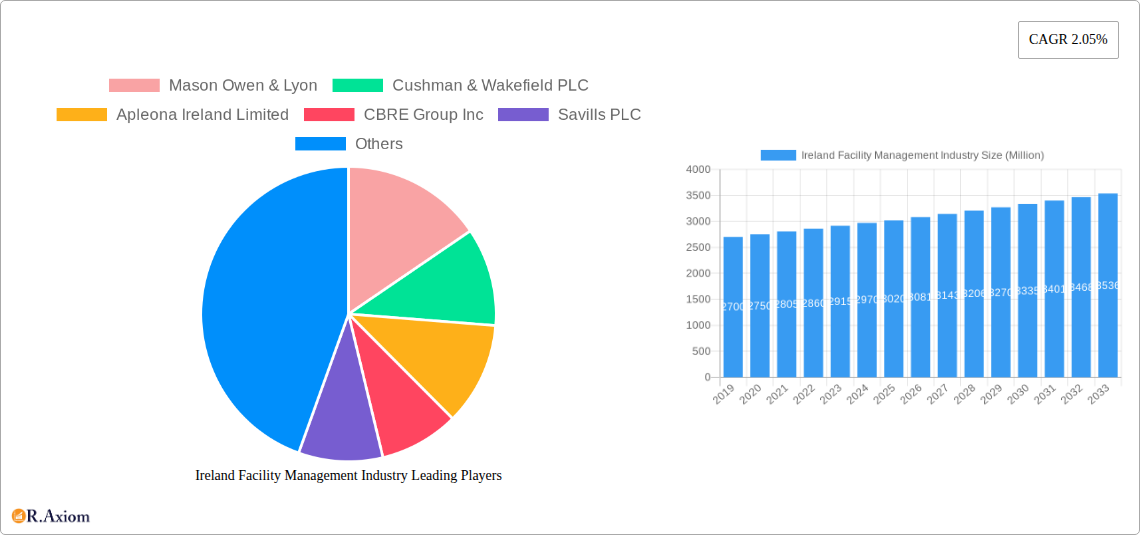

The Irish facility management market is characterized by a moderate level of concentration, with a few dominant players like CBRE Group Inc., Cushman & Wakefield PLC, and Savills PLC holding significant market share, estimated to be over 50 million. However, the presence of numerous smaller, specialized firms prevents complete market saturation. Innovation is a key differentiator, driven by the increasing adoption of smart building technologies, AI-powered predictive maintenance, and sustainable facility solutions. Regulatory frameworks, particularly concerning health, safety, and environmental standards, are robust and influence service delivery. Product substitutes, such as in-house management for certain functions or alternative service providers, exist but are often outcompeted by the efficiency and expertise of dedicated FM companies. End-user trends reveal a growing demand for integrated services, cost optimization, and enhanced employee experience. Mergers and acquisitions (M&A) activity is present, with deal values in the past three years estimated to be in the range of 50 million to 150 million, indicating strategic consolidation and expansion by larger entities.

- Market Share of Top Players: Estimated > 50 million

- M&A Deal Value (Past 3 Years): 50 million - 150 million

- Innovation Drivers: Smart building tech, AI, sustainability, digital transformation.

- Regulatory Influence: Health & Safety Executive (HSE) guidelines, environmental regulations.

Ireland Facility Management Industry Industry Trends & Insights

The Ireland facility management industry is poised for significant growth, projected to experience a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period of 2025-2033. This expansion is primarily fueled by increasing outsourcing trends across diverse end-user verticals, a burgeoning demand for specialized soft and hard facility management services, and the continuous integration of advanced technologies. The market penetration of outsourced facility management is steadily rising, as businesses recognize the cost efficiencies and operational benefits of entrusting these critical functions to expert providers. Technological disruptions, such as the implementation of the Internet of Things (IoT) for real-time monitoring and data analytics, Building Information Modeling (BIM) for lifecycle management, and robotic process automation for routine tasks, are reshaping service delivery models. Consumer preferences are shifting towards more personalized and sustainable FM solutions, emphasizing occupant well-being and environmental responsibility. Competitive dynamics are intensifying, with established players like Sodexo Group and Apleona Ireland Limited vying for market share against agile innovators. The evolving landscape also sees a growing emphasis on integrated facility management, where a single provider manages a comprehensive suite of services, optimizing coordination and enhancing service quality. The market size is projected to reach over 10,000 million by 2025.

- Projected CAGR (2025-2033): ~ 6.5%

- Estimated Market Size (2025): > 10,000 million

- Key Growth Drivers: Outsourcing, technological adoption, demand for sustainability.

- Technological Disruptions: IoT, BIM, AI, robotics.

- Consumer Preferences: Personalization, sustainability, occupant well-being.

- Competitive Landscape: Dominated by large players, with emerging niche providers.

Dominant Markets & Segments in Ireland Facility Management Industry

The Irish facility management industry exhibits clear dominance across several key segments, driven by distinct economic and operational factors. Within the Type segmentation, Outsourced Facility Management is the most prominent, encompassing a substantial portion of the market, estimated to be over 7,500 million by 2025. This dominance stems from businesses increasingly focusing on core competencies and leveraging the expertise and economies of scale offered by specialized FM providers. Within outsourced models, Integrated FM, which offers a holistic approach to managing all facility needs, is gaining significant traction due to its efficiency and streamlined operations, projected to grow at a CAGR of over 7% during the forecast period.

In terms of Offering Type, both Hard FM (e.g., building maintenance, HVAC, electrical) and Soft FM (e.g., cleaning, security, catering) command significant market share, with Hard FM estimated at over 4,000 million and Soft FM at over 6,000 million by 2025. However, the growth in Soft FM, particularly in areas like hygiene and security, is expected to outpace Hard FM due to heightened awareness and evolving regulatory demands.

The End-User segment analysis reveals that the Commercial sector is the largest consumer of facility management services, projected to reach over 5,000 million by 2025. This is attributed to the high density of office spaces, retail establishments, and corporate headquarters requiring comprehensive FM support. The Institutional sector, including healthcare and education, represents another substantial segment, driven by stringent compliance requirements and the need for specialized building services. Public/Infrastructure and Industrial segments also contribute significantly, with ongoing investment in infrastructure development and manufacturing facilities.

- Dominant Type: Outsourced Facility Management (> 7,500 million in 2025)

- Key Driver: Focus on core business, cost efficiency, access to expertise.

- Sub-segment Growth: Integrated FM experiencing rapid adoption (> 7% CAGR).

- Dominant Offering Type:

- Hard FM: Dominant in building upkeep and infrastructure maintenance (> 4,000 million in 2025).

- Soft FM: Experiencing higher growth due to increased demand for hygiene and security services (> 6,000 million in 2025).

- Key Drivers: Health & safety regulations, evolving workplace needs.

- Dominant End-User: Commercial Sector (> 5,000 million in 2025)

- Key Drivers: High concentration of office spaces, retail, and corporate presence.

- Other Significant End-Users: Institutional (healthcare, education), Public/Infrastructure, Industrial.

- Key Drivers: Compliance, essential service provision, infrastructure investment.

Ireland Facility Management Industry Product Developments

Recent product developments in the Irish facility management industry are heavily influenced by technological advancements and a drive towards sustainability. Innovations in smart building technology are enabling more efficient energy management and predictive maintenance, reducing operational costs and environmental impact. The integration of AI and IoT platforms allows for real-time data collection and analysis, leading to proactive issue resolution and optimized resource allocation. Furthermore, there's a growing emphasis on green FM solutions, with companies offering eco-friendly cleaning products, waste management strategies, and energy-efficient building retrofits. These developments provide competitive advantages by addressing client demands for cost savings, improved occupant comfort, and enhanced corporate social responsibility. The market fit for these innovations is strong, as businesses increasingly recognize the tangible benefits of modern facility management practices.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Ireland Facility Management Industry, covering the period from 2019 to 2033, with a base year of 2025. The market is segmented across several key dimensions to offer granular insights.

Type: The report examines both Inhouse Facility Management and Outsourced Facility Management. Within outsourced, it details Single FM, Bundled FM, and Integrated FM. Each segment's growth projections, market sizes, and competitive dynamics are analyzed. For instance, Integrated FM is projected to grow at a CAGR exceeding 7% due to its comprehensive service delivery, estimated to reach over 3,500 million by 2025.

Offering Type: The analysis includes Hard FM and Soft FM. Hard FM services are projected to reach over 4,000 million by 2025, driven by infrastructure upkeep, while Soft FM is expected to grow at a CAGR of approximately 6%, reaching over 6,000 million by 2025, fueled by hygiene and security demands.

End-User: The report segments the market by Commercial, Institutional, Public/Infrastructure, Industrial, and Other End-user Verticals. The Commercial sector is anticipated to dominate, with a market size exceeding 5,000 million by 2025, followed by Institutional and Public/Infrastructure segments.

Key Drivers of Ireland Facility Management Industry Growth

The growth of the Ireland facility management industry is propelled by several interconnected factors. Technologically, the widespread adoption of smart building solutions, IoT devices for real-time monitoring, and AI-powered analytics are optimizing operational efficiency and driving cost savings. Economically, increasing business outsourcing trends, particularly in sectors like IT and finance, allow companies to focus on core competencies, thereby expanding the demand for specialized FM services. Regulatory mandates concerning health, safety, and environmental standards also act as significant growth catalysts, compelling businesses to engage professional FM providers to ensure compliance. The ongoing infrastructure development across Ireland further fuels demand for robust facility management services.

- Technological Advancements: Smart building tech, IoT, AI for efficiency.

- Economic Factors: Business outsourcing, cost optimization focus.

- Regulatory Compliance: Health, safety, and environmental standards.

- Infrastructure Investment: Public and private sector projects.

Challenges in the Ireland Facility Management Industry Sector

Despite robust growth, the Ireland facility management sector faces several challenges. A significant restraint is the scarcity of skilled labor, particularly in specialized technical roles, leading to increased recruitment costs and potential service delivery delays. Regulatory hurdles, while driving demand, also impose compliance burdens and can escalate operational costs if not managed effectively. Supply chain disruptions, exacerbated by global economic volatility, can impact the availability and pricing of essential materials and equipment, affecting project timelines and budgets. Intense competitive pressures among a growing number of providers can lead to price wars, impacting profitability margins, estimated to be between 5%-10% for some services.

- Skilled Labor Shortage: Difficulty in recruiting and retaining qualified personnel.

- Regulatory Complexity: Evolving compliance requirements and associated costs.

- Supply Chain Volatility: Impact on material availability and pricing.

- Competitive Pressures: Price sensitivity and margin erosion.

Emerging Opportunities in Ireland Facility Management Industry

Emerging opportunities in the Irish facility management industry are abundant, driven by evolving client needs and technological innovation. The increasing focus on sustainability presents a significant opportunity for FM providers offering green building solutions, energy efficiency audits, and waste reduction programs. The growth of the data center sector in Ireland creates a demand for specialized FM services tailored to these critical infrastructure facilities. Furthermore, the rise of flexible working models necessitates adaptable workplace management solutions, including smart office technologies and enhanced occupant experience services. The development of niche service offerings, such as specialized cleaning for healthcare facilities or advanced security systems for sensitive industrial sites, also presents lucrative avenues for growth and market differentiation.

- Sustainability Services: Green FM, energy efficiency, waste management.

- Data Center FM: Specialized services for critical infrastructure.

- Flexible Workplace Solutions: Smart offices, occupant experience.

- Niche Service Development: Catering to specific industry needs.

Leading Players in the Ireland Facility Management Industry Market

- Mason Owen & Lyon

- Cushman & Wakefield PLC

- Apleona Ireland Limited

- CBRE Group Inc

- Savills PLC

- O'Brien Facilities Ltd

- Sodexo Group

- K-MAC Facilities Management Services

- Techcon International Ltd

- Kier Group PLC

- Elevare

- Manor Properties

- Neylons Facility Management Limited

- Sensori Facilities Management

Key Developments in Ireland Facility Management Industry Industry

- February 2023: Robinson Services partnered with FM Stores Ireland to enhance professional soft services in Ireland's commercial sectors, leveraging FM Stores' expertise in cleaning, hygiene, and safety.

- January 2023: Virgin Media O2 renewed and expanded its partnership with ISS Ireland, with ISS providing security, workplace services, and vital technological infrastructure maintenance.

Strategic Outlook for Ireland Facility Management Industry Market

The strategic outlook for the Ireland facility management industry remains exceptionally positive, with sustained growth anticipated. The market's trajectory is underpinned by the increasing adoption of integrated and technology-driven solutions, emphasizing efficiency, sustainability, and occupant well-being. Opportunities in specialized segments like data centers and green FM are set to expand significantly. Strategic partnerships and M&A activities will likely continue as key players consolidate their market positions and acquire new capabilities. Investment in talent development and advanced digital platforms will be crucial for maintaining a competitive edge. The industry is well-positioned to capitalize on Ireland's economic growth and evolving business landscape, ensuring a robust and dynamic future.

Ireland Facility Management Industry Segmentation

-

1. Type

- 1.1. Inhouse Facility Management

-

1.2. Outsourced Facility Management

- 1.2.1. Single FM

- 1.2.2. Bundled FM

- 1.2.3. Integrated FM

-

2. Offering Type

- 2.1. Hard FM

- 2.2. Soft FM

-

3. End-User

- 3.1. Commercial

- 3.2. Institutional

- 3.3. Public/Infrastructure

- 3.4. Industrial

- 3.5. Other End-user Verticals

Ireland Facility Management Industry Segmentation By Geography

- 1. Ireland

Ireland Facility Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.05% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Growing Construction Sector; Increasing Focus on Industry 4.0

- 3.2.2 Leading to More Manufacturing Facilities

- 3.3. Market Restrains

- 3.3.1. Diminishing Profit Margins And Ongoing Changes In Macro-environment

- 3.4. Market Trends

- 3.4.1. Growing Construction Sector Drives the Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Ireland Facility Management Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Inhouse Facility Management

- 5.1.2. Outsourced Facility Management

- 5.1.2.1. Single FM

- 5.1.2.2. Bundled FM

- 5.1.2.3. Integrated FM

- 5.2. Market Analysis, Insights and Forecast - by Offering Type

- 5.2.1. Hard FM

- 5.2.2. Soft FM

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Commercial

- 5.3.2. Institutional

- 5.3.3. Public/Infrastructure

- 5.3.4. Industrial

- 5.3.5. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Ireland

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Mason Owen & Lyon

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Cushman & Wakefield PLC

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Apleona Ireland Limited

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 CBRE Group Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Savills PLC

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 O'Brien Facilities Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Sodexo Group

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 K-MAC Facilities Management Services

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Techcon International Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Kier Group PLC

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Elevare

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Manor Properties

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Neylons Facility Management Limited

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Sensori Facilities Management

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.1 Mason Owen & Lyon

List of Figures

- Figure 1: Ireland Facility Management Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Ireland Facility Management Industry Share (%) by Company 2024

List of Tables

- Table 1: Ireland Facility Management Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Ireland Facility Management Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Ireland Facility Management Industry Revenue Million Forecast, by Offering Type 2019 & 2032

- Table 4: Ireland Facility Management Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 5: Ireland Facility Management Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Ireland Facility Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Ireland Facility Management Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 8: Ireland Facility Management Industry Revenue Million Forecast, by Offering Type 2019 & 2032

- Table 9: Ireland Facility Management Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 10: Ireland Facility Management Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ireland Facility Management Industry?

The projected CAGR is approximately 2.05%.

2. Which companies are prominent players in the Ireland Facility Management Industry?

Key companies in the market include Mason Owen & Lyon, Cushman & Wakefield PLC, Apleona Ireland Limited, CBRE Group Inc, Savills PLC, O'Brien Facilities Ltd, Sodexo Group, K-MAC Facilities Management Services, Techcon International Ltd, Kier Group PLC, Elevare, Manor Properties, Neylons Facility Management Limited, Sensori Facilities Management.

3. What are the main segments of the Ireland Facility Management Industry?

The market segments include Type, Offering Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Construction Sector; Increasing Focus on Industry 4.0. Leading to More Manufacturing Facilities.

6. What are the notable trends driving market growth?

Growing Construction Sector Drives the Market Growth.

7. Are there any restraints impacting market growth?

Diminishing Profit Margins And Ongoing Changes In Macro-environment.

8. Can you provide examples of recent developments in the market?

February 2023: Robinson Services, one of Northern Ireland's major service providers in the support services sector, partnered with FM Stores Ireland, a company with expertise in cleaning, hygiene, and safety services. This partnership would enable Robinson Services to provide many professional FM soft services in Ireland's commercial sectors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ireland Facility Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ireland Facility Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ireland Facility Management Industry?

To stay informed about further developments, trends, and reports in the Ireland Facility Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence