Key Insights

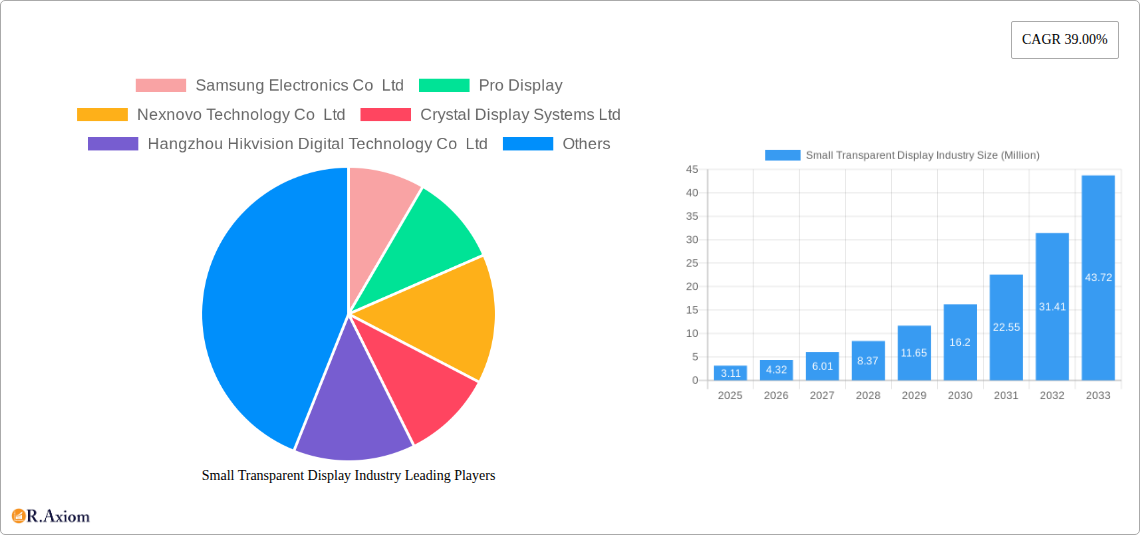

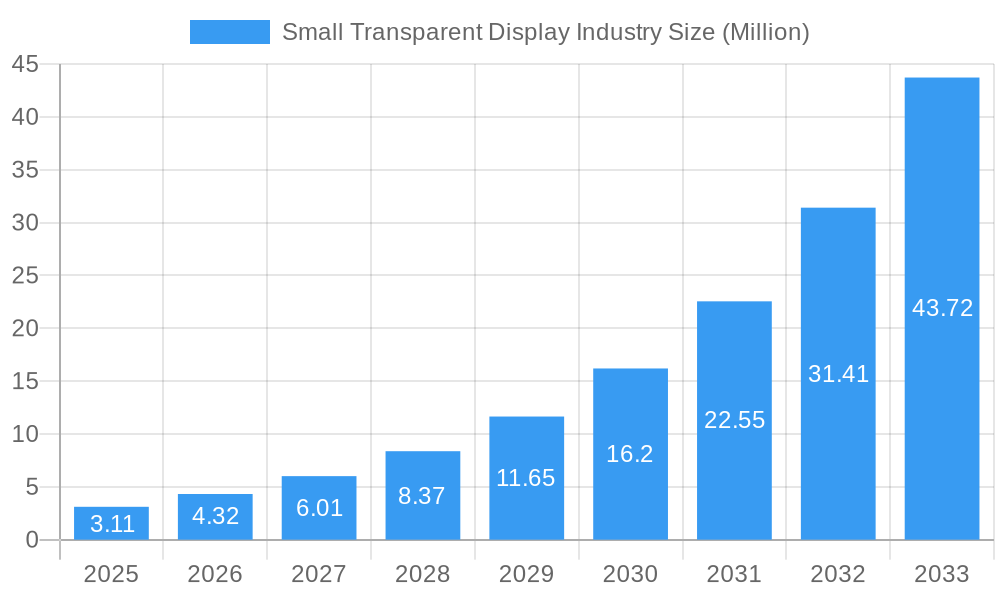

The global Small Transparent Display market is poised for explosive growth, projected to reach a substantial USD 3.11 million by 2025 and then surge forward with an exceptional Compound Annual Growth Rate (CAGR) of 39.00% through 2033. This remarkable expansion is fueled by a confluence of compelling market drivers, including the increasing demand for immersive and interactive user experiences across various sectors, advancements in display technologies such as OLED and micro-LED which offer superior clarity and energy efficiency, and the growing adoption of smart technologies in everyday applications. The integration of transparent displays into retail environments for dynamic advertising and product information, consumer electronics for innovative device designs, and the automotive industry for advanced heads-up displays and augmented reality interfaces are key growth areas. Furthermore, the aerospace and defense sector's requirement for advanced situational awareness tools also contributes significantly to this upward trajectory. The market's inherent ability to blend digital information seamlessly with the real world unlocks unprecedented opportunities for engagement and functionality.

Small Transparent Display Industry Market Size (In Million)

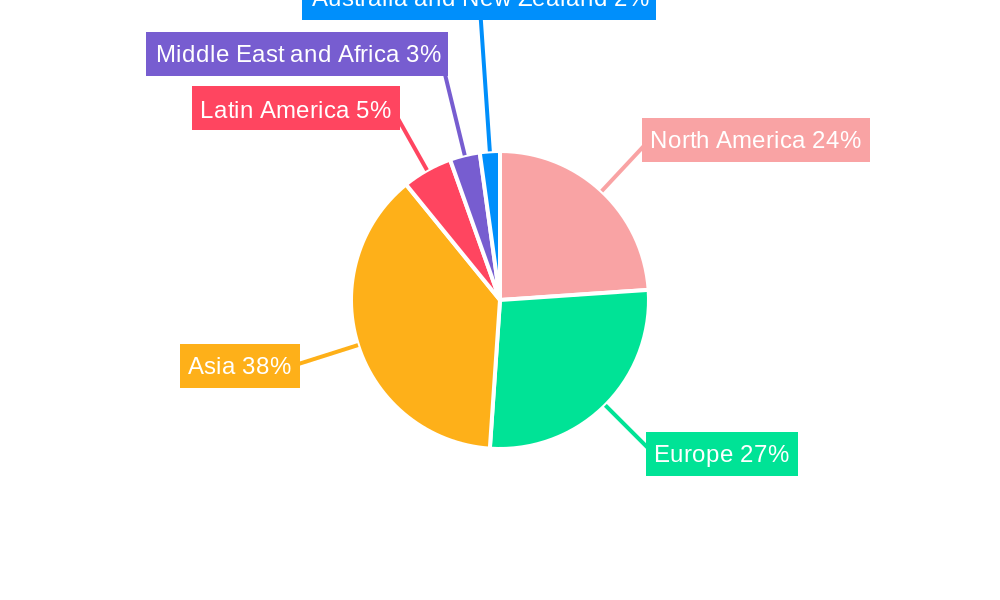

Despite the overwhelmingly positive outlook, certain restraints warrant consideration. High manufacturing costs associated with sophisticated transparent display technologies, coupled with challenges in achieving widespread product standardization, could temper the pace of adoption in some segments. Nevertheless, ongoing research and development efforts aimed at cost reduction and technological refinement are expected to mitigate these challenges over the forecast period. Emerging trends such as the integration of touch functionalities, the development of flexible and rollable transparent displays, and the increasing use of AI for personalized content delivery on these displays will further accelerate market penetration. The Asia-Pacific region, led by China and South Korea, is expected to dominate the market due to its robust manufacturing capabilities and significant investments in display technology innovation. North America and Europe are also anticipated to witness substantial growth driven by advanced technological adoption and increasing consumer demand for novel electronic products.

Small Transparent Display Industry Company Market Share

Small Transparent Display Industry Market Insights and Forecast: 2019–2033

This comprehensive report delivers an in-depth analysis of the Small Transparent Display Industry, providing critical market intelligence for stakeholders from 2019 to 2033. With a base year of 2025 and a forecast period spanning 2025–2033, this study offers actionable insights into market dynamics, technological advancements, and competitive landscapes. Explore the burgeoning demand for transparent display solutions across diverse applications and uncover the key growth drivers and emerging opportunities within this dynamic sector.

Small Transparent Display Industry Market Concentration & Innovation

The Small Transparent Display Industry exhibits a moderate market concentration, with key players like Samsung Electronics Co Ltd, LG Electronics Co Ltd, and BOE Technology Group holding significant market shares, estimated to be around XX% in the base year 2025. Innovation is a primary driver, fueled by ongoing research and development in materials science and display manufacturing. The development of higher transparency, improved brightness, and increased resolution are critical areas of focus. Regulatory frameworks are still evolving, with a focus on safety standards and energy efficiency in certain regions. Product substitutes, such as traditional opaque displays and augmented reality solutions, present a competitive challenge, necessitating continuous product differentiation. End-user trends are leaning towards immersive and interactive experiences, driving demand for transparent displays in retail, automotive, and consumer electronics. Mergers and acquisitions are expected to increase as companies seek to consolidate market positions and acquire innovative technologies. Anticipated M&A deal values are projected to reach approximately $XX million during the forecast period.

- Market Share of Key Players (2025): Samsung Electronics Co Ltd (XX%), LG Electronics Co Ltd (XX%), BOE Technology Group (XX%).

- Innovation Focus: Enhanced transparency, brightness, resolution, and interactivity.

- Key End-User Trends: Immersive experiences, smart surfaces, augmented reality integration.

- M&A Activity: Expected to rise with an estimated deal value of $XX million.

Small Transparent Display Industry Industry Trends & Insights

The Small Transparent Display Industry is poised for robust growth, driven by a confluence of technological advancements and evolving consumer preferences. The Compound Annual Growth Rate (CAGR) for the forecast period 2025–2033 is estimated at an impressive XX%, reflecting the expanding adoption of transparent display technologies across various sectors. A significant market penetration is anticipated as display manufacturers overcome existing technical challenges and scale production. The increasing demand for interactive and aesthetically pleasing display solutions in retail environments, for point-of-sale information, product showcases, and engaging customer experiences, is a major growth catalyst. In the consumer electronics segment, transparent displays are revolutionizing product design, enabling sleek and futuristic interfaces in devices ranging from smartphones to home appliances. The automotive industry is actively exploring transparent displays for heads-up displays (HUDs), augmented reality windshields, and interactive dashboards, promising enhanced safety and driving experiences. Technological disruptions, such as the advancement of OLED and MicroLED technologies, are enabling higher transparency levels, improved color reproduction, and greater energy efficiency, making transparent displays more viable and attractive for a wider array of applications. Furthermore, the integration of touch capabilities and advanced connectivity features is enhancing the functionality and appeal of these displays, pushing the boundaries of interactive technology. The competitive dynamics within the industry are intensifying, with established players investing heavily in R&D to maintain their market leadership and new entrants aiming to capture niche segments with specialized transparent display solutions. The overall market trajectory suggests a sustained upward trend, propelled by continuous innovation and a growing recognition of the unique value proposition offered by small transparent displays.

- Estimated CAGR (2025–2033): XX%

- Key Growth Sectors: Retail, Consumer Electronics, Automotive.

- Technological Advancements: OLED, MicroLED, touch integration, enhanced connectivity.

- Competitive Landscape: Intense R&D investment and emergence of specialized players.

Dominant Markets & Segments in Small Transparent Display Industry

The Small Transparent Display Industry is experiencing significant growth, with North America and Asia Pacific emerging as dominant markets. North America's dominance is fueled by early adoption in the retail and automotive sectors, driven by high disposable incomes and a strong appetite for innovative technologies. Countries like the United States and Canada are leading the charge, supported by robust research and development infrastructure and significant investment from leading companies. Asia Pacific, particularly China and South Korea, is a major manufacturing hub and a rapidly growing consumer market, contributing substantially to market expansion. The Automotive end-user industry is projected to witness the highest growth in this segment, driven by the increasing integration of advanced driver-assistance systems (ADAS) and the development of smart vehicle cockpits. The demand for transparent displays in automotive applications, such as augmented reality HUDs and interactive infotainment systems, is escalating due to enhanced safety features and improved user experiences. The Retail sector also represents a significant segment, with businesses leveraging transparent displays for digital signage, interactive product showcases, and enhanced in-store customer engagement. Countries with strong retail sectors and a focus on experiential marketing are expected to lead this adoption.

Technologically, OLED displays are expected to dominate the transparent display market due to their inherent advantages, including self-emissive pixels, superior contrast ratios, and flexible form factors, enabling higher transparency and slimmer designs. While LCD technology also plays a role, particularly in cost-sensitive applications, the advancements in OLED are pushing its market penetration higher.

- Dominant Regions: North America, Asia Pacific.

- Leading Countries: United States, Canada, China, South Korea.

- Dominant End-User Industry: Automotive.

- Key Drivers: ADAS integration, AR HUDs, interactive infotainment.

- Economic Policies: Government incentives for automotive innovation.

- Infrastructure: Investment in smart city initiatives.

- Significant End-User Industry: Retail.

- Key Drivers: Digital signage, interactive product displays, customer engagement.

- Consumer Preferences: Demand for personalized and engaging retail experiences.

- Dominant Technology: OLED.

- Key Drivers: High transparency, superior contrast, flexible form factors.

- Technological Advancements: Improved manufacturing processes for OLED.

Small Transparent Display Industry Product Developments

Recent product developments in the Small Transparent Display Industry highlight a clear focus on enhanced performance and expanded application possibilities. Innovations are centered around achieving higher transparency levels exceeding 70%, greater brightness (e.g., 800 nits), and increased resolutions (e.g., 114 PPI) to deliver vivid and clear visual experiences. Companies are pushing the boundaries of display technology with prototypes like the 8.75” transparent microLED panel unveiled at Display Week 2023, specifically targeting the automotive sector. Furthermore, the exhibition of diverse transparent digital displays, including large pixel pitch LED films, 55-inch transparent OLED panels, and touch-enabled translucent OLED panels in 50-inch and 30-inch sizes, demonstrates a commitment to catering to various creative and business needs, offering endless possibilities for businesses, interior designers, and content creators. These advancements are crucial for unlocking the full potential of transparent displays in interactive signage, augmented reality applications, and futuristic product designs.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Small Transparent Display Industry, segmenting the market by Technology and End-user Industry. The Technology segmentation includes LCD, OLED, and Other Technologies, with OLED projected to hold the largest market share due to its superior performance characteristics. The End-user Industry segmentation encompasses Retail, Consumer Electronics, Automotive, Aerospace and Defense, and Other End-user Industries. The Automotive sector is anticipated to exhibit the highest growth rate, driven by the increasing demand for advanced in-car displays and augmented reality solutions. The Retail sector follows closely, leveraging transparent displays for immersive customer experiences. Growth projections and market sizes will be detailed for each segment, providing a granular understanding of the market landscape and competitive dynamics within each.

- Technology Segmentation: LCD, OLED, Other Technologies.

- End-user Industry Segmentation: Retail, Consumer Electronics, Automotive, Aerospace and Defense, Other End-user Industries.

- Growth Projections: Detailed for each technology and end-user segment.

Key Drivers of Small Transparent Display Industry Growth

Several key factors are driving the growth of the Small Transparent Display Industry. Technologically, advancements in OLED and MicroLED technologies are enabling higher transparency, superior brightness, and enhanced color accuracy, making these displays more practical and appealing for a wider range of applications. Economically, increasing disposable incomes and a growing demand for premium and innovative consumer electronics and automotive features are fueling adoption. Government initiatives promoting smart city development and digital transformation are also indirectly boosting the demand for transparent display solutions in public spaces and infrastructure. Furthermore, the evolving consumer preference for interactive and aesthetically integrated display solutions is a significant driver, particularly in the retail and hospitality sectors.

- Technological Advancements: OLED, MicroLED improvements.

- Economic Factors: Rising disposable incomes, demand for premium products.

- Regulatory Factors: Smart city initiatives, digital transformation policies.

- Consumer Preferences: Demand for interactive and aesthetic displays.

Challenges in the Small Transparent Display Industry Sector

Despite its promising growth trajectory, the Small Transparent Display Industry faces several challenges. High manufacturing costs associated with advanced transparent display technologies, particularly OLED and MicroLED, can hinder mass adoption, especially in price-sensitive markets. Achieving true transparency while maintaining high brightness and color fidelity remains a technical hurdle for some applications. The supply chain for specialized components and materials is still developing, which can lead to production bottlenecks and increased lead times. Additionally, the lack of standardized protocols and integration challenges when implementing transparent displays into existing systems can pose a barrier to widespread deployment. Lastly, the competitive pressure from established opaque display technologies and emerging augmented reality solutions necessitates continuous innovation and cost optimization.

- Manufacturing Costs: High production expenses for advanced technologies.

- Technical Hurdles: Achieving optimal transparency and brightness balance.

- Supply Chain Limitations: Developing and scaling specialized component production.

- Integration Challenges: Interoperability with existing systems.

- Competitive Pressures: From opaque displays and AR solutions.

Emerging Opportunities in Small Transparent Display Industry

The Small Transparent Display Industry is rife with emerging opportunities. The automotive sector presents a significant growth avenue with the increasing demand for augmented reality head-up displays (AR-HUDs), transparent infotainment systems, and smart windows. In the retail space, transparent displays offer unique opportunities for interactive product visualization, personalized advertising, and enhancing store aesthetics. The consumer electronics industry is exploring their integration into smartphones, wearables, and home appliances for a futuristic user interface. Furthermore, the aerospace and defense sectors are investigating transparent displays for cockpits and heads-up displays, offering enhanced situational awareness. The development of more energy-efficient and cost-effective manufacturing processes will further unlock new market segments and applications, including smart furniture and architectural integration.

- Automotive: AR-HUDs, transparent infotainment, smart windows.

- Retail: Interactive product visualization, personalized advertising.

- Consumer Electronics: Futuristic interfaces in devices.

- Aerospace and Defense: Cockpit displays, heads-up displays.

- New Markets: Smart furniture, architectural integration.

Leading Players in the Small Transparent Display Industry Market

- Samsung Electronics Co Ltd

- Pro Display

- Nexnovo Technology Co Ltd

- Crystal Display Systems Ltd

- Hangzhou Hikvision Digital Technology Co Ltd

- Planar Systems Inc (Leyard Optoelectronic Co )

- Shenzhen AuroLED Technology Co Ltd

- BOE Technology Group

- LG Electronics Co Ltd

- Panasonic Corporation

- 2Point0 Concepts

Key Developments in Small Transparent Display Industry Industry

- Jul 2023: Tianma unveiled the latest transparent microLED display prototypes demonstrated at Display Week 2023. The company claims that the automotive sector is the primary application for these displays. The first display is an 8.75” (114 PPI) panel with an 880x480 resolution, 800 nits brightness, and more than 70% transparency.

- Jun 2023: LG Business Solutions USA exhibited its unique transparent digital displays at InfoComm 2023. LED films with a large pixel pitch, an OLED display with a 55-inch transparent panel, and transparent OLED touch displays with 50-inch and 30-inch translucent panels are formed in the lineup. With these innovative displays, businesses, interior designers, and content creators have endless creative possibilities.

Strategic Outlook for Small Transparent Display Industry Market

The Small Transparent Display Industry is set for significant expansion, driven by relentless innovation and a growing demand for immersive and integrated display solutions. Strategic focus on advancing OLED and MicroLED technologies to achieve higher transparency, brightness, and energy efficiency will be crucial. Partnerships between display manufacturers and end-user industries, particularly automotive and retail, will accelerate product development and market penetration. Investment in scaling production capabilities and optimizing manufacturing processes will address cost barriers and enhance market accessibility. The development of specialized transparent display solutions tailored to niche applications in aerospace, defense, and architecture presents further growth catalysts. The industry's future lies in its ability to seamlessly blend digital information with the physical world, creating intuitive and engaging user experiences.

Small Transparent Display Industry Segmentation

-

1. Technology

- 1.1. LCD

- 1.2. OLED

- 1.3. Other Technologies

-

2. End-user Industry

- 2.1. Retail

- 2.2. Consumer Electronics

- 2.3. Automotive

- 2.4. Aerospace and Defense

- 2.5. Other End-user Industries

Small Transparent Display Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

-

3. Asia

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Australia and New Zealand

- 4. Latin America

- 5. Middle East and Africa

Small Transparent Display Industry Regional Market Share

Geographic Coverage of Small Transparent Display Industry

Small Transparent Display Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 39.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. LCD

- 5.1.2. OLED

- 5.1.3. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Consumer Electronics

- 5.2.3. Automotive

- 5.2.4. Aerospace and Defense

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Small Transparent Display Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. LCD

- 6.1.2. OLED

- 6.1.3. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Consumer Electronics

- 6.2.3. Automotive

- 6.2.4. Aerospace and Defense

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Small Transparent Display Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. LCD

- 7.1.2. OLED

- 7.1.3. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Retail

- 7.2.2. Consumer Electronics

- 7.2.3. Automotive

- 7.2.4. Aerospace and Defense

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Small Transparent Display Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. LCD

- 8.1.2. OLED

- 8.1.3. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Retail

- 8.2.2. Consumer Electronics

- 8.2.3. Automotive

- 8.2.4. Aerospace and Defense

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Small Transparent Display Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. LCD

- 9.1.2. OLED

- 9.1.3. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Retail

- 9.2.2. Consumer Electronics

- 9.2.3. Automotive

- 9.2.4. Aerospace and Defense

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Latin America Small Transparent Display Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. LCD

- 10.1.2. OLED

- 10.1.3. Other Technologies

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Retail

- 10.2.2. Consumer Electronics

- 10.2.3. Automotive

- 10.2.4. Aerospace and Defense

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Middle East and Africa Small Transparent Display Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. LCD

- 11.1.2. OLED

- 11.1.3. Other Technologies

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Retail

- 11.2.2. Consumer Electronics

- 11.2.3. Automotive

- 11.2.4. Aerospace and Defense

- 11.2.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Samsung Electronics Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Pro Display

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Nexnovo Technology Co Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Crystal Display Systems Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Hangzhou Hikvision Digital Technology Co Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Planar Systems Inc (Leyard Optoelectronic Co )

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Shenzhen AuroLED Technology Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 BOE Technology Grou

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LG Electronics Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Panasonic Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 2Point0 Concepts

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Samsung Electronics Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Small Transparent Display Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Small Transparent Display Industry Revenue (Million), by Technology 2025 & 2033

- Figure 3: North America Small Transparent Display Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Small Transparent Display Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 5: North America Small Transparent Display Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Small Transparent Display Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Small Transparent Display Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Small Transparent Display Industry Revenue (Million), by Technology 2025 & 2033

- Figure 9: Europe Small Transparent Display Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Europe Small Transparent Display Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 11: Europe Small Transparent Display Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Small Transparent Display Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Small Transparent Display Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Small Transparent Display Industry Revenue (Million), by Technology 2025 & 2033

- Figure 15: Asia Small Transparent Display Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Asia Small Transparent Display Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: Asia Small Transparent Display Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Small Transparent Display Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Small Transparent Display Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Small Transparent Display Industry Revenue (Million), by Technology 2025 & 2033

- Figure 21: Latin America Small Transparent Display Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Latin America Small Transparent Display Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Latin America Small Transparent Display Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America Small Transparent Display Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Small Transparent Display Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Small Transparent Display Industry Revenue (Million), by Technology 2025 & 2033

- Figure 27: Middle East and Africa Small Transparent Display Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Middle East and Africa Small Transparent Display Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Small Transparent Display Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Small Transparent Display Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Small Transparent Display Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Small Transparent Display Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 2: Global Small Transparent Display Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Small Transparent Display Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Small Transparent Display Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 5: Global Small Transparent Display Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Small Transparent Display Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Small Transparent Display Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 10: Global Small Transparent Display Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Small Transparent Display Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Germany Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: France Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Global Small Transparent Display Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 16: Global Small Transparent Display Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 17: Global Small Transparent Display Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: China Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Japan Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: India Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: South Korea Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Australia and New Zealand Small Transparent Display Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Global Small Transparent Display Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 24: Global Small Transparent Display Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 25: Global Small Transparent Display Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Small Transparent Display Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 27: Global Small Transparent Display Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Small Transparent Display Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Small Transparent Display Industry?

The projected CAGR is approximately 39.00%.

2. Which companies are prominent players in the Small Transparent Display Industry?

Key companies in the market include Samsung Electronics Co Ltd, Pro Display, Nexnovo Technology Co Ltd, Crystal Display Systems Ltd, Hangzhou Hikvision Digital Technology Co Ltd, Planar Systems Inc (Leyard Optoelectronic Co ), Shenzhen AuroLED Technology Co Ltd, BOE Technology Grou, LG Electronics Co Ltd, Panasonic Corporation, 2Point0 Concepts.

3. What are the main segments of the Small Transparent Display Industry?

The market segments include Technology, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Advanced Displays in the Automotive Market; Growth of Augmented and Virtual Reality.

6. What are the notable trends driving market growth?

Retail Sector to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Complex Manufacturing Process and Expensive to Deploy in Consumer Products.

8. Can you provide examples of recent developments in the market?

Jul 2023: Tianma unveiled the latest transparent microLED display prototypes demonstrated at Display Week 2023. The company claims that the automotive sector is the primary application for these displays. The first display is an 8.75” (114 PPI) panel with an 880x480 resolution, 800 nits brightness, and more than 70% transparency.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Small Transparent Display Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Small Transparent Display Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Small Transparent Display Industry?

To stay informed about further developments, trends, and reports in the Small Transparent Display Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence