Key Insights

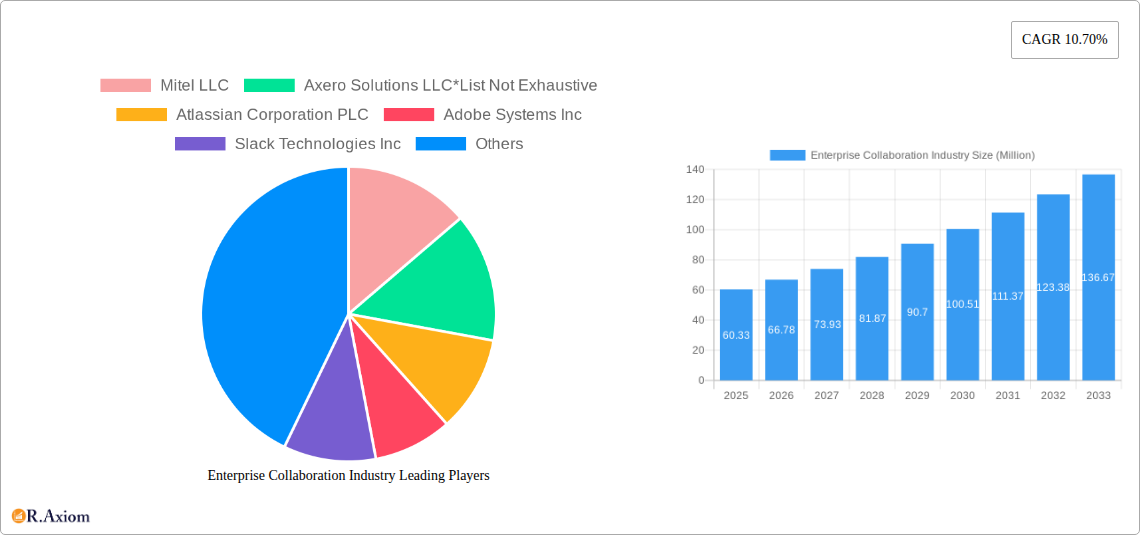

The Enterprise Collaboration Industry is poised for robust growth, projected to reach a substantial market size of USD 60.33 million. This expansion is driven by a compelling Compound Annual Growth Rate (CAGR) of 10.70% during the forecast period of 2025-2033. The primary catalysts fueling this surge include the increasing adoption of cloud-based deployment models, offering enhanced scalability, accessibility, and cost-efficiency for businesses of all sizes. Furthermore, the proliferation of advanced communication tools, sophisticated conferencing solutions, and integrated coordination platforms are vital in enabling seamless teamwork and boosting productivity across geographically dispersed workforces. Industries such as Telecommunications and IT, Travel and Hospitality, BFSI, Retail and Consumer Goods, Education, Transportation and Logistics, and Healthcare are significantly contributing to this market expansion as they increasingly rely on these tools to streamline operations and improve customer engagement.

The market's growth trajectory is further bolstered by the evolving nature of work, with a notable shift towards remote and hybrid work models. This necessitates robust digital collaboration infrastructure to maintain operational efficiency and foster a connected employee experience. While the adoption of on-premise solutions persists, particularly in sectors with stringent data security requirements, the agile and scalable nature of cloud-based offerings is rapidly gaining traction. Key players like Microsoft, Cisco, Salesforce, and Adobe are at the forefront, innovating and expanding their portfolios to meet the diverse needs of this dynamic market. However, challenges such as data security concerns and the integration complexities of disparate systems may pose some restraints, which the industry is actively addressing through enhanced security protocols and unified platform development. The strategic importance of enterprise collaboration in today's interconnected business environment ensures its continued upward trajectory.

Enterprise Collaboration Industry Market Concentration & Innovation

The enterprise collaboration market is characterized by moderate to high concentration, with several dominant players vying for market share. Major companies like Microsoft Corporation, Cisco System Inc., and Salesforce Com Inc. hold significant sway, driven by extensive product portfolios and established client bases. Innovation remains a critical differentiator, fueled by the rapid integration of Artificial Intelligence (AI), machine learning (ML), and automation technologies to enhance productivity and user experience. Regulatory frameworks, particularly concerning data privacy and security (e.g., GDPR, CCPA), are shaping product development and deployment strategies, demanding robust compliance measures. While direct product substitutes are limited within the core collaboration functionalities, adjacent solutions like project management software and specialized communication platforms can exert indirect competitive pressure. End-user demand is shifting towards seamless, integrated workflows and a mobile-first approach, compelling vendors to prioritize cloud-based solutions and intuitive interfaces. Mergers and acquisitions (M&A) are a prominent feature, with estimated M&A deal values reaching into the hundreds of millions to billions of dollars, as larger enterprises acquire innovative startups to expand their capabilities and market reach. For instance, recent M&A activities indicate a trend towards consolidating niche functionalities and acquiring advanced AI capabilities. This dynamic landscape ensures continuous evolution and a competitive environment where innovation and strategic partnerships are paramount for sustained growth.

Enterprise Collaboration Industry Industry Trends & Insights

The enterprise collaboration industry is experiencing robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 15% to 20% during the forecast period of 2025–2033. This expansion is primarily fueled by the accelerating digital transformation initiatives across all sectors, amplified by the widespread adoption of hybrid and remote work models that necessitate sophisticated communication and coordination tools. Technological advancements are at the forefront, with the pervasive integration of AI and ML capabilities enhancing features such as intelligent document analysis, automated meeting summaries, predictive analytics for project management, and personalized user experiences. Cloud-based solutions continue to dominate, offering scalability, flexibility, and cost-efficiency, with market penetration for cloud deployment models exceeding 70% in developed regions. Consumer preferences are increasingly dictating enterprise solutions, with employees demanding intuitive, user-friendly interfaces and seamless integration with their personal devices and preferred applications. This has led to a surge in demand for unified communication and collaboration (UC&C) platforms that consolidate messaging, video conferencing, file sharing, and project management into a single ecosystem. Competitive dynamics are intense, with established tech giants investing heavily in research and development to maintain their edge, while agile startups disrupt the market with specialized solutions. The increasing reliance on collaboration tools for business continuity, employee engagement, and operational efficiency across industries like Telecommunications and IT, Healthcare, and BFSI underscores the industry's critical role. Furthermore, the need for enhanced cybersecurity measures and data compliance is driving innovation in secure collaboration environments. The market penetration of advanced collaboration features, such as virtual reality (VR) and augmented reality (AR) for immersive meetings, is still nascent but represents a significant future growth avenue.

Dominant Markets & Segments in Enterprise Collaboration Industry

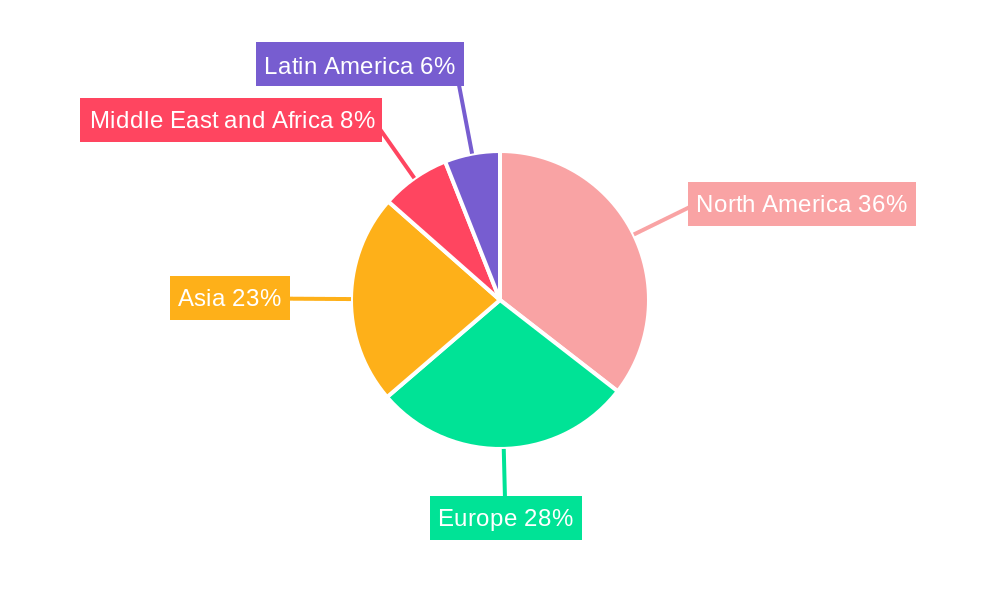

The enterprise collaboration industry showcases dynamic regional and segment dominance, driven by varying economic policies, infrastructure development, and industry-specific needs.

Leading Region/Country:

- North America currently leads the market, propelled by early adoption of advanced technologies, a high concentration of technology companies, and significant investments in digital transformation. The United States, in particular, represents a substantial portion of this dominance, owing to a mature IT infrastructure and a strong appetite for innovation.

- Europe follows closely, with countries like Germany, the UK, and France exhibiting strong growth, influenced by robust economic policies supporting digital initiatives and a significant presence of multinational corporations with extensive collaboration needs.

- Asia-Pacific is the fastest-growing region, driven by rapid digitalization in countries like China, India, and South Korea, coupled with increasing adoption of cloud-based solutions and a burgeoning startup ecosystem.

Dominant Deployment Type:

- Cloud-based deployment is the undisputed leader, projected to account for over 75% of the market share by 2025. This dominance is attributed to its scalability, cost-effectiveness, ease of deployment, and inherent flexibility, which are crucial for organizations of all sizes, especially in the context of remote and hybrid work environments.

- On-premise solutions, while still relevant for highly regulated industries or organizations with specific security concerns, are experiencing a gradual decline in market share, estimated to be around 25%.

Dominant Application:

- Communication Tools represent the largest segment, encompassing instant messaging, email integration, and internal social networking features. The fundamental need for seamless and immediate communication underpins its market leadership, with an estimated market share exceeding 40%.

- Conferencing Tools follow closely, with the surge in virtual meetings and webinars driving significant adoption. This segment is crucial for remote team collaboration and client interactions.

- Coordination Tools, including project management, task assignment, and workflow automation, are experiencing rapid growth as organizations seek to streamline operations and enhance productivity.

Dominant End-user Industry:

- Telecommunications and IT naturally leads the pack due to its inherent reliance on advanced communication and collaboration technologies for operational efficiency and innovation.

- BFSI (Banking, Financial Services, and Insurance) is a significant and rapidly growing segment, driven by the need for secure, compliant, and efficient collaboration for customer service, internal communication, and transaction processing.

- Healthcare is emerging as a critical growth area, with an increasing demand for secure platforms for telemedicine, patient management, and inter-departmental communication, especially post-pandemic.

- Education is also experiencing substantial growth, with institutions adopting collaboration tools for remote learning, administrative tasks, and student engagement.

- Travel and Hospitality, Retail and Consumer Goods, and Transportation and Logistics are increasingly adopting collaboration solutions to improve operational efficiency, supply chain management, and customer service.

Enterprise Collaboration Industry Product Developments

- Cloud-based deployment is the undisputed leader, projected to account for over 75% of the market share by 2025. This dominance is attributed to its scalability, cost-effectiveness, ease of deployment, and inherent flexibility, which are crucial for organizations of all sizes, especially in the context of remote and hybrid work environments.

- On-premise solutions, while still relevant for highly regulated industries or organizations with specific security concerns, are experiencing a gradual decline in market share, estimated to be around 25%.

Dominant Application:

- Communication Tools represent the largest segment, encompassing instant messaging, email integration, and internal social networking features. The fundamental need for seamless and immediate communication underpins its market leadership, with an estimated market share exceeding 40%.

- Conferencing Tools follow closely, with the surge in virtual meetings and webinars driving significant adoption. This segment is crucial for remote team collaboration and client interactions.

- Coordination Tools, including project management, task assignment, and workflow automation, are experiencing rapid growth as organizations seek to streamline operations and enhance productivity.

Dominant End-user Industry:

- Telecommunications and IT naturally leads the pack due to its inherent reliance on advanced communication and collaboration technologies for operational efficiency and innovation.

- BFSI (Banking, Financial Services, and Insurance) is a significant and rapidly growing segment, driven by the need for secure, compliant, and efficient collaboration for customer service, internal communication, and transaction processing.

- Healthcare is emerging as a critical growth area, with an increasing demand for secure platforms for telemedicine, patient management, and inter-departmental communication, especially post-pandemic.

- Education is also experiencing substantial growth, with institutions adopting collaboration tools for remote learning, administrative tasks, and student engagement.

- Travel and Hospitality, Retail and Consumer Goods, and Transportation and Logistics are increasingly adopting collaboration solutions to improve operational efficiency, supply chain management, and customer service.

Enterprise Collaboration Industry Product Developments

- Telecommunications and IT naturally leads the pack due to its inherent reliance on advanced communication and collaboration technologies for operational efficiency and innovation.

- BFSI (Banking, Financial Services, and Insurance) is a significant and rapidly growing segment, driven by the need for secure, compliant, and efficient collaboration for customer service, internal communication, and transaction processing.

- Healthcare is emerging as a critical growth area, with an increasing demand for secure platforms for telemedicine, patient management, and inter-departmental communication, especially post-pandemic.

- Education is also experiencing substantial growth, with institutions adopting collaboration tools for remote learning, administrative tasks, and student engagement.

- Travel and Hospitality, Retail and Consumer Goods, and Transportation and Logistics are increasingly adopting collaboration solutions to improve operational efficiency, supply chain management, and customer service.

Enterprise Collaboration Industry Product Developments

The enterprise collaboration landscape is witnessing a flurry of product innovations focused on enhancing user experience and operational efficiency. Key trends include the integration of advanced AI and ML capabilities for intelligent task automation, predictive analytics, and personalized communication flows. Vendors are prioritizing seamless integration across diverse platforms and applications, offering unified dashboards for messaging, video conferencing, and project management. Development efforts are also concentrated on strengthening security protocols and ensuring compliance with evolving data privacy regulations. For instance, the introduction of AI-enabled platforms that convert unstructured data into structured formats, as seen with Google Cloud's recent launch, is a prime example of innovation addressing specific industry needs like prior authorization and claims processing in healthcare. These advancements aim to boost productivity, foster better teamwork, and provide a competitive edge in a rapidly evolving market.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global enterprise collaboration market, segmented across key parameters to offer detailed insights into market dynamics and growth projections. The segmentation includes:

- Deployment Type: This section analyzes the market split between On-premise and Cloud-based solutions. Cloud-based solutions are projected to maintain their dominance due to scalability and flexibility, while on-premise solutions cater to specific security and regulatory needs.

- Application: The report delves into the market for Communication Tools, Conferencing Tools, and Coordination Tools. Communication tools lead, driven by essential business needs, while conferencing and coordination tools are experiencing rapid growth due to remote work trends and productivity demands.

- End-user Industry: A granular analysis is provided for Telecommunications and IT, Travel and Hospitality, BFSI, Retail and Consumer Goods, Education, Transportation and Logistics, Healthcare, and Other End-user Industries. The Telecommunications and IT and BFSI sectors currently hold significant market share, with Healthcare and Education showing substantial growth potential driven by digital transformation and evolving operational requirements.

Key Drivers of Enterprise Collaboration Industry Growth

The enterprise collaboration industry's growth is propelled by several potent drivers. The pervasive shift towards hybrid and remote work models necessitates robust digital tools for maintaining connectivity and productivity. Technological advancements, particularly in AI and ML, are enhancing the functionality and intelligence of collaboration platforms, offering predictive analytics and automation. Increasing globalization and the need for seamless cross-border communication also contribute significantly. Furthermore, the growing emphasis on employee engagement and streamlined workflow management as strategic business imperatives is driving adoption across all sectors. Government initiatives promoting digitalization and improved IT infrastructure in various regions are also acting as significant catalysts.

Challenges in the Enterprise Collaboration Industry Sector

Despite its robust growth, the enterprise collaboration sector faces several challenges. Ensuring comprehensive data security and privacy compliance across diverse regulatory landscapes (e.g., GDPR, CCPA) remains a significant hurdle for vendors. The integration of disparate legacy systems and new collaboration tools can be complex and costly for organizations. Fierce competition among a multitude of vendors, including large established players and agile startups, leads to pricing pressures and demands for continuous innovation. User adoption and training can also be a barrier, as employees may resist new workflows or find certain tools unintuitive. Furthermore, the potential for information overload and distractions from constant communication streams requires careful platform design and user management.

Emerging Opportunities in Enterprise Collaboration Industry

Emerging opportunities in the enterprise collaboration industry lie in the continued advancement and integration of AI for more intelligent and predictive functionalities, such as proactive issue resolution and personalized workflow recommendations. The expansion of immersive collaboration technologies, including VR and AR for virtual meetings and training, presents a significant growth avenue. Tailoring solutions for niche industries, such as specialized collaboration tools for research and development or highly regulated environments, offers untapped potential. The increasing demand for cybersecurity-focused collaboration platforms, especially in sectors like healthcare and finance, is another key opportunity. Furthermore, focusing on sustainable and eco-friendly collaboration solutions could appeal to a growing segment of environmentally conscious organizations.

Leading Players in the Enterprise Collaboration Industry Market

- Mitel LLC

- Axero Solutions LLC

- Atlassian Corporation PLC

- Adobe Systems Inc

- Slack Technologies Inc

- TIBCO Software Inc

- IBM Corporation

- Jive Software

- Polycom Inc

- Microsoft Corporation

- Salesforce Com Inc

- Zoho Corporation Pvt Ltd

- Huawei Technologies Co Ltd

- Cisco System Inc

- SAP SE

Key Developments in Enterprise Collaboration Industry Industry

- April 2023: Google Cloud launched an AI-enabled platform for prior authorization and claims processing powered by a new data and analytics tool. The latest offering will convert unstructured data into structured data and can help payers meet existing and proposed CMS rules around interoperability and prior authorization, including using HL7 FHIR. This development signifies a move towards AI-driven automation and data standardization in healthcare collaboration.

- February 2022: IceWarp, a global player in developing unified collaboration tools and messaging solutions for companies of all sizes, expanded its presence in the Middle East by opening its first office in the prime area of Business Bay in Dubai. IceWarp provides businesses with affordable, seamlessly integrated, easy-to-use communication solutions that protect all corporation collaboration and productivity aspects. This expansion highlights the growing demand for integrated collaboration solutions in emerging markets.

Strategic Outlook for Enterprise Collaboration Industry Market

The strategic outlook for the enterprise collaboration industry remains exceptionally positive, driven by sustained demand for digital workplace solutions. Future growth will be fueled by the deeper integration of AI and machine learning, leading to more intelligent and predictive collaboration experiences. The continued adoption of cloud-native architectures will ensure scalability and agility for businesses. Companies that successfully deliver secure, compliant, and user-friendly platforms that seamlessly integrate diverse communication and workflow tools will capture significant market share. Emerging technologies like VR/AR for immersive collaboration and specialized industry solutions present substantial opportunities for differentiation and expansion. Strategic partnerships and potential M&A activities will continue to shape the competitive landscape, enabling players to consolidate offerings and expand their technological capabilities.

Enterprise Collaboration Industry Segmentation

-

1. Deployment Type

- 1.1. On-premise

- 1.2. Cloud-based

-

2. Application

- 2.1. Communication Tools

- 2.2. Conferencing Tools

- 2.3. Coordination Tools

-

3. End-user Industry

- 3.1. Telecommunications and IT

- 3.2. Travel and Hospitality

- 3.3. BFSI

- 3.4. Retail and Consumer Goods

- 3.5. Education

- 3.6. Transportation and Logistics

- 3.7. Healthcare

- 3.8. Other End-user Industries

Enterprise Collaboration Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Spain

-

3. Asia

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Enterprise Collaboration Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.70% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. API Integration for Greater Efficiency; Increase in Usage of Mobile Devices for Time Management

- 3.3. Market Restrains

- 3.3.1. Data Security While Deploying SDDC is a Major Challenge

- 3.4. Market Trends

- 3.4.1. Cloud-based Deployment to Increase the Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 5.1.1. On-premise

- 5.1.2. Cloud-based

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Communication Tools

- 5.2.2. Conferencing Tools

- 5.2.3. Coordination Tools

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Telecommunications and IT

- 5.3.2. Travel and Hospitality

- 5.3.3. BFSI

- 5.3.4. Retail and Consumer Goods

- 5.3.5. Education

- 5.3.6. Transportation and Logistics

- 5.3.7. Healthcare

- 5.3.8. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6. North America Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6.1.1. On-premise

- 6.1.2. Cloud-based

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Communication Tools

- 6.2.2. Conferencing Tools

- 6.2.3. Coordination Tools

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Telecommunications and IT

- 6.3.2. Travel and Hospitality

- 6.3.3. BFSI

- 6.3.4. Retail and Consumer Goods

- 6.3.5. Education

- 6.3.6. Transportation and Logistics

- 6.3.7. Healthcare

- 6.3.8. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7. Europe Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7.1.1. On-premise

- 7.1.2. Cloud-based

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Communication Tools

- 7.2.2. Conferencing Tools

- 7.2.3. Coordination Tools

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Telecommunications and IT

- 7.3.2. Travel and Hospitality

- 7.3.3. BFSI

- 7.3.4. Retail and Consumer Goods

- 7.3.5. Education

- 7.3.6. Transportation and Logistics

- 7.3.7. Healthcare

- 7.3.8. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8. Asia Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8.1.1. On-premise

- 8.1.2. Cloud-based

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Communication Tools

- 8.2.2. Conferencing Tools

- 8.2.3. Coordination Tools

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Telecommunications and IT

- 8.3.2. Travel and Hospitality

- 8.3.3. BFSI

- 8.3.4. Retail and Consumer Goods

- 8.3.5. Education

- 8.3.6. Transportation and Logistics

- 8.3.7. Healthcare

- 8.3.8. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9. Australia and New Zealand Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9.1.1. On-premise

- 9.1.2. Cloud-based

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Communication Tools

- 9.2.2. Conferencing Tools

- 9.2.3. Coordination Tools

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Telecommunications and IT

- 9.3.2. Travel and Hospitality

- 9.3.3. BFSI

- 9.3.4. Retail and Consumer Goods

- 9.3.5. Education

- 9.3.6. Transportation and Logistics

- 9.3.7. Healthcare

- 9.3.8. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10. Latin America Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10.1.1. On-premise

- 10.1.2. Cloud-based

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Communication Tools

- 10.2.2. Conferencing Tools

- 10.2.3. Coordination Tools

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Telecommunications and IT

- 10.3.2. Travel and Hospitality

- 10.3.3. BFSI

- 10.3.4. Retail and Consumer Goods

- 10.3.5. Education

- 10.3.6. Transportation and Logistics

- 10.3.7. Healthcare

- 10.3.8. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11. Middle East and Africa Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11.1.1. On-premise

- 11.1.2. Cloud-based

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Communication Tools

- 11.2.2. Conferencing Tools

- 11.2.3. Coordination Tools

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Telecommunications and IT

- 11.3.2. Travel and Hospitality

- 11.3.3. BFSI

- 11.3.4. Retail and Consumer Goods

- 11.3.5. Education

- 11.3.6. Transportation and Logistics

- 11.3.7. Healthcare

- 11.3.8. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Deployment Type

- 12. North America Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United States

- 12.1.2 Canada

- 13. Europe Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 United Kingdom

- 13.1.2 Germany

- 13.1.3 France

- 13.1.4 Spain

- 14. Asia Pacific Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 China

- 14.1.2 Japan

- 14.1.3 India

- 14.1.4 South Korea

- 15. Latin America Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Middle East and Africa Enterprise Collaboration Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1.

- 17. Competitive Analysis

- 17.1. Global Market Share Analysis 2024

- 17.2. Company Profiles

- 17.2.1 Mitel LLC

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 Axero Solutions LLC*List Not Exhaustive

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 Atlassian Corporation PLC

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 Adobe Systems Inc

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 Slack Technologies Inc

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.6 TIBCO Software Inc

- 17.2.6.1. Overview

- 17.2.6.2. Products

- 17.2.6.3. SWOT Analysis

- 17.2.6.4. Recent Developments

- 17.2.6.5. Financials (Based on Availability)

- 17.2.7 IBM Corporation

- 17.2.7.1. Overview

- 17.2.7.2. Products

- 17.2.7.3. SWOT Analysis

- 17.2.7.4. Recent Developments

- 17.2.7.5. Financials (Based on Availability)

- 17.2.8 Jive Software

- 17.2.8.1. Overview

- 17.2.8.2. Products

- 17.2.8.3. SWOT Analysis

- 17.2.8.4. Recent Developments

- 17.2.8.5. Financials (Based on Availability)

- 17.2.9 Polycom Inc

- 17.2.9.1. Overview

- 17.2.9.2. Products

- 17.2.9.3. SWOT Analysis

- 17.2.9.4. Recent Developments

- 17.2.9.5. Financials (Based on Availability)

- 17.2.10 Microsoft Corporation

- 17.2.10.1. Overview

- 17.2.10.2. Products

- 17.2.10.3. SWOT Analysis

- 17.2.10.4. Recent Developments

- 17.2.10.5. Financials (Based on Availability)

- 17.2.11 Salesforce Com Inc

- 17.2.11.1. Overview

- 17.2.11.2. Products

- 17.2.11.3. SWOT Analysis

- 17.2.11.4. Recent Developments

- 17.2.11.5. Financials (Based on Availability)

- 17.2.12 Zoho Corporation Pvt Ltd

- 17.2.12.1. Overview

- 17.2.12.2. Products

- 17.2.12.3. SWOT Analysis

- 17.2.12.4. Recent Developments

- 17.2.12.5. Financials (Based on Availability)

- 17.2.13 Huawei Technologies Co Ltd

- 17.2.13.1. Overview

- 17.2.13.2. Products

- 17.2.13.3. SWOT Analysis

- 17.2.13.4. Recent Developments

- 17.2.13.5. Financials (Based on Availability)

- 17.2.14 Cisco System Inc

- 17.2.14.1. Overview

- 17.2.14.2. Products

- 17.2.14.3. SWOT Analysis

- 17.2.14.4. Recent Developments

- 17.2.14.5. Financials (Based on Availability)

- 17.2.15 SAP SE

- 17.2.15.1. Overview

- 17.2.15.2. Products

- 17.2.15.3. SWOT Analysis

- 17.2.15.4. Recent Developments

- 17.2.15.5. Financials (Based on Availability)

- 17.2.1 Mitel LLC

List of Figures

- Figure 1: Global Enterprise Collaboration Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Enterprise Collaboration Industry Revenue (Million), by Deployment Type 2024 & 2032

- Figure 13: North America Enterprise Collaboration Industry Revenue Share (%), by Deployment Type 2024 & 2032

- Figure 14: North America Enterprise Collaboration Industry Revenue (Million), by Application 2024 & 2032

- Figure 15: North America Enterprise Collaboration Industry Revenue Share (%), by Application 2024 & 2032

- Figure 16: North America Enterprise Collaboration Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 17: North America Enterprise Collaboration Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 18: North America Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: North America Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Europe Enterprise Collaboration Industry Revenue (Million), by Deployment Type 2024 & 2032

- Figure 21: Europe Enterprise Collaboration Industry Revenue Share (%), by Deployment Type 2024 & 2032

- Figure 22: Europe Enterprise Collaboration Industry Revenue (Million), by Application 2024 & 2032

- Figure 23: Europe Enterprise Collaboration Industry Revenue Share (%), by Application 2024 & 2032

- Figure 24: Europe Enterprise Collaboration Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 25: Europe Enterprise Collaboration Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 26: Europe Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Europe Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Asia Enterprise Collaboration Industry Revenue (Million), by Deployment Type 2024 & 2032

- Figure 29: Asia Enterprise Collaboration Industry Revenue Share (%), by Deployment Type 2024 & 2032

- Figure 30: Asia Enterprise Collaboration Industry Revenue (Million), by Application 2024 & 2032

- Figure 31: Asia Enterprise Collaboration Industry Revenue Share (%), by Application 2024 & 2032

- Figure 32: Asia Enterprise Collaboration Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 33: Asia Enterprise Collaboration Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 34: Asia Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Asia Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Australia and New Zealand Enterprise Collaboration Industry Revenue (Million), by Deployment Type 2024 & 2032

- Figure 37: Australia and New Zealand Enterprise Collaboration Industry Revenue Share (%), by Deployment Type 2024 & 2032

- Figure 38: Australia and New Zealand Enterprise Collaboration Industry Revenue (Million), by Application 2024 & 2032

- Figure 39: Australia and New Zealand Enterprise Collaboration Industry Revenue Share (%), by Application 2024 & 2032

- Figure 40: Australia and New Zealand Enterprise Collaboration Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 41: Australia and New Zealand Enterprise Collaboration Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 42: Australia and New Zealand Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Australia and New Zealand Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 44: Latin America Enterprise Collaboration Industry Revenue (Million), by Deployment Type 2024 & 2032

- Figure 45: Latin America Enterprise Collaboration Industry Revenue Share (%), by Deployment Type 2024 & 2032

- Figure 46: Latin America Enterprise Collaboration Industry Revenue (Million), by Application 2024 & 2032

- Figure 47: Latin America Enterprise Collaboration Industry Revenue Share (%), by Application 2024 & 2032

- Figure 48: Latin America Enterprise Collaboration Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 49: Latin America Enterprise Collaboration Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 50: Latin America Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 51: Latin America Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

- Figure 52: Middle East and Africa Enterprise Collaboration Industry Revenue (Million), by Deployment Type 2024 & 2032

- Figure 53: Middle East and Africa Enterprise Collaboration Industry Revenue Share (%), by Deployment Type 2024 & 2032

- Figure 54: Middle East and Africa Enterprise Collaboration Industry Revenue (Million), by Application 2024 & 2032

- Figure 55: Middle East and Africa Enterprise Collaboration Industry Revenue Share (%), by Application 2024 & 2032

- Figure 56: Middle East and Africa Enterprise Collaboration Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 57: Middle East and Africa Enterprise Collaboration Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 58: Middle East and Africa Enterprise Collaboration Industry Revenue (Million), by Country 2024 & 2032

- Figure 59: Middle East and Africa Enterprise Collaboration Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Enterprise Collaboration Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 3: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: Global Enterprise Collaboration Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: United Kingdom Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Germany Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Spain Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: China Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Japan Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: India Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: South Korea Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 24: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 25: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 26: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: United States Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Canada Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 30: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 31: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 32: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 33: United Kingdom Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Germany Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: France Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Spain Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 38: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 39: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 40: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 41: China Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Japan Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: India Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Enterprise Collaboration Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 46: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 47: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 48: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 49: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 50: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 51: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 52: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 53: Global Enterprise Collaboration Industry Revenue Million Forecast, by Deployment Type 2019 & 2032

- Table 54: Global Enterprise Collaboration Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 55: Global Enterprise Collaboration Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 56: Global Enterprise Collaboration Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Enterprise Collaboration Industry?

The projected CAGR is approximately 10.70%.

2. Which companies are prominent players in the Enterprise Collaboration Industry?

Key companies in the market include Mitel LLC, Axero Solutions LLC*List Not Exhaustive, Atlassian Corporation PLC, Adobe Systems Inc, Slack Technologies Inc, TIBCO Software Inc, IBM Corporation, Jive Software, Polycom Inc, Microsoft Corporation, Salesforce Com Inc, Zoho Corporation Pvt Ltd, Huawei Technologies Co Ltd, Cisco System Inc, SAP SE.

3. What are the main segments of the Enterprise Collaboration Industry?

The market segments include Deployment Type, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 60.33 Million as of 2022.

5. What are some drivers contributing to market growth?

API Integration for Greater Efficiency; Increase in Usage of Mobile Devices for Time Management.

6. What are the notable trends driving market growth?

Cloud-based Deployment to Increase the Market Growth.

7. Are there any restraints impacting market growth?

Data Security While Deploying SDDC is a Major Challenge.

8. Can you provide examples of recent developments in the market?

April 2023: Google Cloud launched an AI-enabled platform for prior authorization and claims processing powered by a new data and analytics tool. The latest offering will convert unstructured data into structured data and can help payers meet existing and proposed CMS rules around interoperability and prior authorization, including using HL7 FHIR.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Enterprise Collaboration Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Enterprise Collaboration Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Enterprise Collaboration Industry?

To stay informed about further developments, trends, and reports in the Enterprise Collaboration Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence