Key Insights

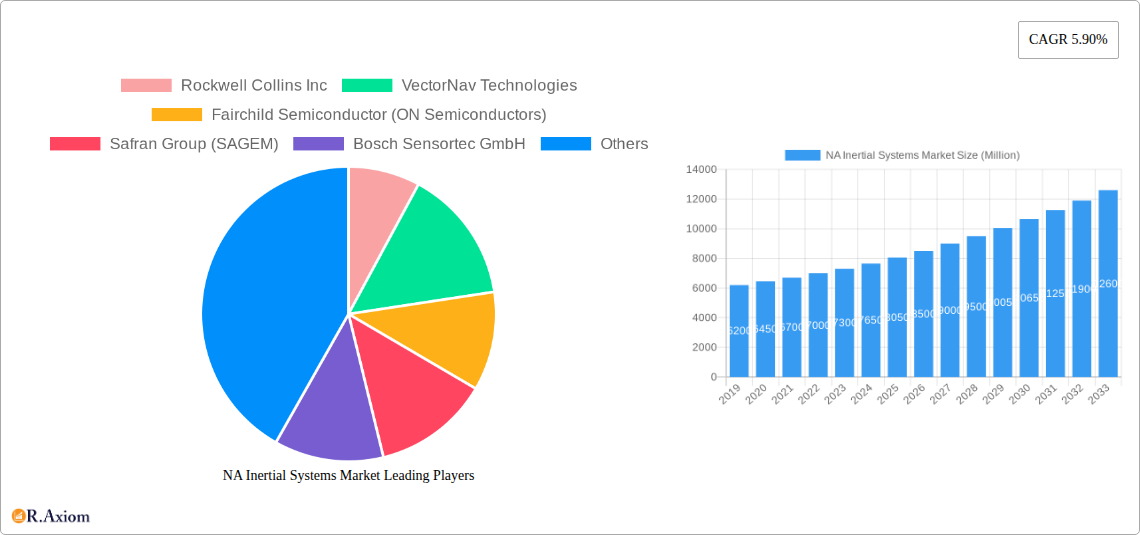

The North American (NA) Inertial Systems Market is poised for robust expansion, projected to reach approximately $8,500 million by 2025, driven by a Compound Annual Growth Rate (CAGR) of 5.90% through 2033. This growth is primarily fueled by the increasing adoption of inertial systems across critical sectors such as Civil Aviation and Defense, where precision navigation, guidance, and control are paramount. The burgeoning demand for advanced unmanned aerial vehicles (UAVs) in both commercial and military applications, coupled with the continuous evolution of commercial aviation with sophisticated avionics, are significant growth catalysts. Furthermore, the automotive sector's embrace of autonomous driving technologies, requiring highly accurate sensor fusion, and the expanding use of inertial measurement units (IMUs) in the Medical and Consumer Electronics industries, are contributing to this upward trajectory. Advancements in MEMS (Micro-Electro-Mechanical Systems) technology are leading to smaller, more cost-effective, and higher-performing inertial sensors, further democratizing their application.

The market's upward momentum is supported by key trends including the miniaturization of inertial components, the integration of advanced algorithms for enhanced accuracy and reliability, and the growing emphasis on cybersecurity within navigation systems. The development of highly sophisticated Attitude Heading and Navigation Systems (AHNS) and IMUs with reduced drift and improved stability are critical for achieving next-generation performance in various applications. However, certain restraints, such as the high cost associated with cutting-edge inertial system development and integration, and the stringent regulatory requirements, particularly in the aerospace and defense sectors, could temper immediate growth. The competitive landscape features established players like Honeywell Aerospace Inc. and Rockwell Collins Inc., alongside innovative companies such as Bosch Sensortec GmbH and STMicroelectronics NV, constantly pushing the boundaries of inertial sensing technology across the United States and Canada.

North America Inertial Systems Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides an exhaustive analysis of the North American Inertial Systems Market, encompassing a historical review of 2019-2024, a base year assessment of 2025, and a comprehensive forecast for 2025-2033. We delve into critical market dynamics, including market concentration, innovation drivers, regulatory landscapes, competitive strategies, and emerging trends across key segments like Civil Aviation, Defense, Consumer Electronics, Automotive, Energy & Infrastructure, and Medical. Leveraging high-traffic keywords such as "inertial navigation systems," "IMU market," "aerospace inertial sensors," "automotive INS," and "defense guidance systems," this report is meticulously crafted to enhance search visibility and provide actionable intelligence for industry stakeholders.

NA Inertial Systems Market Market Concentration & Innovation

The North American Inertial Systems Market exhibits a moderate to high level of concentration, driven by the dominance of established aerospace and defense contractors and the presence of specialized component manufacturers. Key players like Honeywell Aerospace Inc., Northrop Grumman Corporation, and Rockwell Collins Inc. hold significant market shares due to their long-standing relationships, extensive R&D capabilities, and comprehensive product portfolios. Innovation is a primary growth catalyst, fueled by the demand for enhanced accuracy, miniaturization, reduced power consumption, and increased resilience in challenging environments. The integration of advanced algorithms, MEMS technology, and GPS/GNSS fusion for improved navigation performance are critical innovation drivers. Regulatory frameworks, particularly in the defense and aerospace sectors, influence product development and market entry. While product substitutes exist, such as GPS-only solutions or vision-based navigation in specific applications, the inherent advantages of inertial systems in GNSS-denied environments and for precise short-term trajectory estimation maintain their indispensability. End-user trends point towards increasing adoption in autonomous systems, from drones and autonomous vehicles to advanced robotics and precision agriculture. Mergers and acquisitions (M&A) activities, while not as frequent as in broader tech markets, play a role in market consolidation and technology acquisition. For instance, the acquisition of InvenSense by TDK (though not explicitly detailed for NA market impact here) highlights the strategic importance of sensor technology. Deal values for significant M&A activities in this specialized sector are often substantial, reflecting the high-value nature of the underlying technologies and intellectual property.

NA Inertial Systems Market Industry Trends & Insights

The North American Inertial Systems Market is poised for robust growth, propelled by an escalating demand for precise and reliable navigation and guidance solutions across diverse sectors. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% from 2025 to 2033, reaching an estimated market size of over $3,500 million by 2033. This expansion is significantly driven by advancements in autonomous technologies, the increasing sophistication of defense systems, and the burgeoning demand for advanced driver-assistance systems (ADAS) in the automotive industry. Technological disruptions, such as the continuous miniaturization and cost reduction of MEMS-based inertial sensors (accelerometers and gyroscopes), are democratizing access to inertial measurement units (IMUs) and making them viable for a broader range of applications, including consumer electronics and industrial automation. Consumer preferences are increasingly leaning towards integrated and seamless navigation experiences, pushing for higher accuracy and longer operational autonomy, particularly in unmanned aerial vehicles (UAVs) and robotics. Competitive dynamics are characterized by intense R&D investment, strategic partnerships between component manufacturers and system integrators, and a focus on developing highly reliable and robust inertial navigation systems (INS). The market penetration of high-performance INS is expected to deepen across all segments, as the limitations of GPS-only solutions become more apparent in complex operational environments. Furthermore, the ongoing development of fused navigation systems that combine inertial data with other sensor inputs (GNSS, lidar, vision) is a significant trend, enhancing overall system performance and resilience. The energy and infrastructure sector is also showing increased interest in inertial systems for surveying, monitoring, and pipeline inspection, contributing to market diversification.

Dominant Markets & Segments in NA Inertial Systems Market

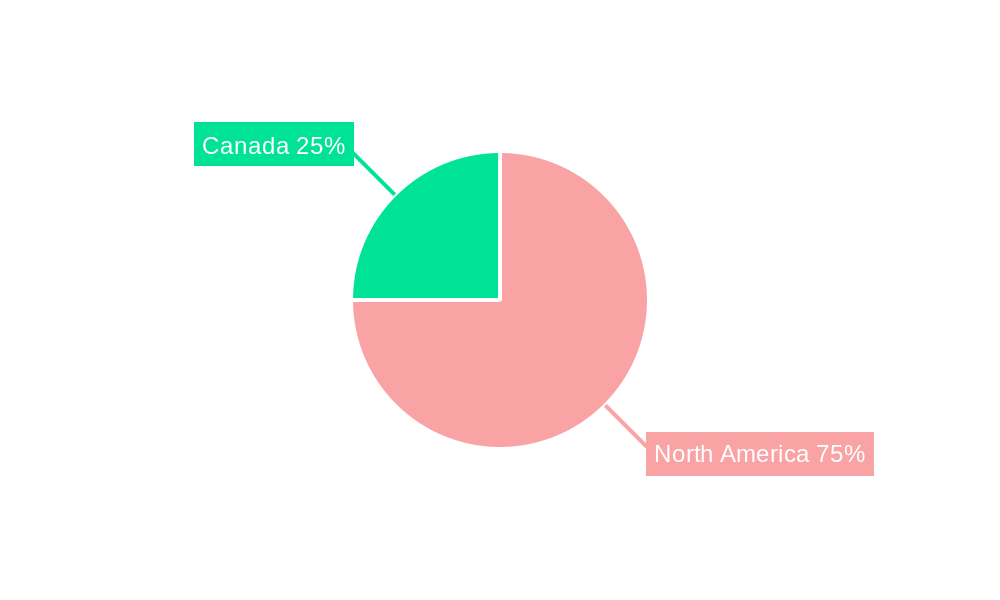

The North American Inertial Systems Market is significantly shaped by the United States as the dominant geographical segment, accounting for over 75% of the regional market share. This leadership is underpinned by substantial government spending on defense modernization, a thriving aerospace industry, and a leading position in automotive innovation and consumer electronics. The Defense application segment emerges as the largest contributor, driven by the need for advanced navigation and guidance systems in military aircraft, naval vessels, ground vehicles, and unmanned systems. Key drivers include geopolitical factors, national security imperatives, and the ongoing development of intelligent and autonomous warfare capabilities.

Dominant Application Segments:

- Defense: Continuous procurement of advanced INS for fighter jets, drones, submarines, and tactical ground vehicles. The integration of AI and machine learning in defense systems further amplifies the need for precise inertial data.

- Civil Aviation: Growth in commercial air travel, coupled with the adoption of advanced avionics and autonomous flight technologies, fuels demand for inertial reference systems (IRS) and attitude and heading reference systems (AHRS).

- Automotive: The rapid expansion of ADAS features, the development of autonomous driving capabilities, and the increasing use of digital maps necessitate sophisticated inertial sensors for accurate vehicle positioning and motion tracking.

Dominant Component Segments:

- IMU (Inertial Measurement Unit): As the core of most inertial systems, IMUs, encompassing accelerometers and gyroscopes, represent the largest component segment due to their widespread application across all end-use industries.

- Attitude Heading and Navigation System (AHNS): These systems, often integrating IMUs with magnetometers and GPS, are crucial for providing complete navigational awareness, particularly in aviation and defense.

Geographical Dominance:

- United States: Robust defense budget, significant aerospace manufacturing base, and a leading automotive sector are key drivers. Government initiatives supporting technological advancement and innovation further bolster its position.

The Energy and Infrastructure and Medical segments, while smaller in current market share, are showing promising growth trajectories, driven by the need for precision in exploration, asset management, and advanced medical robotics.

NA Inertial Systems Market Product Developments

Product development in the North American Inertial Systems Market is characterized by a relentless pursuit of enhanced accuracy, reduced size, weight, power, and cost (SWaP-C), and improved performance in challenging environments. Innovations focus on sophisticated sensor fusion techniques, advanced gyroscopic technologies (e.g., fiber optic gyros for high-end applications and MEMS gyros for broader adoption), and the integration of machine learning algorithms for self-calibration and improved data interpretation. The development of compact, high-performance IMUs for UAVs and small satellites is a significant trend. These advancements enable new applications, such as highly precise drone-based surveying, autonomous navigation in GNSS-denied urban canyons, and advanced surgical robotics. Competitive advantages are gained through superior algorithmic processing, robust sensor packaging, and the ability to provide reliable data in dynamic and disruptive conditions.

Report Scope & Segmentation Analysis

This report meticulously segments the North American Inertial Systems Market by application, component, and geography.

- Application Segmentation: This covers Civil Aviation, Defense, Consumer Electronics, Automotive, Energy and Infrastructure, Medical, and Other Applications. Each segment is analyzed for its current market size, projected growth, and key market dynamics, with Defense and Civil Aviation expected to lead in market share during the forecast period.

- Component Segmentation: This includes Accelerometer, Gyroscope, IMU, Magnetometer, Attitude Heading and Navigation System, and Other Components. The IMU segment is projected to hold the largest market share due to its fundamental role across all applications, followed by accelerometers and gyroscopes as their core constituents.

- Geographical Segmentation: The analysis focuses on United States and Canada. The United States is anticipated to dominate the market, driven by its extensive defense spending, advanced aerospace industry, and rapid adoption of new technologies.

Key Drivers of NA Inertial Systems Market Growth

The growth of the North American Inertial Systems Market is propelled by several key factors. The escalating demand for autonomy across sectors, particularly in defense, automotive, and consumer electronics, is a primary driver, necessitating precise and reliable navigation. Continuous technological advancements in MEMS sensors are leading to smaller, more affordable, and higher-performing IMUs. Furthermore, the increasing sophistication of defense applications, including unmanned systems and precision-guided munitions, relies heavily on advanced inertial guidance. The growing adoption of ADAS and autonomous driving technologies in the automotive sector is also a significant growth catalyst. Finally, favorable government initiatives and funding for aerospace and defense research and development in both the United States and Canada contribute to market expansion.

Challenges in the NA Inertial Systems Market Sector

Despite the promising outlook, the North American Inertial Systems Market faces several challenges. The high cost of advanced inertial components, particularly for high-end fiber optic gyroscopes and specialized military-grade IMUs, can be a barrier to adoption in price-sensitive applications. Intense competition among established players and emerging technology providers can lead to pricing pressures and impact profitability. Furthermore, supply chain disruptions, as witnessed in recent years, can affect the availability of critical raw materials and components, leading to production delays. Regulatory hurdles, especially concerning export controls and certifications for defense and aerospace applications, can also pose challenges for market entry and expansion. Over-reliance on GNSS in certain applications, despite its limitations in denied environments, can sometimes hinder the adoption of purely inertial solutions.

Emerging Opportunities in NA Inertial Systems Market

Emerging opportunities within the North American Inertial Systems Market are substantial and diverse. The rapid growth of the commercial drone market for delivery, inspection, and surveillance presents a significant opportunity for cost-effective and high-performance IMUs. The expansion of autonomous vehicles, extending beyond passenger cars to include autonomous trucking and logistics, will drive demand for sophisticated inertial navigation solutions. The increasing focus on smart city infrastructure and the development of intelligent transportation systems offer new avenues for inertial sensor integration. Furthermore, the healthcare sector's growing adoption of robotic surgery and advanced patient monitoring systems creates a niche but high-value market for medical-grade inertial sensors. The exploration and production of energy resources, particularly in remote and challenging offshore environments, will continue to drive demand for inertial systems in navigation and asset monitoring.

Leading Players in the NA Inertial Systems Market Market

- Rockwell Collins Inc.

- VectorNav Technologies

- Fairchild Semiconductor (ON Semiconductors)

- Safran Group (SAGEM)

- Bosch Sensortec GmbH

- Moog Inc.

- Thales Group

- STMicroelectronics NV

- Meggitt PLC

- Analog Devices Inc.

- Honeywell Aerospace Inc.

- InvenSense Inc.

- Northrop Grumman Corporation

Key Developments in NA Inertial Systems Market Industry

- January 2023: Inertial Labs released an upgraded version of the "INS-U" GPS-Aided Inertial Navigation System and an extended version of the Differential Pressure Sensor and Embedded Air Data Computer, allowing the unit to measure airspeed with up to 600 KNOTS to enhance high dynamic applications. This new INS-U version can send fused (GNSS + IMU) NMEA data to Pixhawk Autopilot, allowing Pixhawk Autopilot to navigate UAVs in GNSS-denied environments for extended periods (more than 1 hour).

- July 2022: TT Electronics, a technology provider of engineered technologies for mission-critical applications, announced that its Kansas City facility received a Letter of Authority from long-term partner Honeywell Aerospace to begin designing a new power supply for next-generation inertial navigation units.

Strategic Outlook for NA Inertial Systems Market Market

The strategic outlook for the North American Inertial Systems Market is highly optimistic, driven by sustained demand for advanced navigation and guidance technologies across key sectors. The increasing integration of inertial systems with AI and machine learning will unlock new capabilities in autonomous decision-making and predictive maintenance. Strategic partnerships between sensor manufacturers and system integrators will be crucial for developing tailored solutions for specific applications. Investments in research and development focused on miniaturization, increased accuracy, and improved resilience in challenging environments will remain paramount. The growing adoption of inertial measurement units in emerging markets like consumer robotics and advanced healthcare applications presents significant long-term growth potential. Furthermore, the ongoing evolution of autonomous vehicles and the continued modernization of defense capabilities will ensure a robust pipeline of demand for inertial system solutions. The market is expected to witness a continued trend of innovation, leading to more integrated and intelligent navigation systems.

NA Inertial Systems Market Segmentation

-

1. Application

- 1.1. Civil Aviation

- 1.2. Defense

- 1.3. Consumer Electronics

- 1.4. Automotive

- 1.5. Energy and Infrastructure

- 1.6. Medical

- 1.7. Other Applications

-

2. Component

- 2.1. Accelerometer

- 2.2. Gyroscope

- 2.3. IMU

- 2.4. Magnetometer

- 2.5. Attitude Heading and Navigation System

- 2.6. Other Components

-

3. Geography

- 3.1. United States

- 3.2. Canada

NA Inertial Systems Market Segmentation By Geography

- 1. United States

- 2. Canada

NA Inertial Systems Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

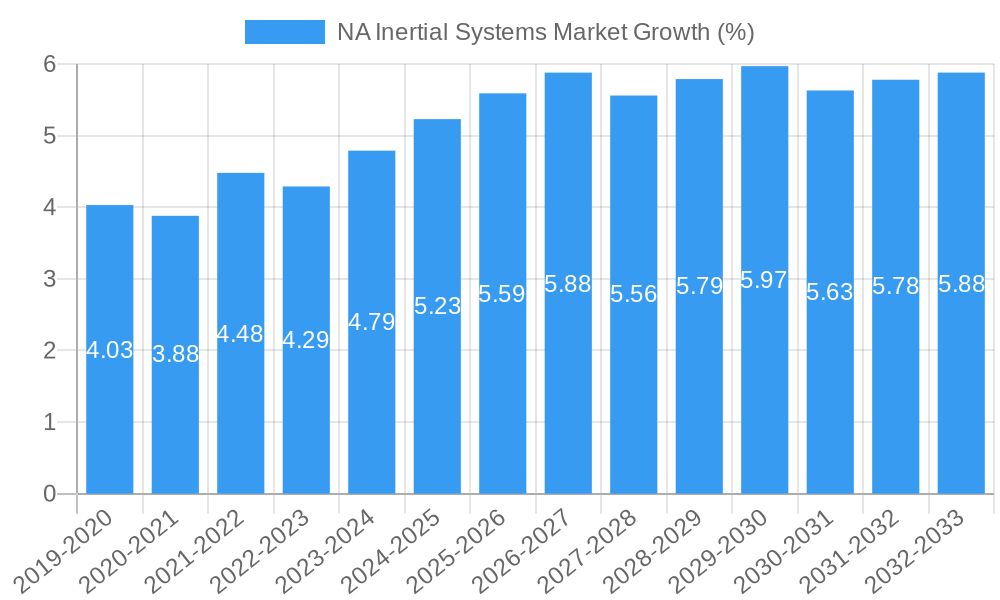

| Growth Rate | CAGR of 5.90% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Emergence of MEMS Technology; Inclination of Growth Toward Defense and Aerospace; Technological Advancements in Navigation Systems

- 3.3. Market Restrains

- 3.3.1. Operational Complexity and High Maintenance Costs

- 3.4. Market Trends

- 3.4.1. Increasing Demand in Accuracy to Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Civil Aviation

- 5.1.2. Defense

- 5.1.3. Consumer Electronics

- 5.1.4. Automotive

- 5.1.5. Energy and Infrastructure

- 5.1.6. Medical

- 5.1.7. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Accelerometer

- 5.2.2. Gyroscope

- 5.2.3. IMU

- 5.2.4. Magnetometer

- 5.2.5. Attitude Heading and Navigation System

- 5.2.6. Other Components

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. United States NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Civil Aviation

- 6.1.2. Defense

- 6.1.3. Consumer Electronics

- 6.1.4. Automotive

- 6.1.5. Energy and Infrastructure

- 6.1.6. Medical

- 6.1.7. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by Component

- 6.2.1. Accelerometer

- 6.2.2. Gyroscope

- 6.2.3. IMU

- 6.2.4. Magnetometer

- 6.2.5. Attitude Heading and Navigation System

- 6.2.6. Other Components

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Canada NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Civil Aviation

- 7.1.2. Defense

- 7.1.3. Consumer Electronics

- 7.1.4. Automotive

- 7.1.5. Energy and Infrastructure

- 7.1.6. Medical

- 7.1.7. Other Applications

- 7.2. Market Analysis, Insights and Forecast - by Component

- 7.2.1. Accelerometer

- 7.2.2. Gyroscope

- 7.2.3. IMU

- 7.2.4. Magnetometer

- 7.2.5. Attitude Heading and Navigation System

- 7.2.6. Other Components

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. North America NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 United States

- 8.1.2 Canada

- 8.1.3 Mexico

- 9. Europe NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1 Germany

- 9.1.2 United Kingdom

- 9.1.3 France

- 9.1.4 Spain

- 9.1.5 Italy

- 9.1.6 Spain

- 9.1.7 Belgium

- 9.1.8 Netherland

- 9.1.9 Nordics

- 9.1.10 Rest of Europe

- 10. Asia Pacific NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 China

- 10.1.2 Japan

- 10.1.3 India

- 10.1.4 South Korea

- 10.1.5 Southeast Asia

- 10.1.6 Australia

- 10.1.7 Indonesia

- 10.1.8 Phillipes

- 10.1.9 Singapore

- 10.1.10 Thailandc

- 10.1.11 Rest of Asia Pacific

- 11. South America NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 Brazil

- 11.1.2 Argentina

- 11.1.3 Peru

- 11.1.4 Chile

- 11.1.5 Colombia

- 11.1.6 Ecuador

- 11.1.7 Venezuela

- 11.1.8 Rest of South America

- 12. North America NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United States

- 12.1.2 Canada

- 12.1.3 Mexico

- 13. MEA NA Inertial Systems Market Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 United Arab Emirates

- 13.1.2 Saudi Arabia

- 13.1.3 South Africa

- 13.1.4 Rest of Middle East and Africa

- 14. Competitive Analysis

- 14.1. Global Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Rockwell Collins Inc

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 VectorNav Technologies

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Fairchild Semiconductor (ON Semiconductors)

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Safran Group (SAGEM)

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Bosch Sensortec GmbH

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Moog Inc

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Thales Group

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 STMicroelectronics NV

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Meggitt PLC*List Not Exhaustive

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Analog Devices Inc

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.11 Honeywell Aerospace Inc

- 14.2.11.1. Overview

- 14.2.11.2. Products

- 14.2.11.3. SWOT Analysis

- 14.2.11.4. Recent Developments

- 14.2.11.5. Financials (Based on Availability)

- 14.2.12 InvenSense Inc

- 14.2.12.1. Overview

- 14.2.12.2. Products

- 14.2.12.3. SWOT Analysis

- 14.2.12.4. Recent Developments

- 14.2.12.5. Financials (Based on Availability)

- 14.2.13 Northrop Grumman Corporation

- 14.2.13.1. Overview

- 14.2.13.2. Products

- 14.2.13.3. SWOT Analysis

- 14.2.13.4. Recent Developments

- 14.2.13.5. Financials (Based on Availability)

- 14.2.1 Rockwell Collins Inc

List of Figures

- Figure 1: Global NA Inertial Systems Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 3: North America NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 9: South America NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 11: North America NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 12: MEA NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 13: MEA NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 14: United States NA Inertial Systems Market Revenue (Million), by Application 2024 & 2032

- Figure 15: United States NA Inertial Systems Market Revenue Share (%), by Application 2024 & 2032

- Figure 16: United States NA Inertial Systems Market Revenue (Million), by Component 2024 & 2032

- Figure 17: United States NA Inertial Systems Market Revenue Share (%), by Component 2024 & 2032

- Figure 18: United States NA Inertial Systems Market Revenue (Million), by Geography 2024 & 2032

- Figure 19: United States NA Inertial Systems Market Revenue Share (%), by Geography 2024 & 2032

- Figure 20: United States NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 21: United States NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

- Figure 22: Canada NA Inertial Systems Market Revenue (Million), by Application 2024 & 2032

- Figure 23: Canada NA Inertial Systems Market Revenue Share (%), by Application 2024 & 2032

- Figure 24: Canada NA Inertial Systems Market Revenue (Million), by Component 2024 & 2032

- Figure 25: Canada NA Inertial Systems Market Revenue Share (%), by Component 2024 & 2032

- Figure 26: Canada NA Inertial Systems Market Revenue (Million), by Geography 2024 & 2032

- Figure 27: Canada NA Inertial Systems Market Revenue Share (%), by Geography 2024 & 2032

- Figure 28: Canada NA Inertial Systems Market Revenue (Million), by Country 2024 & 2032

- Figure 29: Canada NA Inertial Systems Market Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global NA Inertial Systems Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global NA Inertial Systems Market Revenue Million Forecast, by Application 2019 & 2032

- Table 3: Global NA Inertial Systems Market Revenue Million Forecast, by Component 2019 & 2032

- Table 4: Global NA Inertial Systems Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: Global NA Inertial Systems Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Germany NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United Kingdom NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: France NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Italy NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Spain NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Belgium NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Netherland NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Nordics NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Europe NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 22: China NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Japan NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: India NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Korea NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Southeast Asia NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Australia NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Indonesia NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Phillipes NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Singapore NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Thailandc NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Rest of Asia Pacific NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 34: Brazil NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Argentina NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Peru NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Chile NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Colombia NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Ecuador NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Venezuela NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Rest of South America NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 43: United States NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Canada NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Mexico NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 47: United Arab Emirates NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Saudi Arabia NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: South Africa NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Middle East and Africa NA Inertial Systems Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global NA Inertial Systems Market Revenue Million Forecast, by Application 2019 & 2032

- Table 52: Global NA Inertial Systems Market Revenue Million Forecast, by Component 2019 & 2032

- Table 53: Global NA Inertial Systems Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 54: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

- Table 55: Global NA Inertial Systems Market Revenue Million Forecast, by Application 2019 & 2032

- Table 56: Global NA Inertial Systems Market Revenue Million Forecast, by Component 2019 & 2032

- Table 57: Global NA Inertial Systems Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 58: Global NA Inertial Systems Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the NA Inertial Systems Market?

The projected CAGR is approximately 5.90%.

2. Which companies are prominent players in the NA Inertial Systems Market?

Key companies in the market include Rockwell Collins Inc, VectorNav Technologies, Fairchild Semiconductor (ON Semiconductors), Safran Group (SAGEM), Bosch Sensortec GmbH, Moog Inc, Thales Group, STMicroelectronics NV, Meggitt PLC*List Not Exhaustive, Analog Devices Inc, Honeywell Aerospace Inc, InvenSense Inc, Northrop Grumman Corporation.

3. What are the main segments of the NA Inertial Systems Market?

The market segments include Application, Component, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Emergence of MEMS Technology; Inclination of Growth Toward Defense and Aerospace; Technological Advancements in Navigation Systems.

6. What are the notable trends driving market growth?

Increasing Demand in Accuracy to Drive the Market.

7. Are there any restraints impacting market growth?

Operational Complexity and High Maintenance Costs.

8. Can you provide examples of recent developments in the market?

January 2023 - Inertial Labs released an upgraded version of the "INS-U" GPS-Aided Inertial Navigation System and an extended version of the Differential Pressure Sensor and Embedded Air Data Computer, allowing the unit to measure airspeed with up to 600 KNOTS to enhance high dynamic applications. This new INS-U version can send fused (GNSS + IMU) NMEA data to Pixhawk Autopilot, allowing Pixhawk Autopilot to navigate UAVs in GNSS-denied environments for extended periods (more than 1 hour).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "NA Inertial Systems Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the NA Inertial Systems Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the NA Inertial Systems Market?

To stay informed about further developments, trends, and reports in the NA Inertial Systems Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence