Key Insights

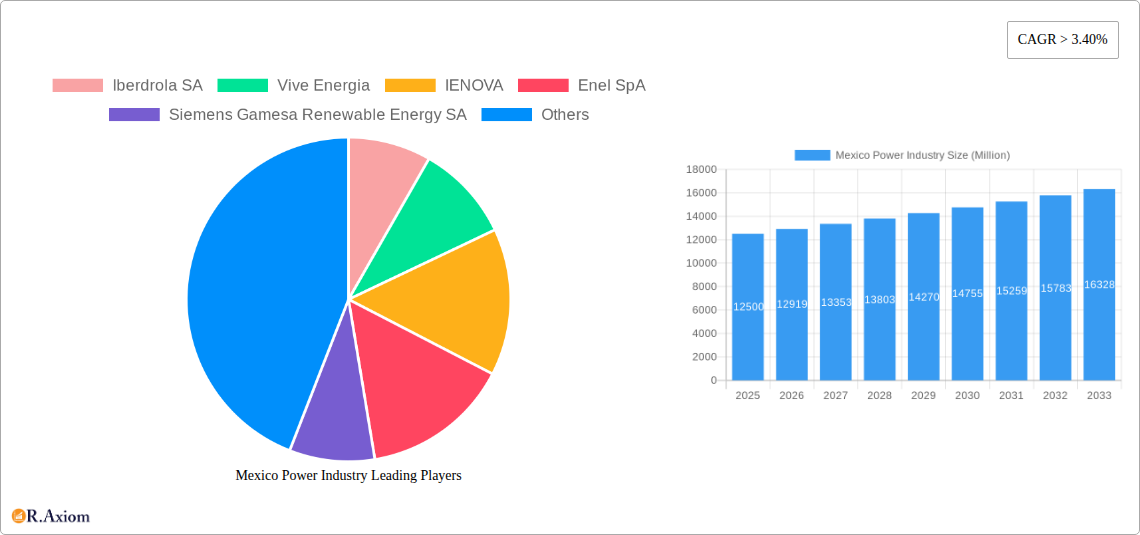

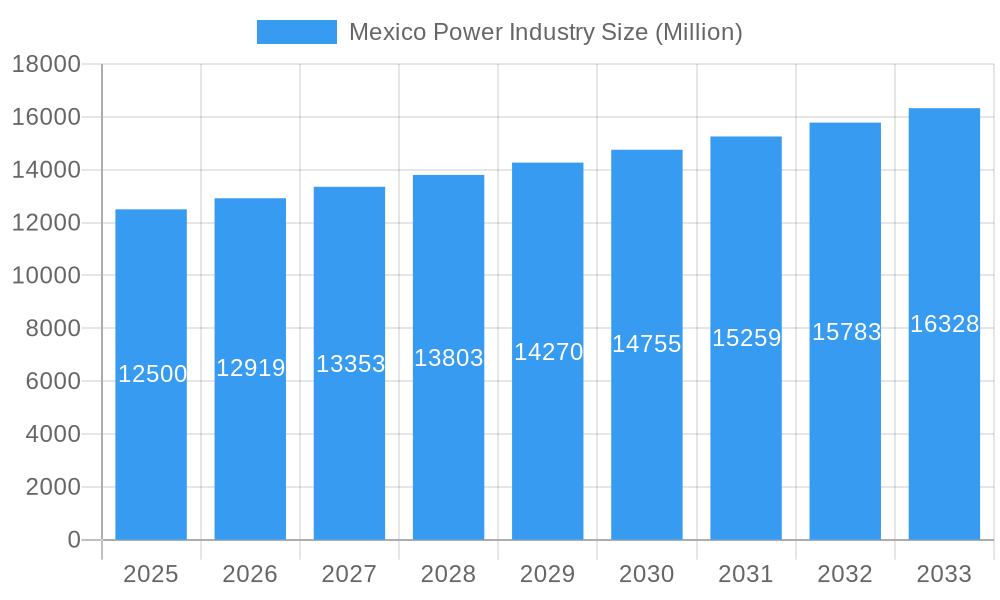

Mexico's power industry is projected for substantial expansion, anticipated to reach $7.83 billion by 2025, growing at a Compound Annual Growth Rate (CAGR) of 3.26% through 2033. This growth is fueled by escalating electricity demand from residential, commercial, and industrial sectors, alongside government-led grid modernization and energy efficiency programs. Mexico's advantageous location and robust economic performance further support these trends. A significant driver is the increasing adoption of renewable energy, especially solar and wind, as the nation pursues climate targets and diversifies its energy portfolio beyond fossil fuels, supported by supportive policies and decreasing technology costs.

Mexico Power Industry Market Size (In Billion)

The market is segmented into Power Generation and Power Transmission and Distribution (T&D). While thermal power remains dominant in generation, renewables are expanding rapidly. Hydroelectric power is a stable contributor, with emerging technologies and smaller projects falling under "Other Power Generation." The T&D segment is vital for reliable energy delivery to a growing customer base and integrating new, often decentralized, power sources. Investments are prioritizing the enhancement and expansion of T&D networks to minimize losses and improve grid stability. Leading companies such as Iberdrola SA, Enel SpA, and Comision Federal de Electricidad are spearheading this evolution with investments in renewables and grid infrastructure. Nevertheless, challenges persist, including regulatory complexities and substantial capital requirements for large-scale development, which may influence growth rates in specific areas.

Mexico Power Industry Company Market Share

Mexico Power Industry Market Concentration & Innovation

The Mexico power industry exhibits a dynamic market concentration, influenced by significant regulatory shifts and ongoing innovation. The recent acquisition of 13 power plants by the Mexican government from Iberdrola SA for USD 6 Billion, alongside plans to grant Comision Federal de Electricidad (CFE) majority control, indicates a trend towards increased state influence and consolidation within the electricity market. This move, alongside the November 2022 bilateral agreement on nuclear energy with the United States, aims to bolster energy security and foster cooperation. Innovation is primarily driven by the expansion of renewable energy sources, with companies like Vive Energia, Enel SpA, and Jinko Solar Holdings Co Ltd actively investing in solar and wind power. Siemens Gamesa Renewable Energy SA and Acciona SA are key players in the wind sector, contributing significantly to the industry's technological advancement. The threat of product substitutes, such as advancements in distributed generation and battery storage, is compelling established players to adapt and integrate new technologies. End-user trends are shifting towards cleaner energy solutions, pushing for greater efficiency and sustainability across the power generation and distribution segments. Merger and acquisition (M&A) activities, exemplified by the Iberdrola deal valued at approximately 6 Million, are reshaping the competitive landscape. IENOVA and Sempra Energy are also active participants, further contributing to the evolving market structure. The market, currently at a 4 6 Market Rankin, is poised for further transformation.

Mexico Power Industry Industry Trends & Insights

The Mexico power industry is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period of 2025–2033. This expansion is fueled by increasing energy demand driven by industrialization, urbanization, and a growing population. The sector is undergoing a significant transformation towards cleaner energy, with a substantial push for renewable energy sources. This includes a notable increase in solar photovoltaic (PV) and wind power installations, reflecting a global trend towards decarbonization and a commitment to meeting climate change objectives. Technological disruptions are at the forefront, with advancements in smart grid technologies, energy storage solutions, and digitalized power management systems enhancing operational efficiency and reliability. The integration of these technologies is crucial for managing the intermittent nature of renewable energy and ensuring grid stability. Consumer preferences are increasingly aligning with sustainable energy solutions, driving demand for green energy options and pushing companies to adopt more environmentally friendly practices. Competitive dynamics are intensifying, with both established state-owned entities like Comision Federal de Electricidad (CFE) and private sector players such as Iberdrola SA, Vive Energia, IENOVA, Enel SpA, Siemens Gamesa Renewable Energy SA, Jinko Solar Holdings Co Ltd, Aldesa Energias Renovables SLU, Acciona SA, and Sempra Energy vying for market share. Strategic partnerships and investments in new generation capacity are key strategies employed by these companies. The market penetration of renewable energy, particularly in the solar segment, has seen a significant uptick, moving from approximately 20% in the historical period (2019-2024) to an estimated 35% by the end of the forecast period. The government's energy policies, aimed at promoting both traditional and renewable energy sources, play a pivotal role in shaping these trends. The ongoing evolution of the regulatory framework also presents both opportunities and challenges for market participants.

Dominant Markets & Segments in Mexico Power Industry

The Mexico power industry is characterized by a complex interplay of dominant markets and segments, with Power Transmission and Distribution (T&D) emerging as a cornerstone of the sector's infrastructure and growth. This segment is critical for ensuring the reliable and efficient delivery of electricity from generation sources to end-users across the nation. The dominance of T&D is underpinned by substantial investments in upgrading and expanding the existing grid infrastructure to accommodate the increasing influx of power, particularly from burgeoning renewable energy projects.

Key drivers for the dominance of Power Transmission and Distribution include:

- Economic Policies: Government initiatives and national development plans that prioritize energy security and industrial growth necessitate a robust and modern T&D network.

- Infrastructure Development: Continuous investment in transmission lines, substations, and distribution networks is crucial for meeting rising energy demand and integrating diverse energy sources.

- Technological Advancements: The adoption of smart grid technologies, including advanced metering infrastructure (AMI), Supervisory Control and Data Acquisition (SCADA) systems, and grid automation, enhances the efficiency, resilience, and reliability of the T&D network.

Within Power Generation, the Renewables segment is experiencing remarkable growth and is poised to become increasingly dominant. This surge is driven by Mexico's abundant solar and wind resources, coupled with supportive government policies and international commitments to reduce carbon emissions. Companies like Vive Energia, Enel SpA, and Jinko Solar Holdings Co Ltd are at the forefront of this renewable energy revolution, investing heavily in solar farms and wind power projects. The Thermal power generation segment, while historically dominant, is gradually seeing its share tempered by the rise of renewables. However, it remains a crucial component of Mexico's energy mix, providing baseload power and ensuring grid stability. Hydro power, a significant contributor to the nation's energy supply, continues to play a vital role, although its expansion is often constrained by geographical limitations and environmental considerations. The Other Power Generation segment, encompassing sources like geothermal and waste-to-energy, represents a smaller but growing part of the energy landscape, reflecting diversification efforts. The market size for the T&D segment is estimated to be around USD 15 Billion in the base year of 2025, with a projected growth to USD 22 Billion by 2033. The Renewables segment's market size is anticipated to grow from USD 10 Billion in 2025 to USD 18 Billion by 2033, demonstrating its rapidly increasing importance.

Mexico Power Industry Product Developments

Product innovations in the Mexico power industry are primarily focused on enhancing the efficiency, sustainability, and reliability of energy generation, transmission, and distribution. This includes the development of advanced solar photovoltaic (PV) panels with higher conversion efficiencies by companies like Jinko Solar Holdings Co Ltd, and more powerful and durable wind turbines by manufacturers such as Siemens Gamesa Renewable Energy SA. In the realm of energy storage, advancements in battery technologies are crucial for integrating intermittent renewable sources into the grid. Smart grid technologies, including intelligent meters and grid management software, are continuously being refined to optimize power flow and reduce transmission losses. These innovations offer competitive advantages by lowering operational costs, improving grid stability, and meeting the growing demand for cleaner energy solutions.

Mexico Power Industry Report Scope & Segmentation Analysis

This report comprehensively analyzes the Mexico power industry, segmented into key areas. Power Generation is examined across Thermal, Hydro, Renewables, and Other Power Generation. The Renewables segment, encompassing solar, wind, and other sustainable sources, is projected to experience the highest growth rate, driven by favorable government policies and declining technology costs. The Power Transmission and Distribution (T&D) segment is analyzed as a distinct entity, crucial for grid modernization and efficient energy delivery, with significant investment anticipated in infrastructure upgrades. Growth projections for the Renewables segment are robust, with an estimated market size of USD 10 Billion in the base year (2025) growing to USD 18 Billion by 2033. The T&D segment is estimated at USD 15 Billion in 2025, projected to reach USD 22 Billion by 2033.

Key Drivers of Mexico Power Industry Growth

The Mexico power industry's growth is propelled by a confluence of powerful factors. Government initiatives promoting energy independence and diversification are paramount, encouraging investment in both traditional and renewable energy sources. The increasing demand for electricity, fueled by a growing population and expanding industrial sector, provides a consistent market impetus. Technological advancements, particularly in solar and wind energy, are making these cleaner alternatives more cost-competitive and efficient, accelerating their adoption. The ongoing modernization of the power grid infrastructure to enhance reliability and accommodate new generation sources is also a significant driver. Furthermore, Mexico's commitment to international climate agreements is pushing the country towards a greener energy future, creating substantial opportunities for renewable energy development.

Challenges in the Mexico Power Industry Sector

Despite its growth potential, the Mexico power industry faces several significant challenges. Regulatory uncertainty and frequent policy shifts can create an unpredictable investment environment, deterring long-term capital commitments. The aging infrastructure in certain regions necessitates substantial upgrades, presenting a significant financial burden. Supply chain disruptions for critical components, particularly for renewable energy installations, can lead to project delays and increased costs. Furthermore, competition from established state-owned entities and the complexities of market liberalization pose hurdles for private sector players. The significant upfront capital required for large-scale power projects, coupled with challenges in securing financing, also remains a considerable restraint.

Emerging Opportunities in Mexico Power Industry

Emerging opportunities in the Mexico power industry are abundant and diverse. The significant untapped potential for solar and wind energy generation presents a vast landscape for new project development and investment. The growing demand for energy storage solutions, driven by the need to stabilize grids with high renewable penetration, offers a burgeoning market. Opportunities also exist in distributed generation, empowering consumers to produce their own electricity, and in the modernization of existing T&D infrastructure to improve efficiency and resilience. Furthermore, the government's focus on energy security and diversification opens avenues for innovation in various clean energy technologies, including green hydrogen and advanced biofuels.

Leading Players in the Mexico Power Industry Market

- Iberdrola SA

- Vive Energia

- IENOVA

- Enel SpA

- Siemens Gamesa Renewable Energy SA

- Comision Federal de Electricidad

- Jinko Solar Holdings Co Ltd

- Aldesa Energias Renovables SLU

- Acciona SA

- Sempra Energy

Key Developments in Mexico Power Industry Industry

- Apr 2023: The Mexican government agreed to buy 13 power plants from the Spanish energy company Iberdrola SA. The deal is worth USD 6 Billion. The government also plans to give state-owned power company Comision Federal de Electricidad (CFE) majority control over the electricity market. This development signifies a significant shift towards increased state control and consolidation within the Mexican electricity sector.

- Nov 2022: The United States and Mexico, through their bilateral agreement on nuclear energy, entered into force to enhance cooperation on energy security. The agreement enables the peaceful transfer of nuclear material, equipment, and information from the United States in adherence with nonproliferation requirements. This reinforces energy security and collaborative efforts in the nuclear energy domain.

Strategic Outlook for Mexico Power Industry Market

The strategic outlook for the Mexico power industry is one of significant growth and transformation, driven by a robust demand for electricity and a strong governmental push towards clean energy. The continued expansion of renewable energy, particularly solar and wind power, will be a defining characteristic of the market. Investments in modernizing the power transmission and distribution network are essential for integrating these new capacities and ensuring grid stability. Opportunities in energy storage, smart grid technologies, and distributed generation will also play a crucial role in shaping the future landscape. Companies that can navigate the evolving regulatory environment, embrace technological innovation, and focus on sustainable energy solutions are poised for substantial success in this dynamic market. The estimated market size of the entire industry is projected to reach USD 55 Billion by 2033, with a CAGR of approximately 7.5%.

Mexico Power Industry Segmentation

-

1. Power Generation

- 1.1. Thermal

- 1.2. Hydro

- 1.3. Renewables

- 1.4. Other Power Generation

- 2. Power Transmission and Distribution (T&D)

Mexico Power Industry Segmentation By Geography

- 1. Mexico

Mexico Power Industry Regional Market Share

Geographic Coverage of Mexico Power Industry

Mexico Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.26% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 5.1.1. Thermal

- 5.1.2. Hydro

- 5.1.3. Renewables

- 5.1.4. Other Power Generation

- 5.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution (T&D)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 6. Mexico Power Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Power Generation

- 6.1.1. Thermal

- 6.1.2. Hydro

- 6.1.3. Renewables

- 6.1.4. Other Power Generation

- 6.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution (T&D)

- 6.1. Market Analysis, Insights and Forecast - by Power Generation

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Iberdrola SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Vive Energia

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 IENOVA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Enel SpA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Siemens Gamesa Renewable Energy SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Comision Federal de Electricidad

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Jinko Solar Holdings Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Aldesa Energias Renovables SLU*List Not Exhaustive 6 4 Market Rankin

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Acciona SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sempra Energy

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Iberdrola SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Mexico Power Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Mexico Power Industry Share (%) by Company 2025

List of Tables

- Table 1: Mexico Power Industry Revenue billion Forecast, by Power Generation 2020 & 2033

- Table 2: Mexico Power Industry Volume gigawatt Forecast, by Power Generation 2020 & 2033

- Table 3: Mexico Power Industry Revenue billion Forecast, by Power Transmission and Distribution (T&D) 2020 & 2033

- Table 4: Mexico Power Industry Volume gigawatt Forecast, by Power Transmission and Distribution (T&D) 2020 & 2033

- Table 5: Mexico Power Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Mexico Power Industry Volume gigawatt Forecast, by Region 2020 & 2033

- Table 7: Mexico Power Industry Revenue billion Forecast, by Power Generation 2020 & 2033

- Table 8: Mexico Power Industry Volume gigawatt Forecast, by Power Generation 2020 & 2033

- Table 9: Mexico Power Industry Revenue billion Forecast, by Power Transmission and Distribution (T&D) 2020 & 2033

- Table 10: Mexico Power Industry Volume gigawatt Forecast, by Power Transmission and Distribution (T&D) 2020 & 2033

- Table 11: Mexico Power Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Mexico Power Industry Volume gigawatt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mexico Power Industry?

The projected CAGR is approximately 3.26%.

2. Which companies are prominent players in the Mexico Power Industry?

Key companies in the market include Iberdrola SA, Vive Energia, IENOVA, Enel SpA, Siemens Gamesa Renewable Energy SA, Comision Federal de Electricidad, Jinko Solar Holdings Co Ltd, Aldesa Energias Renovables SLU*List Not Exhaustive 6 4 Market Rankin, Acciona SA, Sempra Energy.

3. What are the main segments of the Mexico Power Industry?

The market segments include Power Generation, Power Transmission and Distribution (T&D).

4. Can you provide details about the market size?

The market size is estimated to be USD 7.83 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; High Power Demand due to the Growing Population4.; Upcoming Power Generation Projects.

6. What are the notable trends driving market growth?

Thermal Power Generation Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; The New Government's Intentions to Reduce Private Investments.

8. Can you provide examples of recent developments in the market?

Apr 2023: The Mexican government agreed to buy 13 power plants from the Spanish energy company Iberdrola. The deal is worth USD 6 billion. The government also plans to give state-owned power company Comision Federal de Electricidad (CFE) majority control over the electricity market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in gigawatt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mexico Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mexico Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mexico Power Industry?

To stay informed about further developments, trends, and reports in the Mexico Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence