Key Insights

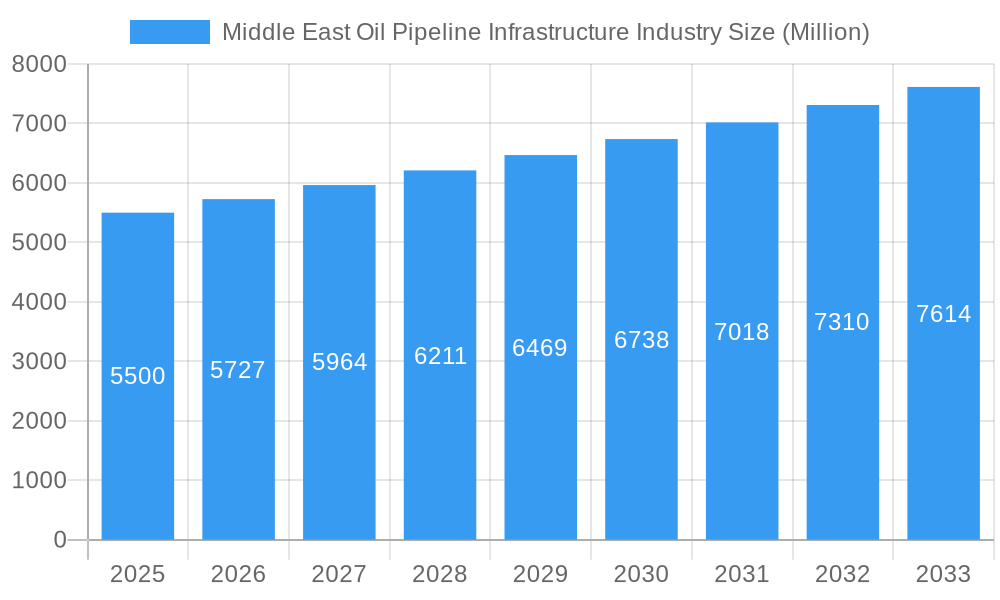

The Middle East Oil Pipeline Infrastructure market is poised for significant growth, estimated at USD 5.50 billion in 2025, and is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.12% through 2033. This robust expansion is primarily driven by the region's substantial oil reserves and the continuous need to enhance and expand its oil transportation networks to meet both domestic energy demands and global export requirements. Key growth catalysts include ongoing investments in exploration and production activities, the development of new oil fields, and the imperative to upgrade aging pipeline infrastructure for improved safety, efficiency, and environmental compliance. The increasing focus on energy security and the strategic importance of the Middle East as a global oil supplier further bolster the market's positive trajectory. The market is segmented by type into Seamless and Welded pipelines, with both playing crucial roles depending on the specific application and pressure requirements. Seamless pipelines are often favored for high-pressure applications and critical infrastructure due to their inherent strength and integrity, while welded pipelines offer cost-effectiveness for certain segments.

Middle East Oil Pipeline Infrastructure Industry Market Size (In Billion)

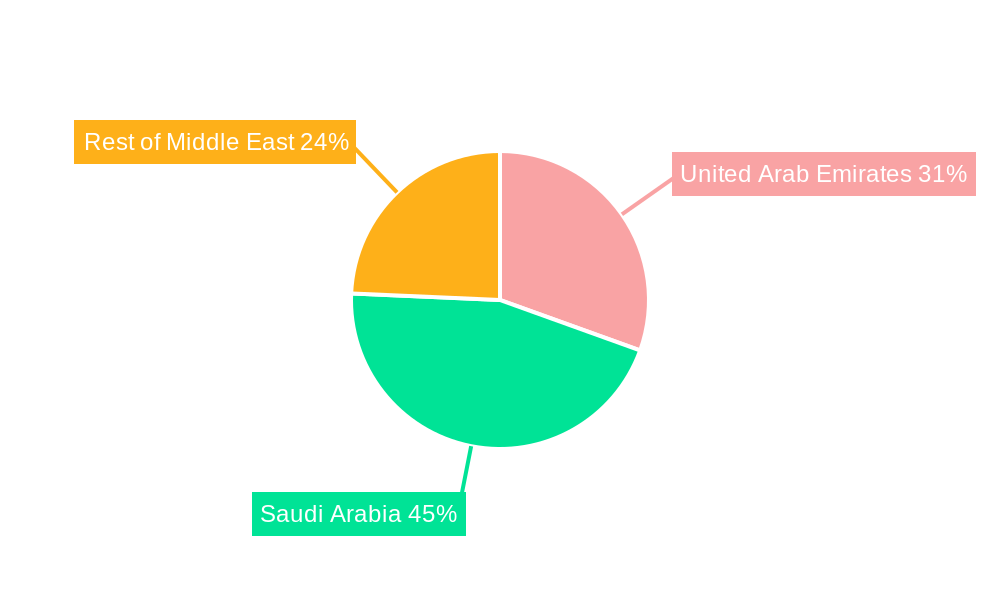

Geographically, the market is dominated by Saudi Arabia and the United Arab Emirates, which represent the largest consumers and investors in oil pipeline infrastructure due to their status as major oil producers and exporters. The "Rest of the Middle East" segment, encompassing countries like Kuwait, Qatar, Iraq, and Oman, also contributes significantly, driven by their own production capacities and strategic export initiatives. Emerging trends include the adoption of advanced materials and technologies for pipeline construction and maintenance, such as smart coatings for corrosion resistance and the integration of IoT devices for real-time monitoring and predictive maintenance. These advancements aim to reduce operational costs, minimize downtime, and enhance the overall lifespan and reliability of oil pipelines. However, the market faces restraints such as volatile crude oil prices, which can impact investment decisions, and stringent environmental regulations that necessitate significant compliance costs and sophisticated technological solutions for emission control and leak detection. Geopolitical uncertainties in the region can also pose challenges to long-term project planning and execution.

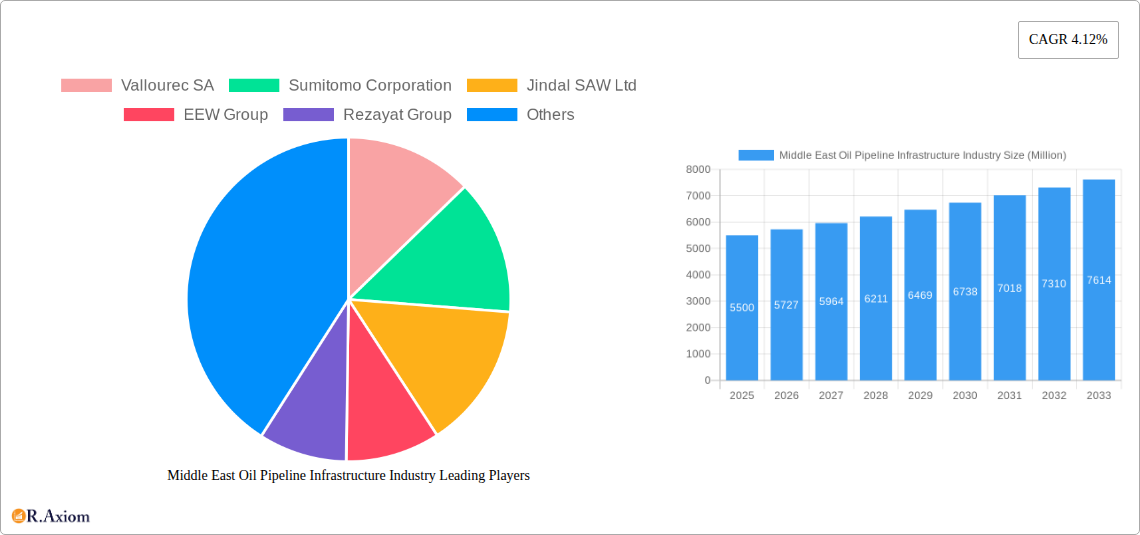

Middle East Oil Pipeline Infrastructure Industry Company Market Share

Middle East Oil Pipeline Infrastructure Industry Market Concentration & Innovation

The Middle East oil pipeline infrastructure industry exhibits a moderate market concentration, with a few large, established players dominating significant portions of the market. Key companies such as Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, and ArcelorMittal SA are pivotal in shaping the industry's landscape. While specific market share data fluctuates, these entities collectively account for a substantial portion of the total market value. Innovation drivers are primarily focused on enhancing pipeline efficiency, durability, and safety. This includes advancements in corrosion-resistant materials, smart pipeline technologies for real-time monitoring, and the development of high-strength steel alloys. Regulatory frameworks are crucial, often driven by government mandates for environmental protection, safety standards, and the strategic importance of energy exports. Product substitutes, while limited for large-scale oil and gas transport, include alternative transportation methods like supertankers for specific export routes and, in the longer term, the potential for LNG terminals for gas. End-user trends point towards increasing demand for higher-pressure pipelines and pipelines capable of handling higher-temperature fluids. Mergers and acquisitions (M&A) activities are sporadic but significant, often aimed at consolidating market presence, acquiring new technologies, or expanding geographical reach. Deal values can range from tens of millions to hundreds of millions of millions of dollars, as seen in strategic partnerships and company acquisitions within the sector.

Middle East Oil Pipeline Infrastructure Industry Industry Trends & Insights

The Middle East oil pipeline infrastructure industry is poised for robust growth, driven by an insatiable global demand for crude oil and natural gas, coupled with the region's pivotal role as a major energy producer. The market is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.8% during the forecast period of 2025–2033. This expansion is underpinned by several key market growth drivers. Firstly, substantial investments in upstream exploration and production by national oil companies (NOCs) and international oil companies (IOCs) necessitate the development and expansion of associated pipeline networks to transport extracted resources to processing facilities and export terminals. Secondly, the ongoing pursuit of energy diversification and the development of new oil and gas fields across the region fuel demand for new pipeline construction and upgrades to existing infrastructure. Technological disruptions are playing an increasingly important role, with the adoption of digitalization and automation becoming paramount. This includes the implementation of advanced SCADA (Supervisory Control and Data Acquisition) systems, AI-powered predictive maintenance, and IoT sensors for enhanced operational efficiency and safety. Consumer preferences, in this context, translate to the demand for reliable, secure, and environmentally sound energy transportation solutions. The competitive dynamics within the industry are characterized by a blend of global manufacturers and specialized regional players. Intense competition exists in securing large-scale project bids, driving innovation in cost-effectiveness and project execution timelines. Market penetration is steadily increasing as countries within the region prioritize energy security and export capacity enhancement, leading to a higher proportion of oil and gas being transported via pipelines. The strategic importance of the Middle East in global energy markets ensures a sustained need for a resilient and expansive pipeline infrastructure, making it a cornerstone of the global energy supply chain.

Dominant Markets & Segments in Middle East Oil Pipeline Infrastructure Industry

Within the Middle East oil pipeline infrastructure industry, Saudi Arabia consistently emerges as the dominant market. Its extensive hydrocarbon reserves, coupled with a strategic vision for expanding oil and gas production and export capabilities, fuel significant ongoing and planned investments in pipeline networks. Economic policies, particularly those focused on diversifying national economies away from sole reliance on crude oil exports, often include substantial investment in downstream industries that require robust pipeline infrastructure for feedstock and product transportation. Infrastructure development is paramount; Saudi Arabia's commitment to world-class industrial cities like Jubail and Yanbu, along with ambitious giga-projects, necessitates extensive pipeline networks to support their operations.

- Key Drivers for Saudi Arabia's Dominance:

- Vast Oil and Gas Reserves: The sheer scale of its hydrocarbon resources mandates a comprehensive and expanding pipeline network.

- Strategic Export Hubs: Development of advanced export terminals and associated pipelines to cater to global demand.

- Downstream Industrialization: Significant investments in petrochemicals and refining require efficient feedstock and product transport.

- Government Investment and Vision: Ambitious national development plans, such as Saudi Vision 2030, prioritize infrastructure development, including pipelines.

The United Arab Emirates (UAE) follows closely, driven by its strategic geographic location and its role as a significant oil and gas producer and exporter. Abu Dhabi's substantial offshore reserves and Dubai's position as a global trade hub necessitate continuous investment in pipeline networks for both domestic consumption and international trade. The UAE's proactive approach to energy infrastructure modernization and its focus on attracting foreign investment contribute to its strong market position.

The Rest of Middle East segment, while less dominant than Saudi Arabia or the UAE individually, collectively represents a substantial market. This includes countries like Qatar, a major liquefied natural gas (LNG) exporter, which requires extensive offshore and onshore pipeline infrastructure for gas extraction and liquefaction. Kuwait and Iraq also continue to invest in upgrading and expanding their pipeline networks to bolster production and export capacities. The Welded segment within the pipeline Type often dominates in terms of volume for large-diameter, long-haul oil and gas transmission pipelines, owing to its cost-effectiveness and structural integrity for such applications. However, the Seamless segment is crucial for specialized applications, particularly in high-pressure gas transmission and for transporting aggressive or high-temperature fluids, where its inherent strength and uniformity are critical.

Middle East Oil Pipeline Infrastructure Industry Product Developments

Product developments in the Middle East oil pipeline infrastructure industry are increasingly focused on enhancing performance, safety, and environmental sustainability. Innovations in high-strength, corrosion-resistant steel alloys are crucial for extending pipeline lifespan in harsh Middle Eastern environments, reducing maintenance costs and the risk of leaks. The integration of smart pipeline technologies, such as fiber optic sensing and advanced leak detection systems, allows for real-time monitoring of pipeline integrity, pressure, and flow rates. These technologies offer significant competitive advantages by enabling proactive maintenance, minimizing downtime, and improving operational safety. Furthermore, the development of specialized coatings and linings is addressing the challenges posed by corrosive crude oils and gas compositions, ensuring product quality and preventing infrastructure degradation. The market fit for these developments is directly driven by the region's commitment to maximizing resource extraction efficiency and adhering to increasingly stringent environmental regulations.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Middle East Oil Pipeline Infrastructure Industry, covering the period from 2019 to 2033, with a base and estimated year of 2025, and a forecast period of 2025–2033.

- By Type: The market is segmented into Seamless and Welded pipelines. The Seamless segment, while typically used for higher-value, specialized applications like high-pressure gas transmission, is projected to grow at a steady pace. The Welded segment is expected to dominate in terms of volume, driven by the construction of large-diameter transmission lines for crude oil and gas.

- By Geography: The analysis encompasses key regions including the United Arab Emirates, Saudi Arabia, and the Rest of Middle East. Saudi Arabia is anticipated to lead in market size and growth, followed by the UAE. The Rest of Middle East segment, encompassing countries like Qatar, Kuwait, and Iraq, will exhibit significant growth driven by their specific energy export strategies and infrastructure development needs.

Key Drivers of Middle East Oil Pipeline Infrastructure Industry Growth

The growth of the Middle East oil pipeline infrastructure industry is propelled by several fundamental drivers. Firstly, the region's status as a global energy powerhouse necessitates continuous investment in expanding and modernizing its vast network of oil and gas pipelines to meet ever-increasing global demand. Secondly, government initiatives focused on energy security and export diversification are fueling substantial capital expenditure in new pipeline projects and the upgrade of existing ones. Technological advancements, particularly in materials science and digital monitoring systems, are enabling the construction of more efficient, durable, and safer pipelines, thereby driving adoption and investment. Furthermore, ongoing upstream exploration and production activities across the region continuously create demand for new pipeline infrastructure to transport extracted hydrocarbons to processing facilities and export terminals.

Challenges in the Middle East Oil Pipeline Infrastructure Industry Sector

Despite its growth trajectory, the Middle East oil pipeline infrastructure sector faces several significant challenges. Geopolitical instability and regional conflicts can disrupt project timelines, increase security costs, and deter foreign investment. Stringent environmental regulations, while essential, add complexity and cost to project development and operation, requiring advanced technologies and rigorous compliance measures. Supply chain disruptions, including the availability of specialized materials and skilled labor, can lead to project delays and cost overruns. Furthermore, the industry grapples with intense competition, particularly from global players with advanced technological capabilities, which can put pressure on profit margins for local manufacturers.

Emerging Opportunities in Middle East Oil Pipeline Infrastructure Industry

Emerging opportunities within the Middle East oil pipeline infrastructure industry are primarily centered around technological innovation and evolving energy landscapes. The increasing focus on decarbonization presents opportunities for developing pipelines capable of transporting lower-carbon fuels like hydrogen or CO2 for carbon capture and storage (CCS) projects. The integration of advanced digital technologies, such as AI and machine learning for predictive maintenance and real-time performance optimization, offers significant potential for enhancing operational efficiency and safety. Furthermore, the ongoing development of new energy fields and the expansion of processing capacities create sustained demand for new pipeline construction and upgrades, particularly in less developed segments of the region.

Leading Players in the Middle East Oil Pipeline Infrastructure Industry Market

- Vallourec SA

- Sumitomo Corporation

- Jindal SAW Ltd

- EEW Group

- Rezayat Group

- Arabian Pipes Company

- ArcelorMittal SA

Key Developments in Middle East Oil Pipeline Infrastructure Industry Industry

- August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023.

- March 2023: Gas Arabian Services Company has been granted a USD 13.58 million engineering, procurement, and construction (EPC) contract for a gas pipeline by Advanced Petrochemical Company (Advanced). The pipeline will connect Advanced's Propane Dehydrogenation (PDH) unit to Jubail United's cracking unit for upgrading the by-product gas stream to high-value chemicals.

Strategic Outlook for Middle East Oil Pipeline Infrastructure Industry Market

The strategic outlook for the Middle East oil pipeline infrastructure market remains exceptionally positive, buoyed by the region's critical role in global energy supply and its unwavering commitment to expanding production and export capabilities. Significant investments are anticipated in both new pipeline construction and the modernization of existing infrastructure to accommodate increased volumes and higher-pressure requirements. The increasing adoption of advanced technologies, including smart pipeline systems and innovative materials, will be a key differentiator, driving efficiency and sustainability. Opportunities in transporting new energy carriers, such as hydrogen, and the expansion of carbon capture infrastructure will further shape the market's future. This dynamic environment underscores the sustained importance of robust pipeline networks as the backbone of the region's energy economy and its influence on global energy markets.

Middle East Oil Pipeline Infrastructure Industry Segmentation

-

1. Type

- 1.1. Seamless

- 1.2. Welded

-

2. Geography

- 2.1. United Arab Emirates

- 2.2. Saudi Arabia

- 2.3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry Segmentation By Geography

- 1. United Arab Emirates

- 2. Saudi Arabia

- 3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry Regional Market Share

Geographic Coverage of Middle East Oil Pipeline Infrastructure Industry

Middle East Oil Pipeline Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Seamless

- 5.1.2. Welded

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United Arab Emirates

- 5.2.2. Saudi Arabia

- 5.2.3. Rest of Middle East

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Rest of Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Seamless

- 6.1.2. Welded

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United Arab Emirates

- 6.2.2. Saudi Arabia

- 6.2.3. Rest of Middle East

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Seamless

- 7.1.2. Welded

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United Arab Emirates

- 7.2.2. Saudi Arabia

- 7.2.3. Rest of Middle East

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Seamless

- 8.1.2. Welded

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United Arab Emirates

- 8.2.2. Saudi Arabia

- 8.2.3. Rest of Middle East

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Seamless

- 9.1.2. Welded

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United Arab Emirates

- 9.2.2. Saudi Arabia

- 9.2.3. Rest of Middle East

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Vallourec SA

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Sumitomo Corporation

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Jindal SAW Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 EEW Group

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Rezayat Group

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Arabian Pipes Company

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 ArcelorMittal SA*List Not Exhaustive

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.1 Vallourec SA

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Middle East Oil Pipeline Infrastructure Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Middle East Oil Pipeline Infrastructure Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 3: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 9: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Oil Pipeline Infrastructure Industry?

The projected CAGR is approximately 4.12%.

2. Which companies are prominent players in the Middle East Oil Pipeline Infrastructure Industry?

Key companies in the market include Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, ArcelorMittal SA*List Not Exhaustive.

3. What are the main segments of the Middle East Oil Pipeline Infrastructure Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.50 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing.

6. What are the notable trends driving market growth?

Seamless Type Segment to Witness a Significant Growth.

7. Are there any restraints impacting market growth?

4.; High Exploration Cost.

8. Can you provide examples of recent developments in the market?

August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Oil Pipeline Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Oil Pipeline Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Oil Pipeline Infrastructure Industry?

To stay informed about further developments, trends, and reports in the Middle East Oil Pipeline Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence