Key Insights

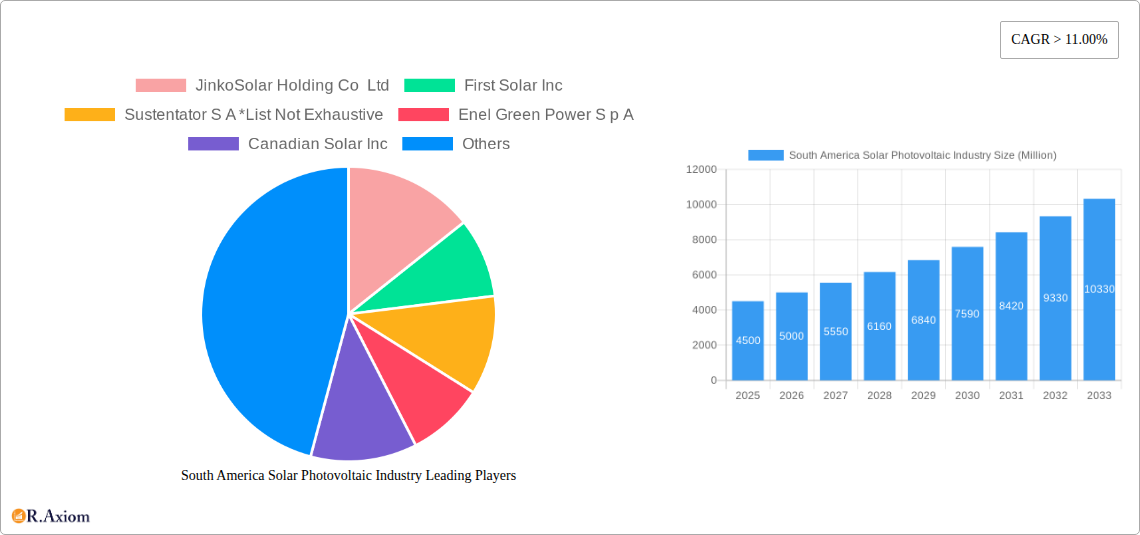

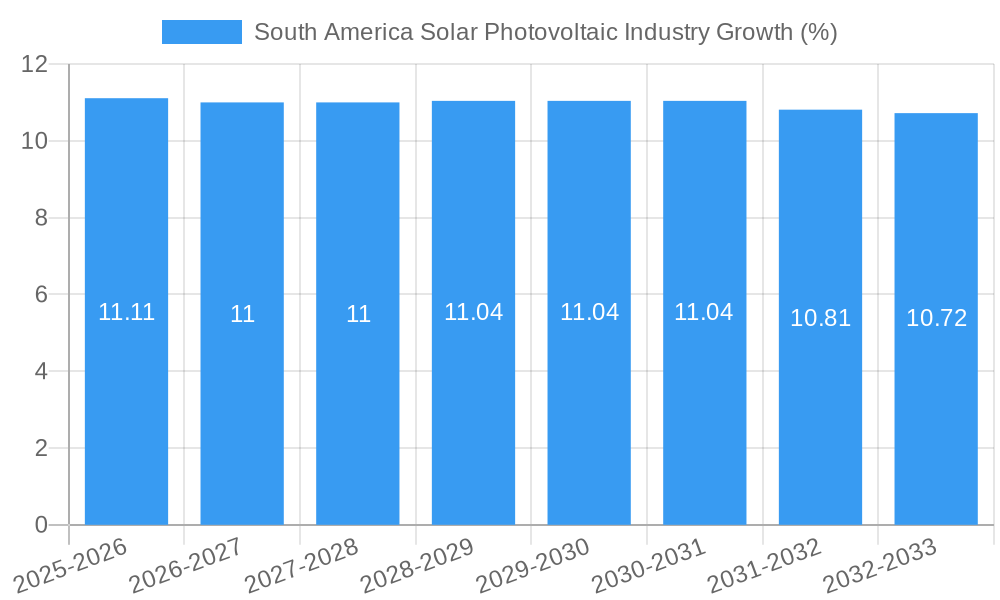

The South America Solar Photovoltaic Industry is poised for substantial growth, with a current market size estimated at approximately USD 4,500 million and a projected Compound Annual Growth Rate (CAGR) exceeding 11.00% from 2025 to 2033. This robust expansion is primarily driven by a confluence of factors, including favorable government policies and incentives across key nations like Brazil and Chile, a growing awareness of environmental sustainability, and the decreasing cost of solar technology. The region's abundant solar irradiation further bolsters the economic viability of solar projects, making it an increasingly attractive investment destination. Demand is being significantly propelled by the widespread adoption of both ground-mounted and rooftop solar installations, catering to the diverse needs of residential, commercial, and industrial end-users.

The market's trajectory is further shaped by several key trends. A notable shift towards large-scale utility projects, coupled with an increasing number of distributed generation installations, signifies a maturing market. Advancements in solar panel efficiency and energy storage solutions are also playing a crucial role in enhancing the reliability and competitiveness of solar power. However, certain restraints, such as initial capital investment for large projects, evolving regulatory frameworks, and grid integration challenges, require careful management. Nevertheless, with major players like JinkoSolar, First Solar, Canadian Solar, and Enel Green Power actively participating and investing in the region, the outlook for the South America Solar Photovoltaic Industry remains exceptionally bright, promising significant contributions to the region's energy transition and economic development.

South America Solar Photovoltaic Industry Market Concentration & Innovation

The South America solar photovoltaic (PV) industry exhibits a moderate to high market concentration, driven by a mix of large international players and increasingly capable regional developers. Key industry leaders such as JinkoSolar Holding Co Ltd, First Solar Inc, Enel Green Power S.p.A., Canadian Solar Inc, JA Solar Holdings Co. Ltd, Acciona S.A., Sonnedix Power Holdings Ltd, and Trina Solar Limited are instrumental in shaping market dynamics. Sustentator S.A. and Atlas Renewable Energy are also significant contributors, particularly within specific geographic niches. Innovation is primarily fueled by advancements in PV module efficiency, the development of cost-effective energy storage solutions, and the integration of smart grid technologies. Regulatory frameworks across South America are evolving, with many nations implementing favorable policies such as tax incentives, feed-in tariffs, and competitive auctions to encourage solar adoption. However, policy consistency remains a crucial factor for sustained investment. Product substitutes, including traditional fossil fuels and hydropower, still represent competition, though the declining cost of solar PV is steadily eroding their market share. End-user trends lean towards increasing demand from Commercial and Industrial (C&I) sectors seeking to reduce operating expenses and enhance sustainability, alongside growing interest from the Residential segment driven by energy independence and cost savings. Mergers and acquisitions (M&A) activities are anticipated to increase as larger entities consolidate their presence and smaller, innovative companies seek strategic partnerships or exits. While specific M&A deal values are not available for this general overview, the trend indicates a maturing market seeking efficiency and scale.

South America Solar Photovoltaic Industry Industry Trends & Insights

The South America solar photovoltaic industry is poised for substantial growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 18.5% during the forecast period. This robust expansion is underpinned by a confluence of favorable trends, including declining solar technology costs, increasing energy demand, and supportive government policies across key markets. The market penetration of solar PV is rapidly accelerating, driven by the economic imperative to diversify energy portfolios away from volatile fossil fuel prices and towards cleaner, more sustainable alternatives. Technological disruptions are playing a pivotal role, with advancements in bifacial solar modules, perovskite solar cells, and sophisticated energy storage systems promising higher efficiency and lower levelized cost of electricity (LCOE). These innovations are making solar power increasingly competitive with conventional energy sources. Consumer preferences are shifting significantly, with a growing awareness of environmental issues and a desire for energy independence driving adoption at both the residential and commercial levels. Businesses are increasingly investing in behind-the-meter solar installations to hedge against rising electricity tariffs and meet corporate social responsibility (CSR) goals. The competitive landscape is characterized by the presence of global PV manufacturers and developers, alongside a rising number of local companies that are building significant project pipelines. Strategic partnerships and joint ventures are becoming common as companies aim to leverage expertise, share risks, and access capital for large-scale projects. Furthermore, the integration of solar PV with digital technologies, such as AI-powered energy management systems and blockchain for peer-to-peer energy trading, is creating new avenues for value creation and operational efficiency. The availability of attractive financing mechanisms and the increasing participation of international financial institutions are also critical enablers of this growth trajectory. The industry is moving towards more integrated solutions that combine solar generation with battery storage, enhancing grid stability and providing reliable power even during intermittent supply periods. The economic resilience of solar PV projects, often supported by long-term power purchase agreements (PPAs), makes them attractive investments in a region with diverse economic conditions.

Dominant Markets & Segments in South America Solar Photovoltaic Industry

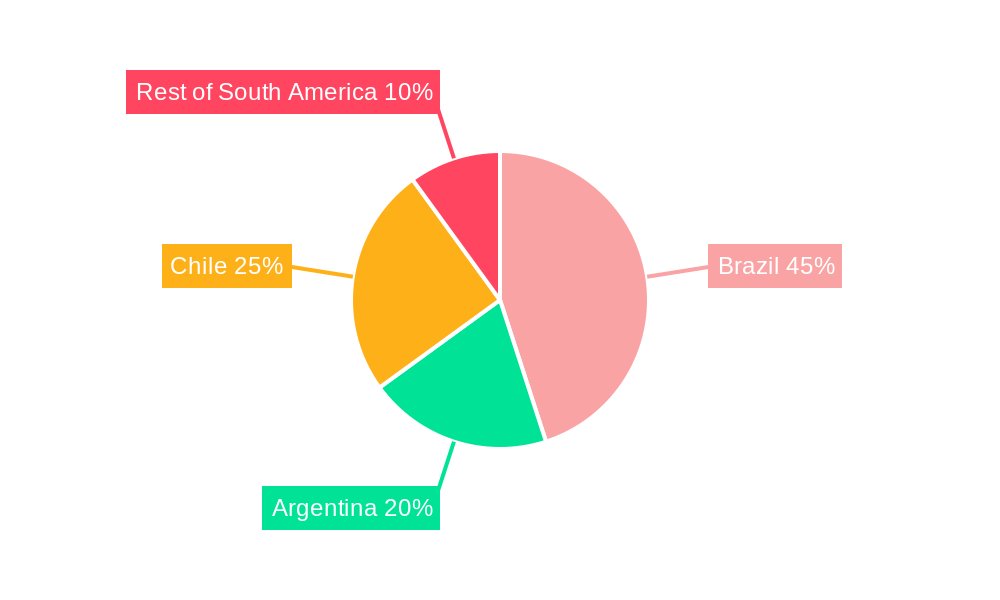

Brazil stands out as the dominant market within the South America solar photovoltaic industry, driven by its vast landmass, significant solar irradiance, and a proactive regulatory environment that has fostered substantial investment. The Ground Mounted segment holds a commanding lead in terms of installed capacity, primarily due to the prevalence of utility-scale solar farms that benefit from economies of scale and efficient land utilization. However, the Rooftop segment, encompassing both Residential and Commercial and Industrial (C&I) end-users, is experiencing rapid growth, particularly in urban centers where land availability is limited and energy costs are higher.

Key Drivers of Dominance in Brazil:

- Economic Policies: Government incentives, including net metering policies and competitive auction mechanisms, have been instrumental in attracting significant domestic and international investment.

- Resource Availability: Brazil possesses excellent solar irradiance levels across many of its regions, making solar power generation highly efficient.

- Energy Demand: A large population and a growing industrial base contribute to a substantial and ever-increasing demand for electricity, creating a strong market for solar solutions.

- Infrastructure Development: Ongoing investments in grid modernization and expansion are crucial for integrating the increasing volume of solar energy into the national power mix.

Argentina and Chile are also significant contributors to the regional solar PV market, exhibiting strong growth trends. Chile, in particular, has been a pioneer in solar development in South America, with a favorable climate and consistent policy support. Argentina is actively expanding its renewable energy capacity, with solar PV playing a crucial role in its energy transition plans. The Rest of South America, encompassing countries like Colombia, Peru, and Ecuador, is gradually increasing its solar PV adoption, with nascent but promising market growth driven by a desire to diversify energy sources and achieve greater energy security.

Across all geographies, the Commercial and Industrial (C&I) end-user segment is a major driver of solar PV deployment. Businesses are increasingly recognizing the financial benefits of installing solar systems, such as reduced electricity bills, predictable energy costs, and enhanced corporate sustainability profiles. The Residential segment is also gaining momentum, fueled by declining system costs, the availability of financing options, and a growing consumer desire for energy independence and environmental consciousness. The Ground Mounted segment is projected to continue its dominance in terms of total installed capacity due to the ongoing development of large-scale solar parks, but the Rooftop segment is expected to witness a higher percentage growth rate as distributed generation becomes more mainstream.

South America Solar Photovoltaic Industry Product Developments

Product innovation in the South America solar photovoltaic industry is rapidly enhancing efficiency and cost-effectiveness. Key advancements include the widespread adoption of bifacial solar modules, which can capture sunlight from both sides, increasing energy yield by an estimated 5-20%. Improvements in PV cell technology, such as the integration of PERC (Passivated Emitter and Rear Cell) and TOPCon (Tunnel Oxide Passivated Contact) architectures, are pushing module efficiencies to over 22%. Furthermore, the development of more efficient and affordable energy storage solutions, particularly lithium-ion batteries, is crucial for addressing the intermittency of solar power and enabling greater grid integration. These product developments are making solar PV increasingly competitive and reliable for a wider range of applications, from utility-scale projects to residential installations.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the South America Solar Photovoltaic Industry, segmented across various critical parameters.

Deployment: The Ground Mounted segment is thoroughly analyzed, covering utility-scale solar farms and large commercial installations, with growth projections and market size estimates for major countries. The Rooftop segment is also examined, focusing on both residential and commercial installations, including an analysis of distributed generation trends and their impact on the market.

End-User: The Residential segment is assessed for its growth potential, driven by declining costs and consumer demand for energy independence. The Commercial and Industrial (C&I) segment is detailed, highlighting its significant contribution to market growth due to cost savings and sustainability initiatives.

Geography: The report provides in-depth analysis for Brazil, Argentina, and Chile, detailing their unique market drivers, regulatory landscapes, and growth trajectories. Rest of South America is also covered, offering insights into emerging markets and opportunities in countries like Colombia, Peru, and Ecuador.

Key Drivers of South America Solar Photovoltaic Industry Growth

Several key factors are propelling the growth of the South America solar photovoltaic industry. Declining manufacturing costs of solar panels and associated equipment have made solar power increasingly competitive with conventional energy sources. Supportive government policies, including tax incentives, feed-in tariffs, and renewable energy targets, are crucial in driving investment and deployment. Increasing energy demand across the region, coupled with a desire for energy diversification and security, further fuels solar adoption. Technological advancements in PV efficiency and energy storage are enhancing the reliability and economic viability of solar projects. Furthermore, growing environmental awareness and corporate sustainability initiatives are encouraging businesses and individuals to adopt cleaner energy solutions.

Challenges in the South America Solar Photovoltaic Industry Sector

Despite its robust growth, the South America solar photovoltaic industry faces several challenges. Regulatory inconsistencies and political instability in some countries can create investment uncertainty and hinder long-term project planning. Grid integration issues, including limited transmission capacity and outdated infrastructure, can pose challenges for connecting large-scale solar farms to the grid. Supply chain disruptions, such as fluctuating raw material prices and shipping delays, can impact project timelines and costs. Financing access for smaller developers and residential projects can also be a barrier. Finally, competition from established fossil fuel industries and hydropower remains a factor, although the economic advantages of solar are steadily increasing.

Emerging Opportunities in South America Solar Photovoltaic Industry

The South America solar photovoltaic industry presents numerous emerging opportunities. The significant potential for distributed generation and rooftop solar installations across residential and commercial sectors offers substantial growth avenues. The increasing demand for solar-plus-storage solutions presents a critical opportunity to enhance grid stability and provide reliable power. Expansion into new geographic markets within the "Rest of South America" region, with tailored market entry strategies, holds considerable promise. Furthermore, the development of innovative business models, such as power purchase agreements (PPAs) for C&I clients and community solar projects, can unlock new investment streams. The integration of digitalization and smart grid technologies for optimized energy management and grid integration is another key area for future development.

Leading Players in the South America Solar Photovoltaic Industry Market

- JinkoSolar Holding Co Ltd

- First Solar Inc

- Sustentator S A

- Enel Green Power S p A

- Canadian Solar Inc

- Atlas Renewable Energy

- JA Solar Holdings Co Ltd

- Acciona SA

- Sonnedix Power Holdings Ltd

- Trina Solar Limited

Key Developments in South America Solar Photovoltaic Industry Industry

- 2024: Several countries announce updated renewable energy targets, increasing the pipeline for solar PV projects.

- 2023: Significant investments in utility-scale solar farms across Brazil and Chile, driving substantial capacity additions.

- 2022: Increased adoption of bifacial solar modules and advanced inverters, leading to improved energy yields in new installations.

- 2021: Growing interest and investment in solar-plus-storage projects to address grid stability and energy security concerns.

- 2020: Governments in Argentina and Colombia implement new policies to accelerate solar PV deployment.

- 2019: Record low auction prices for solar energy in Brazil, signaling increased cost competitiveness.

Strategic Outlook for South America Solar Photovoltaic Industry Market

The strategic outlook for the South America solar photovoltaic industry is exceptionally positive, driven by a compelling mix of economic, environmental, and technological factors. Continued policy support, coupled with the relentless decline in solar PV and battery storage costs, will fuel sustained market expansion. The increasing demand from the Commercial and Industrial sector for cost savings and sustainability compliance will remain a primary growth catalyst. Emerging opportunities in distributed generation, microgrids, and innovative financing models will further diversify the market landscape. As the region prioritizes energy security and decarbonization, solar photovoltaic technology is set to play an increasingly pivotal role in its energy future, making it an attractive sector for continued investment and development.

South America Solar Photovoltaic Industry Segmentation

-

1. Deployment

- 1.1. Ground Mounted

- 1.2. Rooftop

-

2. End-User

- 2.1. Residential

- 2.2. Commercial and Industrial

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Chile

- 3.4. Rest of South America

South America Solar Photovoltaic Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Chile

- 4. Rest of South America

South America Solar Photovoltaic Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 11.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Integration of Renewable Energy4.; Supportive Government Policies

- 3.3. Market Restrains

- 3.3.1. 4.; High infrastructure costs

- 3.4. Market Trends

- 3.4.1. Ground Mounted Solar PV to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Ground Mounted

- 5.1.2. Rooftop

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Residential

- 5.2.2. Commercial and Industrial

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Chile

- 5.3.4. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Chile

- 5.4.4. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Brazil South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Ground Mounted

- 6.1.2. Rooftop

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Residential

- 6.2.2. Commercial and Industrial

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Chile

- 6.3.4. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Argentina South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Ground Mounted

- 7.1.2. Rooftop

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Residential

- 7.2.2. Commercial and Industrial

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Chile

- 7.3.4. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Chile South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Ground Mounted

- 8.1.2. Rooftop

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Residential

- 8.2.2. Commercial and Industrial

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Chile

- 8.3.4. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Rest of South America South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Ground Mounted

- 9.1.2. Rooftop

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Residential

- 9.2.2. Commercial and Industrial

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Chile

- 9.3.4. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Brazil South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 11. Argentina South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of South America South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 JinkoSolar Holding Co Ltd

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 First Solar Inc

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Sustentator S A *List Not Exhaustive

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Enel Green Power S p A

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Canadian Solar Inc

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Atlas Renewable Energy

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 JA Solar Holdings Co Ltd

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Acciona SA

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Sonnedix Power Holdings Ltd

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Trina Solar Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 JinkoSolar Holding Co Ltd

List of Figures

- Figure 1: South America Solar Photovoltaic Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: South America Solar Photovoltaic Industry Share (%) by Company 2024

List of Tables

- Table 1: South America Solar Photovoltaic Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: South America Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 3: South America Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: South America Solar Photovoltaic Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: South America Solar Photovoltaic Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: South America Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Brazil South America Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Argentina South America Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of South America South America Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: South America Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 11: South America Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 12: South America Solar Photovoltaic Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 13: South America Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: South America Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 15: South America Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 16: South America Solar Photovoltaic Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 17: South America Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: South America Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 19: South America Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 20: South America Solar Photovoltaic Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: South America Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: South America Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 23: South America Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 24: South America Solar Photovoltaic Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 25: South America Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Solar Photovoltaic Industry?

The projected CAGR is approximately > 11.00%.

2. Which companies are prominent players in the South America Solar Photovoltaic Industry?

Key companies in the market include JinkoSolar Holding Co Ltd, First Solar Inc, Sustentator S A *List Not Exhaustive, Enel Green Power S p A, Canadian Solar Inc, Atlas Renewable Energy, JA Solar Holdings Co Ltd, Acciona SA, Sonnedix Power Holdings Ltd, Trina Solar Limited.

3. What are the main segments of the South America Solar Photovoltaic Industry?

The market segments include Deployment, End-User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Integration of Renewable Energy4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Ground Mounted Solar PV to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High infrastructure costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Solar Photovoltaic Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Solar Photovoltaic Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Solar Photovoltaic Industry?

To stay informed about further developments, trends, and reports in the South America Solar Photovoltaic Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence