Key Insights

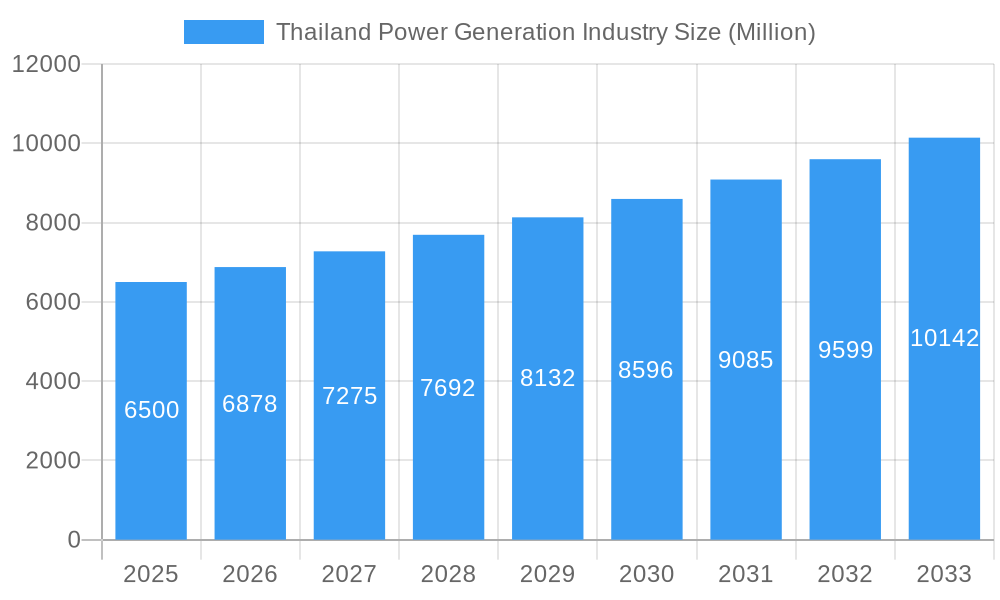

The Thailand Power Generation Industry is projected for substantial growth, with an estimated market size of $1.7 billion by 2024. This expansion is driven by escalating energy demands from industrialization and population growth, alongside government strategies to diversify the energy portfolio and bolster energy security. A significant driver is the increased adoption of renewable energy, specifically solar and wind power, aligning with Thailand's decarbonization objectives and efforts to lessen dependence on fossil fuel imports. Advancements in power transmission and distribution technologies further enhance efficiency, reliability, and grid stability, supporting this market trajectory. The industry is anticipated to achieve a Compound Annual Growth Rate (CAGR) of 9.1%.

Thailand Power Generation Industry Market Size (In Billion)

Supportive government policies, renewable energy incentives, and rising environmental consciousness among stakeholders are key factors fueling this market expansion. Industry leaders are investing in capacity enhancement, technological innovation, and strategic collaborations to leverage emerging opportunities. The market is segmented by conventional and renewable power generation, with ongoing development in transmission and distribution infrastructure. While the shift to cleaner energy presents opportunities, potential challenges include grid integration complexities, upfront investment for new technologies, and evolving regulations. Overall, Thailand's power generation sector presents a dynamic and expanding landscape, attracting significant investment.

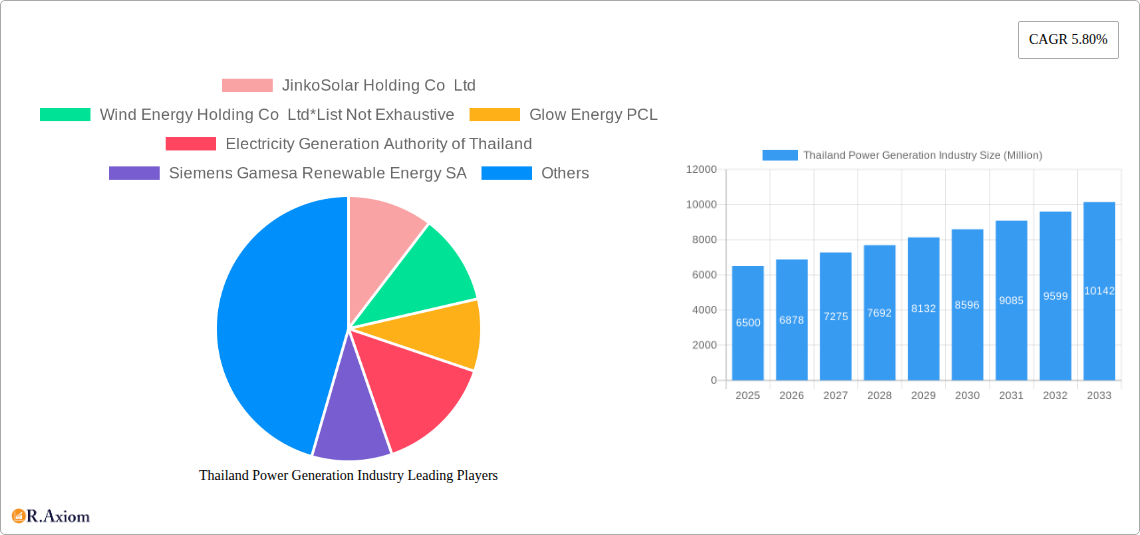

Thailand Power Generation Industry Company Market Share

Thailand Power Generation Industry: Comprehensive Market Analysis and Future Outlook (2019-2033)

This in-depth report provides a comprehensive analysis of the Thailand power generation industry, forecasting market dynamics and identifying key opportunities from 2019 to 2033. The study encompasses a detailed examination of conventional and renewable power generation, alongside power transmission and distribution. We leverage extensive market intelligence and granular data to deliver actionable insights for stakeholders seeking to capitalize on Thailand's evolving energy landscape. The base year for estimations is 2025, with a forecast period extending from 2025 to 2033, building upon historical data from 2019 to 2024.

Thailand Power Generation Industry Market Concentration & Innovation

The Thailand power generation industry exhibits a moderate to high market concentration, with key players dominating significant market shares. Innovation is a critical driver, fueled by government initiatives promoting renewable energy adoption and technological advancements in energy storage solutions. Regulatory frameworks, such as feed-in tariffs and renewable portfolio standards, are instrumental in shaping market dynamics and encouraging investment. While the market is influenced by global trends, the penetration of product substitutes remains relatively low due to the essential nature of electricity. End-user trends point towards an increasing demand for cleaner and more reliable energy sources, influencing investment strategies. Mergers and acquisitions (M&A) activities are anticipated to increase as companies seek to consolidate their market position and expand their operational capabilities. M&A deal values are expected to range from tens of millions to over a billion US Dollars as strategic alliances and acquisitions become more prevalent. The market share of leading conventional power generation companies is estimated to be around 40-50%, while the renewable energy segment is experiencing rapid growth, with key players holding a combined market share projected to exceed 20% by 2033.

Thailand Power Generation Industry Industry Trends & Insights

The Thailand power generation industry is poised for significant growth, driven by a confluence of factors including robust economic expansion, increasing energy demand from industrial and residential sectors, and a strong governmental push towards sustainable energy. The projected Compound Annual Growth Rate (CAGR) for the overall market is approximately 5.5%, with the renewable energy segment experiencing a much higher CAGR of over 12%. Technological disruptions are rapidly reshaping the industry, with advancements in solar PV efficiency, wind turbine technology, and advanced battery energy storage systems playing a pivotal role. The integration of smart grid technologies is also enhancing grid reliability and efficiency. Consumer preferences are increasingly shifting towards environmentally friendly energy solutions, leading to greater adoption of rooftop solar and other decentralized renewable energy sources. Market penetration of renewable energy is expected to reach over 35% by 2033. The competitive dynamics are intensifying, with both domestic and international players vying for market share. This competition is fostering innovation and driving down costs, making clean energy more accessible. The government's commitment to energy security and diversification is a cornerstone of these trends, ensuring a stable and growing market for power generation companies. The growing emphasis on energy efficiency measures across various sectors also contributes to a more balanced and sustainable energy demand.

Dominant Markets & Segments in Thailand Power Generation Industry

The dominant market within the Thailand power generation industry is driven by the Power Generation: Renewables segment, propelled by strong government support and favorable economic policies aimed at decarbonization and energy independence. Key drivers include:

- Economic Policies: The Thai government has implemented aggressive policies to promote renewable energy, including tax incentives, solar farm auctions, and net metering schemes, fostering substantial investment in solar and wind power. The National Energy Policy Committee's (NEPC) targets for renewable energy integration are a significant catalyst.

- Infrastructure Development: Significant investments are being made in grid modernization and expansion to accommodate the increasing influx of renewable energy sources, particularly in areas with high solar and wind potential. This includes upgrades to transmission lines and substations to handle distributed generation.

- Environmental Regulations: Thailand's commitment to climate change mitigation and reduction of greenhouse gas emissions is a crucial factor, mandating a shift away from fossil fuels towards cleaner alternatives.

- Technological Advancements: The decreasing cost of solar photovoltaic (PV) panels and wind turbines, coupled with improvements in energy storage technologies, makes renewables increasingly competitive with conventional power sources.

Within the Power Generation: Renewables segment, solar power currently holds the largest market share due to its widespread applicability and decreasing installation costs. However, wind energy is experiencing rapid growth, particularly in coastal regions. The Power Transmission and Distribution segment is also experiencing substantial growth as it underpins the reliable integration of new generation capacities, especially intermittent renewables. The growth in this segment is directly correlated with the expansion of the generation capacity, requiring upgrades to handle bidirectional power flow and decentralized energy sources.

Thailand Power Generation Industry Product Developments

Product developments in the Thailand power generation industry are increasingly focused on enhancing efficiency, sustainability, and grid integration. Innovations in solar technology include bifacial solar panels and advanced inverter systems that optimize energy capture and conversion. Wind energy sector advancements involve larger, more efficient turbines designed for various wind conditions and offshore applications. A key area of development is in energy storage solutions, with advancements in lithium-ion battery technology and emerging solutions like flow batteries offering improved capacity, lifespan, and safety. Smart grid technologies, including advanced metering infrastructure (AMI) and demand-side management systems, are also gaining traction, enabling better grid control and consumer engagement. These product developments are crucial for enhancing the reliability and flexibility of the power system, particularly with the increasing penetration of renewable energy sources.

Report Scope & Segmentation Analysis

This report analyzes the Thailand power generation industry across key segments: Power Generation: Conventional, Power Generation: Renewables, and Power Transmission and Distribution.

The Power Generation: Conventional segment, encompassing thermal power plants (coal, natural gas), remains a crucial part of Thailand's energy mix, though its growth is expected to moderate in favor of cleaner alternatives. Market size is projected to be approximately 40 Million Megawatts by 2025.

The Power Generation: Renewables segment is the fastest-growing, driven by solar and wind power. Market size is projected to exceed 15 Million Megawatts by 2025, with significant growth anticipated through 2033. Competitive dynamics are characterized by increasing market entry and technological advancements.

The Power Transmission and Distribution segment is vital for grid stability and the integration of renewable energy. Its market size is projected to be over 30 Million Megawatts by 2025, with substantial investments in infrastructure upgrades to support the evolving generation landscape.

Key Drivers of Thailand Power Generation Industry Growth

The Thailand power generation industry's growth is propelled by several key factors. Economically, a growing population and expanding industrial base are increasing overall energy demand. Technologically, advancements in renewable energy technologies like solar PV and wind turbines, coupled with cost reductions, are making clean energy more accessible and competitive. Regulatory frameworks, including government targets for renewable energy integration and supportive policies like feed-in tariffs and tax incentives, are crucial for attracting investment and facilitating project development. Furthermore, Thailand's commitment to energy security and reducing reliance on fossil fuel imports is a significant driver for diversifying its energy mix towards domestic renewable resources.

Challenges in the Thailand Power Generation Industry Sector

Despite the positive growth trajectory, the Thailand power generation industry faces several challenges. Regulatory hurdles, including lengthy permitting processes and complex land acquisition procedures for large-scale projects, can impede development timelines. Supply chain issues, such as the availability of specialized components and skilled labor for renewable energy installations, can also present bottlenecks. Competitive pressures are intensifying, with established players and new entrants vying for market share, potentially leading to price volatility. Furthermore, the intermittent nature of renewable energy sources necessitates significant investment in grid modernization and energy storage to ensure grid stability and reliability. Managing the transition from conventional to renewable sources requires careful planning and substantial capital investment.

Emerging Opportunities in Thailand Power Generation Industry

Emerging opportunities in the Thailand power generation industry are primarily centered around the expanding renewable energy sector and advancements in energy storage. The growing demand for decentralized energy solutions and the potential for smart grid development present significant avenues for growth. Opportunities also lie in the development of green hydrogen production, offshore wind farms, and advanced waste-to-energy technologies. The increasing focus on energy efficiency and demand-side management also opens up new market niches. Furthermore, Thailand's strategic location and its role as a regional hub offer opportunities for cross-border energy trade and collaboration, particularly within the ASEAN region. The government's continued push for sustainable development and net-zero targets will further fuel these emerging trends.

Leading Players in the Thailand Power Generation Industry Market

- JinkoSolar Holding Co Ltd

- Wind Energy Holding Co Ltd

- Glow Energy PCL

- Electricity Generation Authority of Thailand

- Siemens Gamesa Renewable Energy SA

- Schneider Electric SE

- SGS SA

- BCPG PCL

- SIAM SOLAR

- Vestas Wind Systems AS

- General Electric Company

Key Developments in Thailand Power Generation Industry Industry

- May 2023: Mae Hing Son province launched a solar power plant and battery energy storage project. The Electricity Generating Authority of Thailand (EGAT) held a commercial operation date (COD) ceremony for a 3 MW solar power plant and 4 MW battery energy storage system project.

- May 2023: Acciona Energia and the Blue Circle announced inking a 25-year power purchase agreement (PPA) in Thailand for five wind farms with a total capacity of 436 MW. The projects were picked through a bidding process by the Energy Regulatory Commission (ERC), and these projects will be developed in phases. The first wind farm is expected to begin construction in 2024, and all five projects will be completed by 2030.

Strategic Outlook for Thailand Power Generation Industry Market

The strategic outlook for the Thailand power generation industry is overwhelmingly positive, driven by a clear governmental mandate for energy transition and sustainability. Continued investment in renewable energy infrastructure, particularly solar and wind, will be a primary growth catalyst. The development of robust energy storage solutions is essential to complement the increasing share of intermittent renewables, ensuring grid stability and reliability. Opportunities in smart grid technologies and digitalization will enhance operational efficiency and consumer engagement. Furthermore, Thailand's commitment to achieving net-zero emissions by 2050 will necessitate ongoing innovation and expansion in clean energy technologies, creating a dynamic and evolving market landscape. The strategic focus will be on fostering a resilient, efficient, and sustainable energy ecosystem.

Thailand Power Generation Industry Segmentation

-

1. Power Generation

- 1.1. Conventional

- 1.2. Renewables

- 2. Power Transmission and Distribution

Thailand Power Generation Industry Segmentation By Geography

- 1. Thailand

Thailand Power Generation Industry Regional Market Share

Geographic Coverage of Thailand Power Generation Industry

Thailand Power Generation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Renewables Capacity in Thailand4.; Rising Modernization of Existing Transmission and Distribution Infrastructure

- 3.3. Market Restrains

- 3.3.1. 4.; Huge Capital Expenditure Required for Carrying out Modernization of Existing Facilities

- 3.4. Market Trends

- 3.4.1. Renewable Power Generation to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Thailand Power Generation Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 5.1.1. Conventional

- 5.1.2. Renewables

- 5.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Thailand

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 JinkoSolar Holding Co Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Wind Energy Holding Co Ltd*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Glow Energy PCL

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Electricity Generation Authority of Thailand

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Siemens Gamesa Renewable Energy SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Schneider Electric SE

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 SGS SA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 BCPG PCL

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 SIAM SOLAR

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Vestas Wind Systems AS

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 General Electric Company

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 JinkoSolar Holding Co Ltd

List of Figures

- Figure 1: Thailand Power Generation Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Thailand Power Generation Industry Share (%) by Company 2025

List of Tables

- Table 1: Thailand Power Generation Industry Revenue billion Forecast, by Power Generation 2020 & 2033

- Table 2: Thailand Power Generation Industry Revenue billion Forecast, by Power Transmission and Distribution 2020 & 2033

- Table 3: Thailand Power Generation Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Thailand Power Generation Industry Revenue billion Forecast, by Power Generation 2020 & 2033

- Table 5: Thailand Power Generation Industry Revenue billion Forecast, by Power Transmission and Distribution 2020 & 2033

- Table 6: Thailand Power Generation Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thailand Power Generation Industry?

The projected CAGR is approximately 9.1%.

2. Which companies are prominent players in the Thailand Power Generation Industry?

Key companies in the market include JinkoSolar Holding Co Ltd, Wind Energy Holding Co Ltd*List Not Exhaustive, Glow Energy PCL, Electricity Generation Authority of Thailand, Siemens Gamesa Renewable Energy SA, Schneider Electric SE, SGS SA, BCPG PCL, SIAM SOLAR, Vestas Wind Systems AS, General Electric Company.

3. What are the main segments of the Thailand Power Generation Industry?

The market segments include Power Generation, Power Transmission and Distribution.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.7 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Renewables Capacity in Thailand4.; Rising Modernization of Existing Transmission and Distribution Infrastructure.

6. What are the notable trends driving market growth?

Renewable Power Generation to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Huge Capital Expenditure Required for Carrying out Modernization of Existing Facilities.

8. Can you provide examples of recent developments in the market?

May 2023: Mae Hing Son province launched a solar power plant and battery energy storage project. The Electricity Generating Authority of Thailand (EGAT) held a commercial operation date (COD) ceremony for a 3 MW solar power plant and 4 MW battery energy storage system project.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thailand Power Generation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thailand Power Generation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thailand Power Generation Industry?

To stay informed about further developments, trends, and reports in the Thailand Power Generation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence